1. ņä£ļĪĀ

ņŻ╝ņŗØņŗ£ņןņØś ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņØ┤ļĪĀņŚÉņä£ ņ×¼ļ¼┤Ļ┤Ćļ”¼ņŚÉ ņØ┤ļź┤ļŖö ņ×¼ļ¼┤ņØś ĻĘ╝ņøÉņĀüņØĖ ļČäņĢ╝ņŚÉ Ēü░ ņśüĒ¢źņØä ļ»Ėņ╣śļ®░, ņŗ£ņן ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņØä ņśłņĖĪĒĢśĻĖ░ ņ£äĒĢ£ ņŚ░ĻĄ¼Ļ░Ć ĒÖ£ļ░£ĒĢśĻ▓ī ņ¦äĒ¢ēļÉśņ¢┤ ņÖöļŗż(Ang and Bekaert, 2006; Cochrane, 2008; Welch and Goyal, 2007; Campbell and Thompson, 2007; Rapach and Zhou, 2013; Neely et al., 2014; Pettenuzzo et al., 2014; Kelly and Jiang, 2014; McLean and Pontiff, 2016). ļ»Ėļל ņŗ£ņןņŚÉ ļīĆĒĢ£ ņĀĢļ│┤ļź╝ Ļ░Ćņ¦ĆĻ│Ā ņ׳ļŖö ņĀĢļ│┤Ļ▒░ļלņ×ÉņØś Ēł¼ņ×É Ē¢ēĒā£ļŖö ņłśņØĄļźĀ ņśłņĖĪņŚÉ ļīĆĒĢ£ ņżæņÜöĒĢ£ ļŗ©ņä£ļź╝ ņĀ£Ļ│ĄĒĢ£ļŗż. Miller(1977)ņÖĆ Diamond and Verrecchia(1987)ņØś ņŚ░ĻĄ¼ņŚÉ ļö░ļź┤ļ®┤ ņŗ£ņןņŚÉļŖö ļŗżņ¢æĒĢ£ ņØśĻ▓¼ņØä Ļ░Ćņ¦ä Ēł¼ņ×Éņ×ÉĻ░Ć ņ׳Ļ│Ā, Ļ│Ąļ¦żļÅä ņĀ£ņĢĮņØ┤ ņĪ┤ņ×¼ĒĢśļŖö Ļ▓ĮņÜ░ Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉļŖö ļīĆļČĆļČä ņĀĢļ│┤Ļ▒░ļלņ×ÉņØ┤ļŗż(ņĀĢļ│┤Ļ▒░ļלĻ░Ćņäż, informed trading hypothesis). ļ¼╝ļĪĀ ļ╣äņĀĢļ│┤Ļ▒░ļלņ×ÉļÅä ņŗ£ņןņØś ņ£ĀļÅÖņä▒ ĒÖĢļ│┤ ņ░©ņøÉņŚÉņä£ Ļ│Ąļ¦żļÅä Ļ▒░ļלļź╝ ņŗżņŗ£ĒĢśņ¦Ćļ¦ī, ņĀĢļ│┤Ļ▒░ļלņ×ÉļŖö ņŗ£ņןņŚÉ ņĢ×ņä£ ļ»Ėļל ņŻ╝Ļ░Ć ņĀĢļ│┤ļź╝ ņĘ©ļōØĒĢśņŚ¼ ņŻ╝ņŗØņØä ļīĆņ░©ĒĢśĻ│Ā ļ¦żļÅäĒĢ£ļŗż. ĻĘĖļ”¼Ļ│Ā ņśłņāüļīĆļĪ£ ņŻ╝Ļ░ĆĻ░Ć ĒĢśļØĮĒĢśļ®┤ ņŗ£ņןņŚÉņä£ ņŻ╝ņŗØņØä ļ¦żņłś, ļīĆņŚ¼ņ×ÉņŚÉĻ▓ī ņāüĒÖśĒĢśņŚ¼ ņ░©ņØĄņØä ņĘ©ĒĢ£ļŗż. Ēł¼ņ×Éņ×ÉļŖö Ļ│Ąļ¦żļÅä Ļ▒░ļלņŚÉņä£ ļ░£ņāØĒĢśļŖö ļ╣äņÜ®ļ│┤ļŗż ĻĖ░ļīĆļÉśļŖö ņłśņØĄņØ┤ Ēü░ Ļ▓ĮņÜ░ņŚÉļ¦ī Ļ▒░ļלļź╝ ņŗżņŗ£ĒĢśļ»ĆļĪ£ Ļ│Ąļ¦żļÅä Ļ▒░ļלņŚÉļŖö ņ£ĀļÅÖņä▒ Ļ▒░ļלļź╝ ņ£äĒĢ£ ļ╣äņĀĢļ│┤Ļ▒░ļלņ×Éļ│┤ļŗż ņĀĢļ│┤Ļ▒░ļלņ×ÉņØś ļ╣äņżæņØ┤ ņāüļīĆņĀüņ£╝ļĪ£ ļåÆņØä Ļ▓āņØä ņ£ĀņČöĒĢĀ ņłś ņ׳ļŗż. Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉĻ░Ć ļ»Ėļל ņŻ╝Ļ░ĆņŚÉ ļīĆĒĢ£ ņĀĢļ│┤ļź╝ Ļ░Ćņ¦ä ņĀĢļ│┤Ļ▒░ļלņ×ÉļØ╝ļ®┤, Ļ│Ąļ¦żļÅä ņĀ£ņĢĮņØĆ ņĀĢļ│┤Ļ▒░ļלņ×ÉņØś ņŗ£ņן ņ░ĖņŚ¼ļź╝ ņĀ£ĒĢ£ĒĢśņŚ¼ ĒĢ┤ļŗ╣ ņŻ╝Ļ░ĆņŚÉ ļīĆĒĢ£ Ļ│╝ļīĆĒÅēĻ░Ćļź╝ ņ┤łļלĒĢ£ļŗż. ņØ┤ Ļ▓ĮņÜ░ Ļ│Ąļ¦żļÅä ņĀ£ņĢĮņ£╝ļĪ£ Ļ│╝ļīĆĒÅēĻ░ĆļÉ£ ņŻ╝Ļ░ĆĻ░Ć ņĪ░ņĀĢļÉśļŖö Ļ│╝ņĀĢņŚÉņä£ ņŻ╝Ļ░Ć ĒĢśļØĮņØ┤ ļ░£ņāØĒĢśļ»ĆļĪ£ Ļ│Ąļ¦żļÅä Ļ▒░ļלņÖĆ ļ»Ėļל ņŻ╝Ļ░ĆņłśņØĄļźĀņØĆ ņØīņØś ņāüĻ┤ĆĻ┤ĆĻ│äļź╝ Ļ░Ćņ¦äļŗż.

Miller(1977)ņÖĆ Diamond and Verrecchia(1987)ņØś ņŚ░ĻĄ¼ ņØ┤Ēøä Ļ│Ąļ¦żļÅä Ļ▒░ļלņÖĆ ļ»Ėļל ņŻ╝Ļ░ĆņłśņØĄļźĀ Ļ░äņŚÉ ļŗżņ¢æĒĢ£ ņŚ░ĻĄ¼Ļ░Ć ņ¦äĒ¢ēļÉśņŚłļŗż. ņŗżņ”ØļČäņäØņØä ĒåĄĒĢ┤ Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉĻ░Ć ņĀĢļ│┤Ļ▒░ļלņ×Éņ×äņØä ļ░ØĒ×ī ļīĆĒæ£ņĀüņØĖ ņŚ░ĻĄ¼ļōżņØĆ Christophe et al.(2004), Chang et al.(2007), Diether et al.(2008), Christophe et al.(2010), Karpoff and Lou(2010) ļō▒ņØ┤ ņ׳ļŗż. Christophe et al.(2004)ņØĆ ļéśņŖżļŗź(NASDAQ)ņŚÉ ņāüņןļÉ£ Ļ░£ļ│ä ĻĖ░ņŚģņŚÉ ļīĆĒĢ┤, ņØ┤ņØĄ ļ░£Ēæ£ ņĀäņØś Ļ│Ąļ¦żļÅä Ļ▒░ļלļ¤ēņØ┤ ļ░£Ēæ£ Ēøä ņŻ╝Ļ░ĆņłśņØĄļźĀĻ│╝ ņØīņØś Ļ┤ĆĻ│äĻ░Ć ņ׳ņØīņØä ļ░ØĒśöļŗż. Chang et al.(2007)ņØĆ ĒÖŹņĮ® ņŻ╝ņŗØņŗ£ņןņŚÉņä£ Ļ│Ąļ¦żļÅä ņĀ£ņĢĮņØ┤ ņŻ╝Ļ░ĆņØś Ļ│╝ļīĆĒÅēĻ░Ćļź╝ ņ┤łļלĒĢ©ņØä ņŗżņ”ØņĀüņ£╝ļĪ£ ļ│┤ņśĆļŗż. Diether et al.(2008)ņØĆ ļ»ĖĻĄŁņ”ØĻČīņ£äņøÉĒÜī(SEC)ņÖĆ ļē┤ņÜĢņ”ØĻČīĻ▒░ļלņåī(NYSE)ņŚÉņä£ ļ░£ņāØĒĢ£ Ļ│Ąļ¦żļÅä Ļ▒░ļל ņ×ÉļŻīļź╝ ļČäņäØĒĢ£ Ļ▓░Ļ│╝, Ļ│Ąļ¦żļÅä Ļ▒░ļל ņ”ØĻ░ĆĻ░Ć ļŗ©ĻĖ░ ļ»Ėļל ņŻ╝Ļ░Ć ņłśņØĄļźĀņŚÉ ļČĆņĀĢņĀüņØĖ ņśüĒ¢źņØä ļ»Ėņ╣©ņØä ļ│┤ņśĆļŗż. Christophe et al.(2010)ņØĆ ļ»ĖĻĄŁ ļéśņŖżļŗź ĻĖ░ņŚģņØś ņĢĀļäÉļ”¼ņŖżĒŖĖ Ēł¼ņ×ÉņØśĻ▓¼Ļ│╝ Ļ│Ąļ¦żļÅä Ļ▒░ļלņØś ņłśņØĄņä▒ņØä ļČäņäØĒĢśņŚ¼ Ēł¼ņ×É ņČĢņåī ņØśĻ▓¼ ņ¦üņĀäņØś Ļ│Ąļ¦żļÅä Ļ▒░ļלĻ░Ć ņłśņØĄņä▒ņØ┤ ņ׳ņØīņØä ļ│┤ņśĆļŗż. ĒĢ£ĻĄŁņŗ£ņןņŚÉņä£ļÅä Ļ│Ąļ¦żļÅä Ļ▒░ļלņØś ņĀĢļ│┤Ļ▒░ļלĻ░ĆņäżņØä ņŗżņ”Ø ļČäņäØĒĢśļŖö ņŚ░ĻĄ¼ļōżņØ┤ ņ¦äĒ¢ēļÉśņŚłļŗż. Kim(2000)ļŖö Ļ│Ąļ¦żļÅä Ļ▒░ļל ņ¦üĒøä ņŻ╝Ļ░Ć ņłśņØĄļźĀņŚÉ ļīĆĒĢ£ ļČäņäØņØä ņ¦äĒ¢ēĒĢśņŚ¼ ĒĢ£ĻĄŁ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ Ļ│Ąļ¦żļÅä Ļ▒░ļלĻ░Ć ņĀĢļ│┤ Ļ▒░ļלņ×äņØä ņŗżņ”ØņĀüņ£╝ļĪ£ ļ│┤ņśĆļŗż. Hwang and Cho(2011)ņÖĆ Woo and Kim(2017)ņØĆ ĒĢ£ĻĄŁņŗ£ņןņŚÉņä£ Ļ│Ąļ¦żļÅä Ļ▒░ļלņÖĆ ļ»Ėļל ņŻ╝Ļ░Ć ņłśņØĄļźĀ Ļ░äņŚÉ ņØīņØś ņāüĻ┤ĆĻ┤ĆĻ│äĻ░Ć ņ׳ņØīņØä ļ│┤ņŚ¼ ņĀĢļ│┤ Ļ▒░ļל Ļ░ĆņäżņØä ņ¦Ćņ¦ĆĒĢśņśĆļŗż. Wang and Lee(2015)ļŖö ņÖĖĻĄŁņØĖ Ēł¼ņ×Éņ×Éļź╝ ņżæņŗ¼ņ£╝ļĪ£ Ļ│Ąļ¦żļÅä Ļ▒░ļלļź╝ ļČäņäØĒĢśņŚ¼, ņÖĖĻĄŁņØĖņØś ļīĆĻĘ£ļ¬© Ļ│Ąļ¦żļÅä Ļ▒░ļלĻ░Ć ļ»Ėļל ņŻ╝Ļ░Ć ņłśņØĄļźĀņŚÉ ļīĆĒĢ£ ļŗ©ĻĖ░ ņśłņĖĪļĀźņØ┤ ņ׳ņØīņØä ļ░ØĒśöļŗż. ļśÉĒĢ£, Kim and Lee(2013)ņØĆ ņÖĖĻĄŁņØĖ Ēł¼ņ×Éņ×ÉņØś Ļ│Ąļ¦żļÅä ņĀĢļ│┤ļź╝ ĒÖ£ņÜ®ĒĢ£ Ēł¼ņ×ÉņĀäļץņØś ņä▒Ļ│╝ļź╝ ļČäņäØĒĢśņŚ¼ ļ▓żņ╣śļ¦łĒü¼ ņĀäļץļ│┤ļŗż ļ│┤ļŗż ļåÆņØĆ ņä▒Ļ│╝ļź╝ ĒÜŹļōØĒĢ©ņØä ļ│┤ņśĆļŗż. Eom(2012)ņØĆ KOSDAQņŗ£ņןņŚÉņä£ ņĢĀļäÉļ”¼ņŖżĒŖĖņØś Ēł¼ņ×ÉņØśĻ▓¼Ļ│╝ Ļ│Ąļ¦żļÅä Ļ░äņØś Ļ┤ĆĻ│äļź╝ ļČäņäØĒĢśņŚ¼ Christophe et al.(2010)ņØś ņŚ░ĻĄ¼Ļ▓░Ļ│╝ņÖĆ Ļ░ÖņØ┤ ņĢĀļäÉļ”¼ņŖżĒŖĖņØś ļČĆņĀĢņĀü Ēł¼ņ×ÉņØśĻ▓¼ ņ¦üņĀäņØś Ļ│Ąļ¦żļÅä Ļ▒░ļלĻ░Ć ņłśņØĄņä▒ņØ┤ ņ׳ņØīņØä ļ│┤ņśĆļŗż.

ĒĢ£ĒÄĖ, ļŗżņØī ņŚ░ĻĄ¼ļōżņØĆ Ļ│Ąļ¦żļÅä Ļ▒░ļלĻ░Ć ņĀĢļ│┤Ļ▒░ļלļØ╝Ļ│Ā ļ│┤ĻĖ░ ņ¢┤ļĀĄļŗżĻ│Ā ņŻ╝ņןĒĢśņśĆļŗż. Daske et al.(2005)ņØĆ ĻĖ░ņŚģņØś Ļ▓Įņśüņä▒Ļ│╝ ļ░£Ēæ£ ņĀäņØś ļČĆņĀĢņĀüņØĖ ļē┤ņŖżņÖĆ Ļ│Ąļ¦żļÅä Ļ▒░ļל Ļ░äņØś Ļ┤ĆĻ│äļź╝ ļČäņäØĒĢśņśĆļŗż. ĻĘĖ Ļ▓░Ļ│╝, Ļ▓Įņśüņä▒Ļ│╝ ļ░£Ēæ£ ņĀä ļČĆņĀĢņĀüņØĖ ļē┤ņŖżņÖĆ Ļ│Ąļ¦żļÅä Ļ▒░ļל ņé¼ņØ┤ņŚÉ ņ£ĀņØśĒĢ£ Ļ┤ĆĻ│äļź╝ ļ░£Ļ▓¼ĒĢśņ¦Ć ļ¬╗ĒĢśņśĆļŗż. Henry and Koski(2010)ļŖö ņ£Āņāüņ”Øņ×É ņ¦üņĀäņØś Ļ│Ąļ¦żļÅä Ļ▒░ļל ņ×ÉļŻīļź╝ ĒÖ£ņÜ®ĒĢśņŚ¼ Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×Éļź╝ ļČäņäØĒĢśņśĆņ£╝ļéś, Ļ│Ąļ¦żļÅä Ļ▒░ļלņÖĆ ĒĢ┤ļŗ╣ ĻĖ░ņŚģ ņĀĢļ│┤ ņé¼ņØ┤ņØś Ļ┤ĆĻ│äņŚÉ ļīĆĒĢ£ ņ£ĀņØśĒĢ£ ņ”ØĻ▒░ļź╝ ļ░£Ļ▓¼ĒĢśņ¦Ć ļ¬╗Ē¢łļŗż. ņØ┤ņÖĖņŚÉļÅä ĒĢ£ĻĄŁņŗ£ņןņŚÉņä£ Ļ│Ąļ¦żļÅä Ļ▒░ļלĻ░Ć ņĀĢļ│┤ Ļ▒░ļלļØ╝Ļ│Ā ļ│┤ĻĖ░ ņ¢┤ļĀĄļŗżļŖö ļīĆĒæ£ņĀüņØĖ ņŚ░ĻĄ¼ļōżņØĆ Song(2006), Yi et al.(2010), ĻĘĖļ”¼Ļ│Ā Kim et al.(2011) ļō▒ņØ┤ ņ׳ļŗż. ĻĘĖļōżņØĆ Ļ│Ąļ¦żļÅä Ļ▒░ļלņÖĆ ļ»Ėļל ņŻ╝Ļ░ĆņłśņØĄļźĀ Ļ░äņŚÉ ņ£ĀņØśĒĢ£ ņØīņØś Ļ┤ĆĻ│äĻ░Ć ņĪ┤ņ×¼ĒĢśņ¦Ć ņĢŖņØīņØä ņŗżņ”ØņĀüņ£╝ļĪ£ ļ░ØĒśöļŗż.

Ļ░£ļ│ä ņŻ╝ņŗØņŚÉ ļīĆĒĢ£ Ļ│Ąļ¦żļÅä Ļ▒░ļלļź╝ ņŚ░ĻĄ¼ĒĢ£ ĻĖ░ņĪ┤ ņŚ░ĻĄ¼ļōżņØĆ Ļ░£ļ│ä ĻĖ░ņŚģņØś Ļ│Ąļ¦żļÅä ļ│ĆļÅÖņä▒ņØ┤ ĒĢ┤ļŗ╣ ĻĖ░ņŚģņØś ļ»Ėļל ņŻ╝Ļ░Ć ņłśņØĄļźĀĻ│╝ Ļ┤ĆļĀ©ņØ┤ ņ׳ņØīņØä ļ│┤ņśĆļŗż(Senchack and Starks, 1993; Asquith et al., 2005; Desai et al., 2002; Diether et al., 2008). ĒĢśņ¦Ćļ¦ī, Ļ░£ļ│ä ĻĖ░ņŚģņŚÉņä£ņØś Ļ┤ĆĻ│äĻ░Ć ļ░śļō£ņŗ£ ņŗ£ņן ņĀäļ░śņŚÉ ļīĆĒĢ┤ņä£ļÅä ļÅÖņØ╝ĒĢśĻ▓ī ņĀüņÜ®ļÉśņ¦ĆļŖö ņĢŖļŖöļŗżļŖö ņé¼ņŗżņØĆ ļäÉļ”¼ ņĢīļĀżņĀĖ ņ׳ļŗż. ļŗżņØīņØś ņŚ░ĻĄ¼ļōżņØĆ Ļ░£ļ│ä ņŻ╝ņŗØņŚÉņä£ņØś Ļ┤ĆĻ│äĻ░Ć ņĢäļŗī ņŗ£ņן ņĀäņ▓┤ņØś Ļ│Ąļ¦żļÅä ņĀĢļ│┤ņÖĆ ņŗ£ņן ņłśņØĄļźĀ Ļ░äņØś Ļ┤ĆĻ│äļź╝ ņé┤ĒÄ┤ļ│┤Ļ│Ā ņ׳ļŗż. Seneca(1967)ļŖö ņĀäņøö ņżæĻĖ░ņŚÉ ļ│Ė ņŗ£ņן ņĀäņ▓┤ņØś Ļ│Ąļ¦żļÅäņÖĆ S&P 500 ņ¦Ćņłś ņé¼ņØ┤ņŚÉ ņ£ĀņØśĒĢ£ ņØīņØś ņāüĻ┤ĆĻ┤ĆĻ│äĻ░Ć ņĪ┤ņ×¼ĒĢ©ņØä ļ░ØĒśöņ£╝ļéś ĒśäļīĆ ņŗ£Ļ│äņŚ┤ļČäņäØĻ│╝ Ļ│äļ¤ēĻ▓ĮņĀ£ĒĢÖņØ┤ ņČ£ĒśäĒĢśĻĖ░ ņĀäņØś ļģ╝ļ¼Ėņ£╝ļĪ£ ņ¦üņĀæņĀüņØĖ ņśłņĖĪļĀźņØä ņé┤ĒÄ┤ļ│╝ ņłśļŖö ņŚåņŚłļŗżļŖö ĒĢ£Ļ│äĻ░Ć ņ׳ļŗż. ņØ┤Ēøä Lamont and Stein(2004)ņØĆ 1995ļģäņŚÉņä£ 2002ļģäĻ╣īņ¦ĆņØś ļéśņŖżļŗź ņāüņן ĻĖ░ņŚģļōżņŚÉ ļīĆĒĢ£ Ļ│Ąļ¦żļÅä ņ×ÉļŻīļź╝ ļČäņäØĒĢśņŚ¼ ņ░©ņØĄĻ▒░ļלņØś ņĀ£ĒĢ£ņØ┤ ņ׳ņØä ļĢī Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉĻ░Ć ņŗ£ņןņĀäņ▓┤ņØś ņØ┤ļĪĀĻ░ĆņÖĆ ņŗ£ņןĻ░ĆņØś Ļ┤┤ļ”¼ļź╝ ĒĢ┤ņåīĒĢśļŖöļŹ░ ņ¢┤ļĀżņøĆņØ┤ ņĪ┤ņ×¼ĒĢ©ņØä ĻĘ£ļ¬ģĒĢśņśĆļŗż. Lynch et al.(2014)ņØĆ NYSE, ļéśņŖżļŗźņØä ĒżĒĢ©ĒĢ£ ļŗżņ¢æĒĢ£ ļ»ĖĻĄŁ ņŻ╝ņŗØ ņŗ£ņןņØä ļīĆņāüņ£╝ļĪ£ 2005ļģä 1ņøöļČĆĒä░ 2007ļģä 7ņøöĻ╣īņ¦ĆņØś ņØ╝ļ│ä Ļ│Ąļ¦żļÅä Ļ▒░ļלļ¤ēņØä ņĪ░ņé¼ĒĢśņśĆļŗż. ĒĢ┤ļŗ╣ ņŚ░ĻĄ¼ņŚÉņä£ļŖö Ļ│Ąļ¦żļÅä Ēł¼ņ×Éņ×ÉļōżņØ┤ ņŗ£ņן ņĀäļ░śņŚÉ ļīĆĒĢ£ ņĀĢļ│┤ļź╝ Ļ░Ćņ¦ĆĻ│Ā ņ׳ņ£╝ļ®░, ņĀäņ▓┤ Ļ│Ąļ¦żļÅä Ļ▒░ļלļ¤ēņØĆ ļ»Ėļל ņŗ£ņן ņłśņØĄļźĀņØä ņśłņĖĪĒĢĀ ņłś ņ׳ļŖö ņĀĢļ│┤ļź╝ ĒżĒĢ©ĒĢśĻ│Ā ņ׳ļŗżĻ│Ā ņŻ╝ņןĒĢśņśĆļŗż. ĻĘĖļ”¼Ļ│Ā ņĀäņ▓┤ Ļ│Ąļ¦żļÅä Ļ▒░ļלļ¤ēņØä ĒÖ£ņÜ®ĒĢśņŚ¼ ļ»Ėļל 5ņØ╝ņŚÉņä£ 20ņØ╝Ļ╣īņ¦ĆņØś ņŗ£ņן ņłśņØĄļźĀņŚÉ ļīĆĒĢ£ ņśłņĖĪļĀźņØä ņ”ØĻ░Ćņŗ£Ēé¼ ņłś ņ׳ņØīņØä ļ│┤ņśĆļŗż. Rapach et al.(2016)ņØĆ 2014ļģä 12ņøöļČĆĒä░ 2017ļģä 1ņøöĻ╣īņ¦Ć Ļ│Ąļ¦żļÅä Ļ▒░ļלļ¤ēņØä ņØ┤ņÜ®ĒĢśņŚ¼ Ļ│Ąļ¦żļÅä ņ¦Ćņłśļź╝ ĻĄ¼ņČĢĒĢśĻ│Ā S&P500 ņ┤łĻ│╝ ņłśņØĄļźĀņŚÉ ļīĆĒĢ£ ņśłņĖĪļĀźņØä Ļ▓ĆņĀĢĒĢśņśĆļŗż. ĒĢ┤ļŗ╣ ņŚ░ĻĄ¼ņŚÉņä£ļŖö Ļ│Ąļ¦żļÅä ņ¦ĆņłśĻ░Ć Welch and Goyal(2007)ņŚÉņä£ ņé¼ņÜ®ĒĢ£ 14Ļ░£ņØś ņśłņĖĪļ│ĆņłśņŚÉ ļ╣äĒĢ┤ ņ£ĀņØśĒĢśĻ▓ī ļåÆņØĆ ļé┤Ēæ£ļ│Ė ļ░Å ņÖĖĒæ£ļ│Ė ņśłņĖĪļĀźņØä Ļ░Ćņ¦Ćļ®░, ņ×Éņé░ļ░░ļČä ņĖĪļ®┤ņŚÉņä£ņØś ņä▒Ļ│╝ļÅä ņÜ░ņøöĒĢ©ņØä ĒÖĢņØĖĒ¢łļŗż. ļéśņĢäĻ░Ć Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉļōżņØ┤ ļ»Ėļל ņŗ£ņן ņĀäļ░śņØś ĒśäĻĖłĒØÉļ”äņŚÉ ļīĆĒĢ£ ņĀĢļ│┤ļź╝ Ļ░Ćņ¦ĆĻ│Ā ņ׳ļŖö ņĀĢļ│┤Ļ▒░ļלņ×Éņ×äņØä ĒÖĢņØĖĒĢśņśĆļŗż.

ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö ĒĢ£ĻĄŁ ņŻ╝ņŗØ ņŗ£ņן ņ┤łĻ│╝ ņłśņØĄļźĀņŚÉ ļīĆĒĢ£ Ļ│Ąļ¦żļÅä ņ¦ĆņłśņØś ņśłņĖĪļĀźņØä Ļ│äļ¤ēņĀüņ£╝ļĪ£ ĒÖĢņØĖĒĢśĻĖ░ ņ£äĒĢśņŚ¼ ļŗżņØīĻ│╝ Ļ░ÖņØĆ ņł£ņä£ļĪ£ ļČäņäØņØä ņ¦äĒ¢ēĒĢ£ļŗż. ņ▓½ņ¦Ė, ĒĢ£ĻĄŁ ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņן(KOSPI), KOSDAQņŗ£ņןņØä ĒżĒĢ©ĒĢ£ ĻĖłņ£Ą ņŗ£ņן ņĀäļ░śņØś Ļ│Ąļ¦żļÅä Ļ▒░ļלļ¤ēņØä Ļ│ĀļĀżĒĢśņŚ¼ ĒĢ£ĻĄŁņØś ņŗ£ņן Ļ│Ąļ¦żļÅä ņ¦Ćņłśļź╝ ĻĄ¼ņČĢĒĢ£ļŗż. ņØ┤ ļĢī Ļ│Ąļ¦żļÅä ņ¦ĆņłśļŖö ņŗ£ņן ņĀäņ▓┤ņØś Ļ│Ąļ¦żļÅä Ļ▒░ļלņŚÉ Ļ┤ĆĒĢ£ ņĀĢļ│┤ļź╝ ļŗ┤Ļ│Ā ņ׳ņ£╝ļ®░, ņŗ£ņןņØś ĒĢśļ░® ļ”¼ņŖżĒü¼ļź╝ ņĖĪņĀĢĒĢĀ ņłś ņ׳ņØä Ļ▓āņ£╝ļĪ£ ĻĖ░ļīĆļÉ£ļŗż. ļæśņ¦Ė, Ļ│Ąļ¦żļÅä ņ¦ĆņłśņØś ņśłņĖĪļĀźņØä Ļ▓Ćņ”ØĒĢśĻĖ░ ņ£äĒĢśņŚ¼ ņŗ£ņן ņłśņØĄļźĀ ņśłņĖĪņŚÉ ļäÉļ”¼ ņé¼ņÜ®ļÉśļŖö 13Ļ░£ņØś Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│Ćņłśļź╝ ĻĄ¼ņČĢĒĢ£ļŗż. ņģŗņ¦Ė, ĻĘĖļĀłņØĖņĀĖ ņØĖĻ│╝Ļ┤ĆĻ│ä ļČäņäØņØä ĒåĄĒĢ┤ ņŗ£ņן ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäĻ│╝ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII) Ļ░äņØś ņäĀĒ¢ēņä▒ņØä ĒÖĢņØĖĒĢ£ļŗż. ļäĘņ¦Ė, Welch and Goyal(2007)ņØś ņśłņĖĪĒÜīĻĘĆļČäņäØ ļ░®ļ▓ĢļĪĀņØä ļ░öĒāĢņ£╝ļĪ£ ļé┤Ēæ£ļ│ĖĻ│╝ ņÖĖĒæ£ļ│Ė ņśłņĖĪĒÜīĻĘĆļČäņäØņØä ņ¦äĒ¢ēĒĢśņŚ¼ Ļ│Ąļ¦żļÅä ņ¦ĆņłśņÖĆ ĻĖ░ņĪ┤ Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśļōżĻ│╝ ņןļŗ©ĻĖ░ ņśłņĖĪļĀźņØä ĒåĄĻ│äņĀüņ£╝ļĪ£ ļ╣äĻĄÉĒĢ£ļŗż. ļŗżņä»ņ¦Ė, ņŗ£ņן Ļ│Ąļ¦żļÅä ņ¦Ćņłś ņśłņĖĪļĀźņØś Ļ▓ĮņĀ£ĒĢÖņĀü ņØśņØśļź╝ ļČäņäØĒĢśĻĖ░ ņ£äĒĢśņŚ¼ Campbell and Thomson(2007)ņØś ļ░®ļ▓ĢļĪĀņØä ļ░öĒāĢņ£╝ļĪ£ ĒĢ£ ņ×Éņé░ļ░░ļČäņØä ņ¦äĒ¢ēĒĢśņŚ¼ Ļ│Ąļ¦żļÅä ņ¦ĆņłśņØś ņ×Éņé░ļ░░ļČä ņä▒Ļ│╝ļź╝ ĻĖ░ņĪ┤ Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśļōżĻ│╝ ļ╣äĻĄÉĒĢ£ļŗż. ļ¦łņ¦Ćļ¦ēņ£╝ļĪ£, Campbell(1991), Campbell and Ammer(1993)ņØś ļ▓ĪĒä░ņ×ÉĻĖ░ĒÜīĻĘĆ(VAR) ļ░®ļ▓ĢļĪĀņØä ĒÖ£ņÜ®ĒĢśņŚ¼ Ļ│Ąļ¦żļÅä ņ¦ĆņłśņØś ņŗ£ņןņśłņĖĪļĀźņŚÉ ļīĆĒĢ£ ĒĢĄņŗ¼ ļÅÖņØĖ(ÕŗĢÕøĀ)ņØä ļČäņäØĒĢ£ļŗż. ņØ┤ļź╝ ĒåĄĒĢ┤ Ļ│Ąļ¦żļÅä ņ¦ĆņłśņØś ņśłņĖĪļĀźņØ┤ ļ»Ėļל ĒśäĻĖł ĒØÉļ”ä ņĀĢļ│┤ņÖĆ ĒĢĀņØĖņ£© ņĀĢļ│┤ ņżæ ņ¢┤ļ¢ż ņĀĢļ│┤ ĻĖ░ņØĖĒĢ£ Ļ▓āņØĖņ¦Ć ĒÖĢņØĖĒĢĀ ņłś ņ׳ļŗż.

ļ│Ė ņŚ░ĻĄ¼ļŖö ņŗ£Ļ│äņŚ┤ļČäņäØĻ│╝ Ļ│äļ¤ēĻ▓ĮņĀ£ĒĢÖņĀü ĻĖ░ļ▓ĢņØä ņØ┤ņÜ®ĒĢśņŚ¼ ņĀäņ▓┤ Ļ│Ąļ¦żļÅä ņĀĢļ│┤Ļ░Ć ļŗ©ĻĖ░ ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņŚÉ ļīĆĒĢ£ ņóŗņØĆ ņśłņĖĪļĀźņØä Ļ░Ćņ¦äļŗżļŖö Ļ▓āņØä ļ│┤ņśĆļŗżļŖöļŹ░ ņØśņØśĻ░Ć ņ׳ļŗż. ļČäņäØ Ļ▓░Ļ│╝ ļé┤Ēæ£ļ│ĖĻ│╝ ņÖĖĒæ£ļ│Ė ļ¬©ļæÉņŚÉņä£ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ļŗ©ĻĖ░ ņśłņĖĪ ņä▒Ļ│╝Ļ░Ć ĻĖ░ņĪ┤ Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│Ćņłśļōżļ│┤ļŗż ĒåĄĻ│äņĀüņ£╝ļĪ£ ņÜ░ņłśĒĢśļ®░, ņ×Éņé░ļ░░ļČä ņĖĪļ®┤ņØś ņä▒Ļ│╝ļÅä ņÜ░ņøöĒĢ©ņØä ĒÖĢņØĖĒ¢łļŗż. ļśÉĒĢ£ ĻĖ░ņĪ┤ņØś ņśłņĖĪ ļ│ĆņłśļōżņØä ņŗ£ņן ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ ņČöņĀĢņ╣śļĪ£ ļ│Ėļŗżļ®┤ VAR ļČäņäØ Ļ▓░Ļ│╝ļŖö Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉĻ░Ć Ļ▓ĮņĀ£ ļé┤ņØś ļ»Ėļל ĒśäĻĖł ĒØÉļ”äņŚÉ ļīĆĒĢ£ ņé¼ņĀä ņĀĢļ│┤ļź╝ ĒÜŹļōØĒĢśĻ│Ā ņØ┤ļź╝ ņØ┤ņÜ®ĒĢśņŚ¼ ņØ┤ņØĄņØä ņĘ©ĒĢ£ļŗżļŖö Ļ▓āņØä ņØśļ»ĖĒĢ£ļŗż. ņØ┤ļ¤¼ĒĢ£ ļ░£Ļ▓¼ņØĆ Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉĻ░Ć ĻĖ░ņŚģ Ļ│Āņ£ĀņØś ņĀĢļ│┤ļź╝ ņØ┤ņÜ®ĒĢśņŚ¼ ņ┤łĻ│╝ ņłśņØĄņØä ņ¢╗ļŖöļŗżļŖö ĻĖ░ņĪ┤ ņŚ░ĻĄ¼ Ļ▓░Ļ│╝ļōżĻ│╝ ņØ╝ņ╣śĒĢśļŖö Ļ▓░Ļ│╝ņØ┤ļŗż(Akbas et al., 2013; Boehmer et al., 2008; Engelberg et al., 2012; Karpoff and Lou, 2010). ĻĘĖļ”¼Ļ│Ā ņĀĢļ│┤Ļ▒░ļלņ×ÉņØĖ Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉĻ░Ć ņŗ£ņן ņĀäņ▓┤ ĒśäĻĖł ĒØÉļ”äņŚÉ ļīĆĒĢ£ ņśłņĖĪņØä ĒåĄĒĢśņŚ¼ ņŗ£ņן ņĀäņ▓┤ņØś ļ»Ėļל ņøĆņ¦üņ×äņØä ņśłņĖĪĒĢśļ»ĆļĪ£, Ļ│Ąļ¦żļÅä Ļ▒░ļלņŚÉ ļŗ┤ĻĖ┤ ņĀĢļ│┤Ļ░Ć Ļ▓ĮņĀ£ ņĀäļ░śņØś ņĖĪļ®┤ņŚÉņä£ļÅä ņżæņÜöĒĢ£ ņÜöņåīņ×äņØä ņ”Øļ¬ģĒ¢łļŗżĻ│Ā ļ│╝ ņłś ņ׳ļŗż. ņóģĒĢ®ĒĢśļ®┤ Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉļōżņØĆ ļīĆļČĆļČä ļ»Ėļל ņŻ╝Ļ░Ć ņłśņØĄļźĀņŚÉ Ēü░ ņśüĒ¢źņØä ļ»Ėņ╣śļŖö ĒśäĻĖł ĒØÉļ”äņŚÉ ļīĆĒĢ£ ņśłņĖĪļĀźņØ┤ ņ׳ļŖö ņĀĢļ│┤Ļ▒░ļלņ×ÉļØ╝Ļ│Ā Ļ▓░ļĪĀ ļé┤ļ”┤ ņłś ņ׳ņ£╝ļ®░, ņØ┤ļŖö Miller(1977)ņØś ņĀĢļ│┤Ļ▒░ļלĻ░ĆņäżņØä ņ¦Ćņ¦ĆĒĢ£ļŗż.

ļ│Ė ņŚ░ĻĄ¼ņØś ĻĄ¼ņä▒ņØĆ ļŗżņØīĻ│╝ Ļ░Öļŗż. ņĀ£ 2ņןņŚÉņä£ļŖö ņŚ░ĻĄ¼ņŚÉ ĒÖ£ņÜ®ļÉśļŖö ļČäņäØņ×ÉļŻīļź╝ ņåīĻ░£ĒĢśĻ│Ā ņØ┤ļź╝ ĒåĀļīĆļĪ£ ļ│Ė ņŚ░ĻĄ¼ņØś ĒĢĄņŗ¼ ļ│ĆņłśņØĖ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņÖĆ ĻĖ░ņĪ┤ Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśļōżņØä ļÅäņČ£ĒĢ£ļŗż. ņĀ£ 3ņןņŚÉņä£ļŖö ņśłņĖĪĒÜīĻĘĆļČäņäØ, ņ×Éņé░ļ░░ļČäļČäņäØ, VAR ļō▒ņØś ļ░®ļ▓ĢļĪĀņØä ņäżļ¬ģĒĢ£ļŗż. ņĀ£ 4ņןņŚÉņä£ļŖö ļČäņäØ Ļ▓░Ļ│╝ļź╝ ĒÖĢņØĖĒĢśĻ│Ā ĒĢ┤ņäØĒĢ£ļŗż. ļ¦łņ¦Ćļ¦ēņ£╝ļĪ£ ņĀ£ 5ņןņŚÉņä£ļŖö ļ│Ė ņŚ░ĻĄ¼ņØś Ļ▓░ļĪĀņØä ņĀ£ņŗ£ĒĢśĻ│Ā ĒĢ£ĻĄŁ ņŗ£ņןņŚÉņä£ Ļ│Ąļ¦żļÅäņØś Ļ▓ĮņĀ£ņĀü ņØśļ»ĖņÖĆ ĻĘĖ ņŗ£ņé¼ņĀÉņŚÉ ļīĆĒĢ┤ ļģ╝ĒĢ£ļŗż.

2. Ļ│Ąļ¦żļÅä ņ¦ĆņłśņÖĆ ņśłņĖĪ ļ│Ćņłś

2.1 Ļ│Ąļ¦żļÅä ņ¦Ćņłś

ļ│Ė ņןņŚÉņä£ļŖö Miller(1977)ņÖĆ Diamond and Verrecchia(1987)ņØś ņĀĢļ│┤ Ļ▒░ļל Ļ░ĆņäżņŚÉ ĻĘ╝Ļ▒░ĒĢśņŚ¼, ĒĢ£ĻĄŁņŗ£ņןņØś Ļ░£ļ│äĻĖ░ņŚģņØś Ļ│Ąļ¦żļÅä ņ×öĻ│Āļź╝ ĒÖ£ņÜ®ĒĢ£ ņŗ£ņן Ļ│Ąļ¦żļÅä ņ¦Ćņłśļź╝ ĻĄ¼ņČĢĒĢ£ļŗż. 2008ļģä ņØ┤Ēøä ĒĢ£ĻĄŁĻ▒░ļלņåīņŚÉņä£ļŖö ļ¦żņøö Ļ░£ļ│äĻĖ░ņŚģņØś Ļ│Ąļ¦żļÅä ņ×öĻ│Ā ņ×ÉļŻīļź╝ Ļ│ĄĻ░£ĒĢśĻ│Ā ņ׳ņ£╝ļ®░, ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö DataGuideņŚÉņä£ ņĀ£Ļ│ĄĒĢśļŖö 2008ļģä 6ņøöļČĆĒä░ 2016ļģä 8ņøöĻ╣īņ¦ĆņØś ņøöļ│ä Ļ│Ąļ¦żļÅä ņ×ÉļŻīļź╝ ņØ┤ņÜ®ĒĢśņśĆļŗż. ļČäņäØ ļīĆņāüņŚÉļŖö KOSPI ļ░Å KOSDAQ ņāüņןĻĖ░ņŚģ, ETFs(Exchange trading funds), ļ”¼ņĖĀ(Real Estate Investment Trusts, REITs)ļź╝ ĒżĒĢ©ĒĢśņśĆĻ│Ā, ļČäņäØ ĻĖ░Ļ░äņØĆ 2008ļģä 6ņøöļČĆĒä░ 2017ļģä 8ņøöĻ╣īņ¦ĆņØ┤ļŗż. ņŗ£ņן Ļ│Ąļ¦żļÅä ņ¦ĆņłśļŖö ļŗżņØīĻ│╝ Ļ░ÖņØ┤ ĻĄ¼ĒĢĀ ņłś ņ׳ļŗż.

ņŚ¼ĻĖ░ņä£ ViļŖö Ļ░£ļ│äĻĖ░ņŚģņØś ņŗ£Ļ░Ćņ┤ØņĢĪ, SiļŖö Ļ░£ļ│äĻĖ░ņŚģņØś Ļ│Ąļ¦żļÅä ņ×öĻ│Ā, NiļŖö Ļ░£ļ│äĻĖ░ņŚģņØś ļ░£Ē¢ēņŻ╝ņŗØņłśļź╝ ņØśļ»ĖĒĢ£ļŗż. ņŗ£ņן Ļ│Ąļ¦żļÅä ņ¦ĆņłśļŖö ĒĢ£ĻĄŁņŗ£ņןņŚÉ ņāüņןļÉśņ¢┤ ņ׳ļŖö ņĀäņ▓┤ ĻĖ░ņŚģņØś Ļ│Ąļ¦żļÅä Ļ▒░ļל ļ╣äņżæ(Ļ│Ąļ¦żļÅä ņ×öĻ│Ā/ļ░£Ē¢ēņŻ╝ņŗØņłś)ņŚÉ ļīĆĒĢ£ ņŗ£Ļ░Ćņ┤ØņĢĪĻĖ░ņżĆ Ļ░ĆņżæĒÅēĻĘĀņØä ļĪ£ĻĘĖ ļ│ĆĒÖśĒĢśņŚ¼ ĻĄ¼ņä▒ĒĢśņśĆļŗż. ļö░ļØ╝ņä£ Ļ│Ąļ¦żļÅä ņ¦ĆņłśļŖö ņŻ╝ņŗØņŗ£ņןļ┐Éļ¦ī ņĢäļŗłļØ╝ ETF, ļ”¼ņĖĀ ļō▒ ļŗżņ¢æĒĢ£ ĻĖłņ£Ąņŗ£ņןņØś Ļ│Ąļ¦żļÅä ņĀĢļ│┤ļź╝ ļŗ┤Ļ│Ā ņ׳ļŗż. Ļ│╝Ļ▒░ņŚÉļŖö ĒĢ£ĻĄŁņŗ£ņןņŚÉņä£ ņŻ╝ņŗØ ļīĆļ╣ä ETFļéś ļ”¼ņĖĀņØś ņŗ£ņןĻĘ£ļ¬©Ļ░Ć ņ×æņĢä ļČäņäØļīĆņāüņŚÉ ĒżĒĢ©ĒĢśņ¦Ć ņĢŖļŖö Ļ▓ĮņÜ░Ļ░Ć ļ¦ÄņĢśņ£╝ļéś ņĄ£ĻĘ╝ ļīĆņ▓┤ ņ×Éņé░ņØś ņłśņÜöņÖĆ ņāüņŖ╣ņäĖļź╝ Ļ│ĀļĀżĒĢśņŚ¼ ļČäņäØļīĆņāüņŚÉ ĒżĒĢ©ĒĢśņśĆļŗż. ĒŖ╣Ē׳, ĒĢ£ĻĄŁ ETF ņŗ£ņןņØś ņł£ņ×Éņé░ņ┤ØņĢĪņØĆ ņäĖĻ│ä 10ņ£ä ņłśņżĆņØ┤ļ®░, ņØ╝ĒÅēĻĘĀĻ▒░ļלļīĆĻĖłņØĆ ņäĖĻ│ä 5ņ£äņØ┤ļŗż.1) ļśÉĒĢ£, ETF ņŗ£ņןņØĆ 15ļģäĻ░ä ņł£ņ×Éņé░ ĻĘ£ļ¬©Ļ░Ć 89ļ░░ ņä▒ņןĒĢśņśĆņ£╝ļ®░, Ļ░£ņØĖĒł¼ņ×Éņ×Éļ│┤ļŗż ĻĖ░Ļ┤ĆĒł¼ņ×Éņ×ÉņØś ļ╣äņżæņØ┤ ļåÆļŗż. ņØ┤ļ¤¼ĒĢ£ ņĖĪļ®┤ņØä Ļ│ĀļĀżĒĢśņśĆņØä ļĢī, ETF ņŗ£ņןņØĆ ņĀĢļ│┤Ļ▒░ļלņ×ÉņØś ļ╣äņżæņØ┤ ņāüļīĆņĀüņ£╝ļĪ£ ļåÆņØä Ļ▓āņ£╝ļĪ£ ĒīÉļŗ©ļÉ£ļŗż.

<ĻĘĖļ”╝ 1>ņØĆ 2008ļģä 6ņøöņŚÉņä£ 2017ļģä 8ņøöĻ╣īņ¦ĆņØś ņŗ£ņן Ļ│Ąļ¦żļÅä ņ¦ĆņłśņØ┤ļ®░, ĒĢ£ĻĄŁ ņŗ£ņן ņĀäļ░śņØś Ļ│Ąļ¦żļÅä Ļ▒░ļל ņČöņØ┤ļź╝ ļéśĒāĆļéĖļŗż. ĒĢ£ĻĄŁņŗ£ņןņØś Ļ▓ĮņÜ░, Ļ│╝Ļ▒░ 2ņ░©ļĪĆņØś Ļ│Ąļ¦żļÅä ĻĖłņ¦ĆĻĖ░Ļ░äņØ┤ ņ׳ņŚłļŗż. ņ▓½ņ¦Ė, 2008ļģä ĻĖłņ£Ąņ£äĻĖ░ ĻĄŁļ®┤ņŚÉ Ļ│Ąļ¦żļÅä ņ¦ĆņłśĻ░Ć ĻĖēļō▒ĒĢśļŗż ĒĢśļØĮĒĢśļŖö Ļ▓āņØä ĒÖĢņØĖĒĢĀ ņłś ņ׳ļŖöļŹ░, ĻĖĆļĪ£ļ▓ī ĻĖłņ£Ąņ£äĻĖ░ ļÅÖņĢł ĻĖłņ£Ąņ£äņøÉĒÜīĻ░Ć 2008ļģä 10ņøöņŚÉņä£ 2009ļģä 5ņøöĻ╣īņ¦Ć Ļ│Ąļ¦żļÅäļź╝ ĻĖłņ¦ĆĒĢśņśĆĻĖ░ ļĢīļ¼ĖņØ┤ļŗż.2) ļæśņ¦Ė, 2011ļģä 6ņøö ĻĄŁļ®┤ņŚÉņä£ļÅä Ļ│Ąļ¦żļÅä ņ¦ĆņłśĻ░Ć ņ”ØĻ░ĆĒĢśļŗż Ļ░ĆĒīīļź┤Ļ▓ī ĒĢśļØĮĒĢśļŖö Ļ▓āņØä ĒÖĢņØĖĒĢĀ ņłś ņ׳ļŗż. ņØ┤ļŖö 2011ļģä 8ņøö ņ£ĀļĪ£ņĪ┤ ņ×¼ņĀĢņ£äĻĖ░ ĒÖĢņé░, ļ»ĖĻĄŁņØś Ļ▓ĮĻĖ░ļæöĒÖö ļ░Å ņŗĀņÜ®ļō▒ĻĖē ĒĢśļØĮ ļō▒ņ£╝ļĪ£ ĻĄŁļé┤ KOSPI ņ¦ĆņłśĻ░Ć ĻĖēĻ▓®Ē׳ ĒĢśļØĮĒ¢łĻĖ░ ļĢīļ¼Ėņ£╝ļĪ£ ĻĖłņ£Ąņ£äņøÉĒÜīļŖö 2011ļģä 8ņøöņŚÉņä£ 2011ļģä 11ņøöĻ╣īņ¦Ć 3Ļ░£ņøöĻ░ä KOSPI ļ░Å KOSDAQņŗ£ņןņŚÉ ļīĆĒĢ┤ Ļ│Ąļ¦żļÅäļź╝ ņĀäļ®┤ ĻĖłņ¦ĆĒĢśņśĆļŗż. ļö░ļØ╝ņä£, ĒĢ£ĻĄŁņŗ£ņןņØś Ļ▓ĮņÜ░ 2008ļģä 10ņøöļČĆĒä░ 8Ļ░£ņøöĻ░ä, 2011ļģä 8ņøöļČĆĒä░ 3Ļ░£ņøöĻ░ä Ļ│Ąļ¦żļÅäĻ░Ć ņĀäļ®┤ ĻĖłņ¦ĆļÉśņ¢┤ Ļ│Ąļ¦żļÅä ņ¦ĆņłśĻ░Ć 0ņŚÉ Ļ░ĆĻ╣Øļŗż.

<ĻĘĖļ”╝ 1>ņŚÉņä£ ņŗ£Ļ░äņŚÉ ļö░ļźĖ Ļ│Ąļ¦żļÅä ņ¦ĆņłśņØś ņäĀĒśĢ ņČöņäĖļź╝ ĒÖĢņØĖĒĢĀ ņłś ņ׳ļŖöļŹ░, ņØ┤ļ¤¼ĒĢ£ ņŗ£Ļ░ä ņČöņäĖĻ░Ć Ļ│Ąļ¦żļÅä ņĀĢļ│┤ļź╝ ņÖ£Ļ│ĪĒĢĀ ņłś ņ׳ņØīņØ┤ ņĢīļĀżņĀĖ ņ׳ļŗż.3) ĒĢ£ĻĄŁ ņŗ£ņןņŚÉņä£ Ļ│Ąļ¦żļÅä ņ¦ĆņłśĻ░Ć ņäĀĒśĢ ņČöņäĖļź╝ Ļ░¢ļŖö ņØ┤ņ£ĀļŖö Ēü¼Ļ▓ī ļæÉ Ļ░Ćņ¦ĆņØ┤ļŗż. ņ▓½ņ¦Ė, ņ×Éļ│Ėņŗ£ņןņØś ĻĘ£ļ¬©Ļ░Ć ņĀäņäĖĻ│äņĀüņ£╝ļĪ£ ņ╗żņ¦ÉņŚÉ ļö░ļØ╝, ņ”ØĻČīļīĆņ░©ņŗ£ņןņØ┤ ļ░£ņĀäĒĢśņśĆĻĖ░ ļĢīļ¼ĖņØ┤ļŗż. ņ”ØĻČīļīĆņ░©ņŗ£ņןņØś ļ░£ņĀäņØĆ Ļ│Ąļ¦żļÅä Ļ▒░ļלļ╣äņÜ®ņØä ļé«ņČöļŖö ņŚŁĒĢĀņØä ĒĢśņŚ¼, Ļ│Ąļ¦żļÅä ņ¦ĆņłśĻ░Ć ņŗ£Ļ░äņØ┤ ņ¦Ćļé©ņŚÉ ļö░ļØ╝ ņ”ØĻ░ĆĒĢ£ Ļ▓āņ£╝ļĪ£ ĒĢ┤ņäØĒĢĀ ņłś ņ׳ļŗż. ļæśņ¦Ė, ņäĀņ¦äĻĖłņ£ĄĻ▒░ļל ĻĖ░ļ▓ĢņØś ļ░£ņĀäņŚÉ ļö░ļØ╝ Ļ│Ąļ¦żļÅä Ļ▒░ļלņŚÉ ļīĆĒĢ£ ņłśņÜöĻ░Ć ņ”ØĻ░ĆĒĢśņśĆĻĖ░ ļĢīļ¼ĖņØ┤ļŗż. ņśłļź╝ ļōżļ®┤, ļĀłļ▓äļ”¼ņ¦ĆņÖĆ ļĪ▒-ņłÅ(long-short) ņĀäļץņØä Ļ│╝Ļ░ÉĒ׳ ĻĄ¼ņé¼ĒĢśļŖö ĒŚżņ¦ĆĒÄĆļō£ņØś ņ”ØĻ░ĆļĪ£ ņŗ£Ļ░äņØ┤ ņ¦Ćļé©ņŚÉ ļö░ļØ╝ Ļ│Ąļ¦żļÅä ņ¦ĆņłśĻ░Ć ņ”ØĻ░ĆĒĢ£ Ļ▓āņ£╝ļĪ£ ĒĢ┤ņäØĒĢĀ ņłś ņ׳ļŗż. ļö░ļØ╝ņä£, ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö ņŗØ (2)ņØś ļ¬©ĒśĢņØä ĒåĄĒĢ┤ ņŗ£Ļ░äņŚÉ ļö░ļźĖ ņäĀĒśĢ ņČöņäĖĻ░Ć ņĪ┤ņ×¼ĒĢśļŖöņ¦Ć ĒåĄĻ│äņĀüņ£╝ļĪ£ Ļ▓ĆņĀĢĒĢśņśĆļŗż. ņŚ¼ĻĖ░ņä£ RSIItļŖö ņäĀĒśĢ ņČöņäĖĻ░Ć ņĀ£Ļ▒░ļÉśņ¦Ć ņĢŖņØĆ ņŗ£ņן Ļ│Ąļ¦żļÅä ņ¦Ćņłśļź╝ ņØśļ»ĖĒĢ£ļŗż.

ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö ņĄ£ņåīņ×ÉņŖ╣ļ▓Ģ(OLS)ņ£╝ļĪ£ ņŗØ (2)ļź╝ ņČöņĀĢĒĢ£ Ēøä ņŗ£Ļ░ä ņČöņäĖļź╝ ņĀ£Ļ▒░ĒĢ£ ņ×öņ░©(u ^ t u ^ t

2.2 Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│Ćņłś

ļ│Ė ņןņŚÉņä£ļŖö ņŚ░ĻĄ¼ņŚÉņä£ ņé¼ņÜ®ĒĢ£ 13Ļ░Ćņ¦Ć Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśļōżņØä ņåīĻ░£ĒĢ£ļŗż. ĒĢ┤ļŗ╣ ļ│ĆņłśļōżņØĆ Welch and Goyal(2007)ņØä ļ╣äļĪ»ĒĢ£ ņŚ¼ļ¤¼ ņŗ£ņןņłśņØĄļźĀ ņśłņĖĪ ļ¼ĖĒŚīņŚÉņä£ ĒåĄņāüņĀüņ£╝ļĪ£ ĒÖ£ņÜ®ļÉśļŖö ļ│ĆņłśļōżņØ┤ļ®░, Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ņśłņĖĪļĀźĻ│╝ ĻĖ░ņĪ┤ ņŚ░ĻĄ¼Ļ▓░Ļ│╝ļź╝ ļ╣äĻĄÉĒĢśĻĖ░ ņ£äĒĢ£ ļ▓żņ╣śļ¦łĒü¼ļĪ£ ņé¼ņÜ®ļÉ£ļŗż. ņŻ╝ņŗØņŗ£ņןņØś Ļ░£ļ│ä ĻĖ░ņŚģņŚÉ Ļ┤ĆĒĢ£ ņĀĢļ│┤ļŖö DataGuide, ĻĖłļ”¼ ņĀĢļ│┤ņÖĆ ņåīļ╣äņ×É ļ¼╝Ļ░Ćņ¦ĆņłśļŖö ĒåĄĻ│äņ▓ŁņŚÉņä£ ņĀ£Ļ│Ąļ░øņĢśļŗż. Ļ░ü ļ│ĆņłśņŚÉ Ļ┤ĆĒĢ£ ĻĄ¼ņ▓┤ņĀüņØĖ ļÅäņČ£ ļ░®ļ▓ĢņØĆ ņĢäļלņÖĆ Ļ░Öļŗż.

1) ļĪ£ĻĘĖ ļ░░ļŗ╣-ņŻ╝Ļ░Ć ļ╣äņ£©(log dividend-price ratio, DP): KOSPI ņ¦ĆņłśņØś ļ░░ļŗ╣ņŚÉ ļīĆĒĢ£ 12Ļ░£ņøö ņØ┤ļÅÖĒĢ®(moving sum)ņØä Ēśäņ×¼ ņŗ£ņĀÉņØś KOSPI ņ¦ĆņłśļĪ£ ļéśļłł Ēøä ļĪ£ĻĘĖ ļ│ĆĒÖś. KOSPI ņ¦Ćņłś ļ░░ļŗ╣ņØĆ ĒĢ┤ļŗ╣ ņ¦ĆņłśņŚÉ ņåŹĒĢ£ Ļ░£ļ│ä ĻĖ░ņŚģņØś ļ░░ļŗ╣ņØä ņŗ£Ļ░Ćņ┤ØņĢĪņ£╝ļĪ£ Ļ░ĆņżæĒÅēĻĘĀĒĢśņŚ¼ ļÅäņČ£ĒĢ©.

2) ļĪ£ĻĘĖ ļ░░ļŗ╣ ņØ┤ņØĄļźĀ (log dividend yield, DY): KOSPI ņ¦ĆņłśņØś ļ░░ļŗ╣ņŚÉ ļīĆĒĢ£ 12Ļ░£ņøö ņØ┤ļÅÖĒĢ®ņØä ņØ┤ņĀä ņŗ£ņĀÉ KOSPI ņ¦ĆņłśļĪ£ ļéśļłł Ēøä ļĪ£ĻĘĖ ļ│ĆĒÖśĒĢ©.

3) ļĪ£ĻĘĖ ņØ┤ņØĄ-Ļ░ĆĻ▓® ļ╣äņ£© (log earnings-price ratio, EP): KOSPI ņ¦ĆņłśņØś ņØ┤ņØĄ(earnings)ņŚÉ ļīĆĒĢ£ 12Ļ░£ņøö ņØ┤ļÅÖĒĢ®ņØä Ēśäņ×¼ ņŗ£ņĀÉņØś KOSPI ņ¦ĆņłśļĪ£ ļéśļłł Ēøä ļĪ£ĻĘĖ ļ│ĆĒÖś. KOSPI ņ¦ĆņłśņØś ņØ┤ņØĄņØĆ ĒĢ┤ļŗ╣ ņ¦ĆņłśņŚÉ ņåŹĒĢ£ Ļ░£ļ│ä ĻĖ░ņŚģņØś ņØ┤ņØĄņØä ņŗ£Ļ░Ćņ┤ØņĢĪņ£╝ļĪ£ Ļ░ĆņżæĒÅēĻĘĀĒĢśņŚ¼ ļÅäņČ£ĒĢ©.

4) ļĪ£ĻĘĖ ļ░░ļŗ╣ņä▒Ē¢ź(log dividend-payout ratio, DE): KOSPI ņ¦ĆņłśņØś ļ░░ļŗ╣ņŚÉ ļīĆĒĢ£ 12Ļ░£ņøö ņØ┤ļÅÖĒĢ®ņØä KOSPI ņ¦ĆņłśņØś ņØ┤ņØĄņŚÉ ļīĆĒĢ£ 12Ļ░£ņøö ņØ┤ļÅÖĒĢ®ņ£╝ļĪ£ ļéśļłł Ēøä ļĪ£ĻĘĖ ļ│ĆĒÖśĒĢ©.

5) ņ┤łĻ│╝ ņŻ╝Ļ░Ć ņłśņØĄ ļ│ĆļÅÖņä▒(Excess stock return volatility, RVOL): ņ┤łĻ│╝ ņŻ╝Ļ░Ć ņłśņØĄņØś 12Ļ░£ņøö ņØ┤ļÅÖ Ēæ£ņżĆĒÄĖņ░©(Mele, 2007).

6) ņןļČĆĻ░Ć-ņŗ£Ļ░Ć ļ╣äņ£©(Book-to-market ratio, BM): KOSPI ņ¦ĆņłśņŚÉ ņåŹĒĢ£ Ļ░£ļ│ä ĻĖ░ņŚģņØś ņןļČĆĻ░Ć-ņŗ£Ļ░Ć ļ╣äņ£©ņØä ņŗ£Ļ░Ćņ┤ØņĢĪņ£╝ļĪ£ Ļ░ĆņżæĒÅēĻĘĀ.

7) ņł£ņ×Éņé░ĒÖĢļīĆ(Net equity expansion, NTIS): ņł£ņ×Éņé░ĒÖĢļīĆļŖö KOSPIņāüņן ĻĖ░ņŚģļōżņØś ņł£ņ×Éņé░ ņ”ØĻ░Ćļ¤ēņØä ņĖĪņĀĢĒĢśļŖö ļ│ĆņłśļĪ£ņŹ©, KOSPI ņ¦ĆņłśņŚÉ ņāüņןļÉ£ ņŻ╝ņŗØļōżņØś ņāüņן ņŻ╝ņŗØņłś ņł£ ņ”ØĻ░Ćļ¤ēņØś 12Ļ░£ņøö ņØ┤ļÅÖĒĢ®ņØä ņŚ░ļ¦É KOSPI ņ¦ĆņłśņØś ņĀäņ▓┤ ņŗ£Ļ░Ćņ┤ØņĢĪņ£╝ļĪ£ ļéśļłäņ¢┤ ĻĄ¼ĒĢ©.

8) ĻĄŁņ▒ä ņØ┤ņ×Éņ£©(Treasury bill rate, TBL): 1ļģä ĻĄŁĻ│Āņ▒ä ņØ┤ņ×Éņ£©.

9) ņןĻĖ░ ņØ┤ņ×Éņ£©(Long-term yield, LTY): 10ļģä ĻĄŁĻ│Āņ▒ä ņØ┤ņ×Éņ£©.

10) ĻĖłļ”¼ņŖżĒöäļĀłļō£(Term spread, TMS): 10ļģä ĻĄŁĻ│Āņ▒äņÖĆ 1ļģä ĻĄŁĻ│Āņ▒ä Ļ░äņØś ņØ┤ņ×Éņ£© ņ░©ņØ┤.

11) ļČĆļÅä ĻĖłļ”¼ ņŖżĒöäļĀłļō£(Default yield spread, DFY): BBB- ļō▒ĻĖēĻ│╝ AA- ļō▒ĻĖē ĒÜīņé¼ņ▒ä Ļ░ä ņØ┤ņ×Éņ£© ņ░©ņØ┤.

12) ņØĖĒöīļĀłņØ┤ņģś(Inflation, INFL): ņåīļ╣äņ×É ļ¼╝Ļ░Ć ņ¦Ćņłś(Consumer Price Index)ņØś ļ│ĆĒÖöņ£©.

ņśłņĖĪ ļ│ĆņłśļōżĻ│╝ Ļ│Ąļ¦żļÅä ņ¦Ćņłś Ļ░äņØś Ļ┤ĆĻ│äļź╝ ĒīīņĢģĒĢśĻĖ░ ņ£äĒĢ┤ ņÜöņĢĮ ĒåĄĻ│äļ¤ēĻ│╝ ļ│ĆņłśĻ░ä ņāüĻ┤ĆĻ┤ĆĻ│äļź╝ ĻĄ¼ĒĢśņśĆļŗż. <Ēæ£ 1>ņØś Ēī©ļäÉ AņŚÉļŖö Ļ░ü ļ│ĆņłśņŚÉ ļīĆĒĢ£ ĒÅēĻĘĀ, ņżæņĢÖĻ░Æ, Ēæ£ņżĆĒÄĖņ░©, 99 ĒŹ╝ņä╝ĒāĆņØ╝(99th percentile)Ļ│╝ 1 ĒŹ╝ņä╝ĒāĆņØ╝(1st percentile)ņØ┤ ņĀ£ņŗ£ļÉśņ¢┤ ņ׳ļŗż. <Ēæ£ 1> Ēī©ļäÉ AņØś ļ¦łņ¦Ćļ¦ē Ē¢ēĻ│╝ Ēī©ļäÉ Bļź╝ ļ│┤ļ®┤ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ĒÅēĻĘĀĻ░ÆņØĆ 0.0030, ņżæņĢÖĻ░ÆņØĆ 0.0027, 99 ĒŹ╝ņä╝ĒāĆņØ╝ Ļ░ÆņØĆ 0.0062ņØ┤Ļ│Ā ņŗ£Ļ░äņŚÉ ļö░ļØ╝ ĒÅēĻĘĀĻ░ÆņØ┤ ņĀÉņĀÉ ņ”ØĻ░ĆĒĢśļŖö Ļ▓āņØä ņĢī ņłś ņ׳ļŗż.

ļŗżņØīņ£╝ļĪ£ <Ēæ£ 2>ņŚÉļŖö ļ│ĆņłśĻ░ä ņāüĻ┤ĆĻ┤ĆĻ│ä ļÅäĒæ£Ļ░Ć ņĀ£ņŗ£ļÉśņ¢┤ ņ׳ņ£╝ļ®░ ĻĖ░ņĪ┤ Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśĻ░äņØś ņāüĻ┤ĆĻ┤ĆĻ│äĻ░Ć ņĀäļ░śņĀüņ£╝ļĪ£ ļåÆņØĆ Ļ▓āņØä ĒÖĢņØĖĒĢĀ ņłś ņ׳ļŗż. ĒŖ╣Ē׳ DPņÖĆ DYĻ░Ć 0.97ļĪ£ ļåÆņØĆ ņ¢æņØś ņāüĻ┤ĆĻ┤ĆĻ│äļź╝ ļ│┤ņØ┤Ļ│Ā EPņÖĆ DEĻ░Ć -0.56ļĪ£ ļåÆņØĆ ņØīņØś ņāüĻ┤ĆĻ┤ĆĻ│äļź╝ ļ│┤ņØ┤ļŖöļŹ░ ņØ┤ļ¤░ Ļ▓ĮņÜ░ ĒĢ┤ļŗ╣ ļ│ĆņłśļōżņØä ļÅģļ”Į ļ│ĆņłśļĪ£ ĒĢśņŚ¼ ļŗżņżæĒÜīĻĘĆļČäņäØ ĒĢĀ Ļ▓ĮņÜ░ ļ│ĆņłśĻ░ä ļŗżņżæ Ļ│ĄņäĀņä▒ ļ¼ĖņĀ£Ļ░Ć ļ░£ņāØĒĢĀ ņ£äĒŚśņØ┤ ņ׳ļŗż. ļ░śļ®┤, Ļ│Ąļ¦żļÅä ņ¦ĆņłśļŖö ņĀäļ░śņĀüņ£╝ļĪ£ ĻĖ░ņĪ┤ ļ│ĆņłśļōżĻ│╝ņØś ņāüĻ┤ĆĻ┤ĆĻ│äĻ░Ć ļé«ļŗż. ņĀłļīĆĻ░ÆņØä ĻĖ░ņżĆņ£╝ļĪ£ Ļ│Ąļ¦żļÅä ņ¦ĆņłśņÖĆ ņāüĻ┤ĆĻ┤ĆĻ│äĻ░Ć Ļ░Ćņן ļåÆņØĆ ļ│ĆņłśļŖö NTISņØ┤ļ®░(0.46), Ļ░Ćņן ļé«ņØĆ ļ│ĆņłśļŖö INFLņØ┤ļŗż(-0.02). ņ”ē Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ļŖö ĻĖ░ņĪ┤ Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśņÖĆ ļŗżļźĖ ĒŖ╣ļ│äĒĢ£ ņĀĢļ│┤ļź╝ Ļ░Ćņ¦ĆĻ│Ā ņ׳ņØä Ļ░ĆļŖźņä▒ņØ┤ ņ׳ļŗż.

3. ļČäņäØ ļ░®ļ▓ĢļĪĀ

3.1 ņśłņĖĪĒÜīĻĘĆļČäņäØ

3.1.1 ļé┤Ēæ£ļ│Ė ļČäņäØ

Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņÖĆ ļ»Ėļל ņŻ╝Ļ░ĆņłśņØĄļźĀ Ļ░äņØś Ļ┤ĆĻ│äļź╝ ĒåĄĻ│äņĀüņ£╝ļĪ£ Ļ▓Ćņ”ØĒĢśĻĖ░ ņ£äĒĢśņŚ¼ ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö ļŗżņØī ņśłņĖĪĒÜīĻĘĆļČäņäØ ļ¬©ĒśĢņØä ņé¼ņÜ®ĒĢśņśĆļŗż.

ņŚ¼ĻĖ░ņä£ rt:t+hļŖö tņŗ£ņĀÉļČĆĒä░ t+hņŗ£ņĀÉĻ╣īņ¦ĆņØś KOSPI ņ┤łĻ│╝ņłśņØĄļźĀ ĒÅēĻĘĀ, xtļŖö ņśłņĖĪ ļ│Ćņłśļź╝ ņØśļ»ĖĒĢ£ļŗż. r t + 1 f

ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņŚÉ ļīĆĒĢ£ ņśłņĖĪļĀźņØä ļ╣äĻĄÉĒĢśĻĖ░ ņ£äĒĢśņŚ¼ Welch and Goyal(2007)ņØś Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśļōżĻ│╝ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ļź╝ ņäżļ¬ģ ļ│ĆņłśļĪ£ ĒĢśņŚ¼ ļŗ©ļ│Ćļ¤ē ņśłņĖĪĒÜīĻĘĆļČäņäØņØä ņ¦äĒ¢ēĒĢśņśĆļŗż. ļČäņäØ ĻĖ░Ļ░äņØĆ 2008ļģä 6ņøöļČĆĒä░ 2017ļģä 8ņøöĻ╣īņ¦ĆņØ┤Ļ│Ā, ņøöļ│ä(h = 1), ļČäĻĖ░ļ│ä(h = 3), ļ░śĻĖ░ļ│ä(h = 6), 9Ļ░£ņøöļ│ä(h = 9), ņŚ░ļ│ä(h = 12)ļĪ£ ļéśļłäņ¢┤ Ļ░ü ņśłņĖĪļ│ĆņłśņØś ╬▓ļź╝ ņČöņĀĢĒĢśņśĆļŗż. ņśłņĖĪļ│ĆņłśļōżņØś Ēæ£ņżĆĒÄĖņ░©ļź╝ 1ļĪ£ ĒåĄņØ╝ĒĢśĻĖ░ ņ£äĒĢ┤, Ļ░ü ņśłņĖĪļ│ĆņłśņØś Ēæ£ņżĆĒÄĖņ░©ļĪ£ ļéśļłäņ¢┤ Ēæ£ņżĆĒÖöĒĢśņśĆļŗż.

ļŗ©ļ│Ćļ¤ē ĒÜīĻĘĆļ¬©ĒśĢņŚÉņä£ ņóģņåŹļ│Ćņłśļź╝ ņäżļ¬ģĒĢśļŖöļŹ░ ĒĢäņÜöĒĢ£ ļ│Ćņłśļź╝ ĒżĒĢ©ĒĢśņ¦Ć ņĢŖņØĆ Ļ▓ĮņÜ░ ļŗżļźĖ ņäżļ¬ģļ│ĆņłśņØś Ļ│äņłśĻ░Ć Ļ│╝ļīĆ Ēś╣ņØĆ Ļ│╝ņåī ņČöņĀĢļÉĀ ņ£äĒŚś(ļłäļØĮ ļ│Ćņłś ĒÄĖņØś, Omitted variable bias)ņØ┤ ņ׳ļŗż. ņØ┤ņÖĆ Ļ░ÖņØĆ ļ¼ĖņĀ£ļź╝ ĒåĄņĀ£ĒĢśĻ│Āņ×É ļŗżņØīĻ│╝ Ļ░ÖņØĆ ĒÜīĻĘĆļ¬©ĒśĢņØä ņäĖņøī ņśłņĖĪ ĒÜīĻĘĆļČäņäØņØä ņŗżņŗ£ĒĢśņśĆļŗż.

ņŚ¼ĻĖ░ņä£ PC1,t, PC2,t, PC3,tļŖö Ļ░üĻ░ü ņŻ╝ņä▒ļČä ļČäņäØņØä ĒåĄĒĢśņŚ¼ ĻĄ¼ĒĢ£ ņ▓½ ļ▓łņ¦Ė, ļæÉ ļ▓łņ¦Ė, ņäĖ ļ▓łņ¦Ė ņä▒ļČäņØ┤ļŗż(Welch and Goyal, 2007). Ludvigson and Ng(2007)ņØś ņŚ░ĻĄ¼Ļ▓░Ļ│╝ņŚÉ ļö░ļź┤ļ®┤, ņŻ╝ņä▒ļČä ļČäņäØņØĆ ņäżļ¬ģ ļ│ĆņłśĻ░Ć ļ¦ÄņØĆ ņśłņĖĪ ĒÜīĻĘĆļČäņäØņØä ņŗżņŗ£ĒĢĀ ļĢī ĒÜ©Ļ│╝ņĀüņØĖ ņ░©ņøÉ ņČĢņåīļ░®ļ▓ĢļĪĀņØ┤ļŗż.

ļ¦łņ¦Ćļ¦ēņ£╝ļĪ£, Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│Ćņłś ņÖĖņØś ĻĖ░ņŚģĒŖ╣ņä▒ ļ░Å ņŗ£ņן ņÜöņØĖņØä ĒżĒĢ©ĒĢśņŚ¼ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ņśłņĖĪļĀźņØä Ļ▓Ćņ”ØĒĢśņśĆļŗż. Fama and French(1992), Carhart(1997)ņØś ļ░®ļ▓ĢļĪĀņŚÉ ļö░ļØ╝ ņŗ£ņן(MKT), ĻĖ░ņŚģĻĘ£ļ¬©(SMB), Ļ░Ćņ╣ś(HML), ļ¬©ļ®śĒģĆ(MOM) ņÜöņØĖņØä ĒżĒĢ©ĒĢ£ ņŗØ (6)ņØś ĒÜīĻĘĆļ¬©ĒśĢņØä ļČäņäØĒĢśņśĆļŗż.

3.1.2 ņÖĖĒæ£ļ│Ė ļČäņäØ

ļ│Ė ņןņŚÉņä£ļŖö Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņÖĆ Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśņØś ņśłņĖĪļĀźņØä ļ╣äĻĄÉĒĢśĻĖ░ ņ£äĒĢ£ ņÖĖĒæ£ļ│Ė ļČäņäØ ļ░®ļ▓ĢļĪĀņØä ņåīĻ░£ĒĢ£ļŗż. Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ļéś Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśĻ░Ć ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņŚÉ ļīĆĒĢ┤ ņ£ĀņØśĒĢ£ ņśłņĖĪļĀźņØä Ļ░¢ļŖöļŗżļ®┤, ņĀüņ¢┤ļÅä ņśłņĖĪļ│ĆņłśņØś ņĀĢļ│┤ļź╝ ņĀäĒśĆ ĒÖ£ņÜ®ĒĢśņ¦Ć ņĢŖļŖö Ļ│╝Ļ▒░ĒÅēĻĘĀļ¬©ĒśĢļ│┤ļŗż ņśłņĖĪļĀźņØ┤ ļåÆņØä Ļ▓āņØ┤ļŗż. ĻĘĖļ¤¼ļéś, Welch and Goyal(2007)ņØĆ ļé┤Ēæ£ļ│ĖņŚÉņä£ ņ£ĀņØśĒĢ£ ņśłņĖĪļĀźņØä Ļ░¢ļŖö ļ│ĆņłśņØ╝ņ¦ĆļØ╝ļÅä ņÖĖĒæ£ļ│ĖņŚÉņä£ Ļ│╝Ļ▒░ĒÅēĻĘĀļ¬©ĒśĢļ│┤ļŗż ņśłņĖĪļĀźņØ┤ ļ¢©ņ¢┤ņ¦ł ņłś ņ׳ņØīņØä ņŗżņ”ØņĀüņ£╝ļĪ£ ļ│┤ņśĆļŗż. ņÖĖĒæ£ļ│Ė ļČäņäØņØĆ Welch and Goyal(2007)ņØ┤ ņĀ£ņŗ£ĒĢ£ ļ░®ļ▓ĢņØä ļö░ļØ╝ ņ¦äĒ¢ēĒĢśņśĆļŗż. ĻĄ¼ņ▓┤ņĀüņØĖ ļČäņäØ ļ░®ļ▓ĢļĪĀņØĆ ļŗżņØīĻ│╝ Ļ░Öļŗż.

1) tņŗ£ņĀÉ ņśłņĖĪ ļ│ĆņłśļĪ£ ļŗżņØīņØś ļæÉ ņśłņĖĪ ĒÜīĻĘĆ ļ¬©ĒśĢņØä ņČöņĀĢĒĢ£ļŗż. ļŗ©, H M t ^

ņŚ¼ĻĖ░ņä£ ņŗØ (7)ņØĆ ņśłņĖĪ ļ│Ćņłśļź╝ ĒÖ£ņÜ®ĒĢ£ ĒÜīĻĘĆ ļ¬©ĒśĢņØ┤Ļ│Ā ņŗØ (8)ņØś Null ModelņØĆ Model AņŚÉņä£ ĻĖ░ņÜĖĻĖ░Ļ░Ć 0ņØĖ ļ¬©ĒśĢņ£╝ļĪ£, ņśłņĖĪ ļ│ĆņłśņØś ņĀĢļ│┤ļź╝ ņĀäĒśĆ ņé¼ņÜ®ĒĢśņ¦Ć ņĢŖņØĆ ĒÜīĻĘĆ ļ¬©ĒśĢ(Ļ│╝Ļ▒░ĒÅēĻĘĀļ¬©ĒśĢ)ņØä ņØśļ»ĖĒĢ£ļŗż.

2) ņ£ä ļ¬©ĒśĢņŚÉņä£ ņČöņĀĢļÉ£ ╬▒ t ^ ╬▓ t ^ H M t ^

3) Ļ│╝ņĀĢ 1)~2)ļź╝ TŌłÆhļ▓ł ļ░śļ│ĄĒĢśņŚ¼ ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņŚÉ ļīĆĒĢ£ ņśłņĖĪ ņŗ£Ļ│äņŚ┤ r t + 1 A ^ r t + 1 N u l l ^

4) ļ»Ėļל ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņŚÉ ļīĆĒĢ£ ļæÉ ņśłņĖĪ ņŗ£Ļ│äņŚ┤(r t + 1 A ^ r t + 1 N u l l ^

5) Campbell and Thompson(2007)ņØś ļ░®ļ▓ĢņŚÉ ļö░ļØ╝ ņÖĖĒæ£ļ│Ė R O S 2

ļ¦īņĢĮ R O S 2

6) R O S 2

ņŚ¼ĻĖ░ņä£ TļŖö Ļ┤ĆņĖĪņ╣śņØś ņłś, hļŖö ņśłņĖĪ ĻĖ░Ļ░äņØä ļéśĒāĆļéĖļŗż. ĒĢ┤ļŗ╣ Ļ▓ĆņĀĢņØś ĻĘĆļ¼┤Ļ░ĆņäżņØĆ ņśłņĖĪĒÜīĻĘĆļ¬©ĒśĢņØś ņśłņĖĪļĀźņØ┤ Ļ│╝Ļ▒░ĒÅēĻĘĀļ¬©ĒśĢļ│┤ļŗż ļé«Ļ▒░ļéś Ļ░Öļŗż(H 0 : R O S 2 Ōēż 0 H A : R O S 2 > 0

3.2 ņ×Éņé░ļ░░ļČä ļČäņäØ

ļ│Ė ņןņŚÉņä£ļŖö ņ×Éņé░ļ░░ļČäņØś ņĖĪļ®┤ņŚÉņä£ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś Ļ▓ĮņĀ£ņĀü Ļ░Ćņ╣śļź╝ ĒÅēĻ░ĆĒĢśĻĖ░ ņ£äĒĢ┤ Campbell and Thompson(2007)ņØś ņĀłņ░©ņŚÉ ļö░ļØ╝ ņ£äĒŚśņ×Éņé░Ļ│╝ ļ¼┤ņ£äĒŚśņ×Éņé░ņØä ļ░░ļČäĒĢśļŖö ĒÅēĻĘĀ-ļČäņé░ Ēł¼ņ×Éņ×Éļź╝ Ļ│ĀļĀżĒĢśņśĆļŗż. ņ×Éņé░ļ░░ļČä ĒÅēĻ░Ć ļ░®ļ▓ĢļĪĀņØĆ ļŗżņØīĻ│╝ Ļ░Öļŗż.

1) tņŗ£ņĀÉ ņśłņĖĪ ļ│Ćņłśļź╝ ĒÖ£ņÜ®ĒĢśņŚ¼ ļŗżņØīņØś ņśłņĖĪ ĒÜīĻĘĆ ļ¬©ĒśĢņØä ņČöņĀĢĒĢ£ļŗż:

2) ņ£ä ļ¬©ĒśĢņŚÉņä£ ņČöņĀĢļÉ£ ╬▒ ^ t ╬▓ ^ t

t+1ņŗ£ņĀÉ ņśłņĖĪ ņłśņØĄļźĀ r t + 1 ^ = ╬▒ ^ t + ╬▓ ^ t x t

t+1 ņŗ£ņĀÉ ņśłņĖĪ ļČäņé░ Žā t + 1 2 ^

3) ņČöņĀĢļÉ£ KOSPI ņ¦ĆņłśņØś ņśłņĖĪ ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäĻ│╝ ņśłņĖĪ ļČäņé░ņØä Ļ│ĀļĀżĒĢĀ ļĢī t+1ņŗ£ņĀÉņØś ĒÅēĻĘĀ-ļČäņé░ Ēł¼ņ×Éņ×ÉĻ░Ć ļ│┤ņ£ĀĒĢĀ ņĄ£ņĀü ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö ļŗżņØīĻ│╝ Ļ░Öļŗż.

ņŚ¼ĻĖ░ņä£ ╬│ļŖö Ēł¼ņ×Éņ×ÉņØś ņ£äĒŚśĒÜīĒö╝Ļ│äņłśļĪ£ ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö ĻĖ░ņĪ┤ ņŚ░ĻĄ¼ļōżĻ│╝ Ļ░ÖņØ┤ Ēł¼ņ×Éņ×ÉņØś ņ£äĒŚśĒÜīĒö╝Ļ│äņłśļź╝ 3ņ£╝ļĪ£ ņĀĢņØśĒĢśņśĆļŗż. ļśÉĒĢ£ ĻĄŁļé┤ Ļ│Ąļ¬©ĒÄĆļō£ņØś ļĀłļ▓äļ”¼ņ¦Ć ņĀ£ņĢĮņØä Ļ│ĀļĀżĒĢśņŚ¼ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ļ▓öņ£äļź╝ -0.3~1.3 ņé¼ņØ┤ļĪ£ ņäżņĀĢĒĢśņśĆļŗż.

4) t+1ņŗ£ņĀÉņŚÉ Ēł¼ņ×Éņ×ÉĻ░Ć ņŗżņĀ£ ņŗżĒśäĒĢ£ ņłśņØĄļźĀņØä ĻĄ¼ĒĢ£ļŗż.

5) Ļ│╝ņĀĢ 1)~4)ļź╝ t=TŌłÆhĻ╣īņ¦Ć ļ░śļ│ĄĒĢśņŚ¼, Ēł¼ņ×Éņ×ÉĻ░Ć ņŗżņĀ£ ņŗżĒśäĒĢ£ ņłśņØĄļźĀĻ│╝ ļČäņé░ņØä ĻĄ¼ĒĢ£ļŗż.

6) ņ×Éņé░ļ░░ļČäņØś ņä▒Ļ│╝ĒÅēĻ░ĆļŖö ņāżĒöä ļ╣äņ£©(Sharpe ratio)Ļ│╝ ĒÖĢņŗżņä▒ ļō▒Ļ░Ć ņłśņØĄļźĀ(Certainty equivalent return, CER)ņØä ĒÖ£ņÜ®ĒĢ£ļŗż.

ņŚ¼ĻĖ░ņä£ E[Rp]ļŖö ĒÅēĻ░ĆĒĢśĻ│Āņ×É ĒĢśļŖö ņ×äņØśņØś ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ļīĆņłśņØĄļźĀ, rfļŖö ļ¼┤ņ£äĒŚśņłśņØĄļźĀ, ĻĘĖļ”¼Ļ│Ā ŽāpļŖö ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś Ēæ£ņżĆĒÄĖņ░©ļź╝ ļéśĒāĆļéĖļŗż. ĒÖĢņŗżņä▒ ļō▒Ļ░Ć ņłśņØĄļźĀņØĆ ņ£äĒŚś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļ│┤ņ£ĀĒĢśļŖö ļīĆņŗĀ, Ēł¼ņ×Éņ×ÉĻ░Ć ĻĖ░Ļ║╝ņØ┤ ļ░øņĢäļōżņØ╝ ņłś ņ׳ļŖö ļ¼┤ņ£äĒŚś ņłśņØĄļźĀņØ┤ļŗż.

ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö Ēł¼ņ×Éņä▒Ļ│╝ĒÅēĻ░Ćļź╝ ņ£äĒĢ┤ Ļ│╝Ļ▒░ĒÅēĻĘĀļ¬©ĒśĢ(╬▓ = 0 ņØĖ ņśłņĖĪĒÜīĻĘĆļ¬©ĒśĢ)ņ£╝ļĪ£ ņČöņĀĢĒĢ£ ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚä(r t + 1 ^

ļśÉĒĢ£ ņןĻĖ░ ņśłņĖĪļĀźņØś Ļ▓ĮņĀ£ņĀü Ļ░Ćņ╣śļź╝ ĒÅēĻ░ĆĒĢśĻĖ░ ņ£äĒĢ┤ ļ”¼ļ░Ėļ¤░ņŗ▒ ĻĖ░Ļ░äņØä ņøöļ│ä, ļČäĻĖ░ļ│ä, ļ░śĻĖ░ļ│ä, 9Ļ░£ņøöļ│ä, ņŚ░ļ│äļĪ£ ļéśļłäņ¢┤ ļČäņäØĒĢśņśĆļŗż. ņśłļź╝ ļōżņ¢┤, ļČäĻĖ░ļ│ä ļ”¼ļ▓©ļ¤░ņŗ▒(h=3)ņØś Ļ▓ĮņÜ░, Ēł¼ņ×Éņ×ÉļŖö ļČäĻĖ░ļ¦ÉņŚÉ ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņŚÉ ļīĆĒĢ£ ņśłņĖĪĒÜīĻĘĆļ¬©ĒśĢņØä ĒÖ£ņÜ®ĒĢśņŚ¼ ļŗżņØī ļČäĻĖ░ņŚÉ Ēł¼ņ×ÉĒĢĀ ņ£äĒŚśņ×Éņé░Ļ│╝ ļ¼┤ņ£äĒŚśņ×Éņé░ņØś ļ╣äņżæņØä ņŚģļŹ░ņØ┤ĒŖĖĒĢ£ļŗż. ļ¦łņ░¼Ļ░Ćņ¦ĆļĪ£ Ēł¼ņ×Éņ×ÉļŖö Ļ░ü ļ”¼ļ▓©ļ¤░ņŗ▒ ĻĖ░Ļ░äņŚÉ ļ¦×ņČöņ¢┤ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ļ╣äņżæņØä ņŚģļŹ░ņØ┤ĒŖĖĒĢ£ļŗż.

4. Ļ▓░Ļ│╝ ļČäņäØ

4.1 ĻĘĖļĀłņØĖņĀĖ ņØĖĻ│╝Ļ┤ĆĻ│ä ļČäņäØ

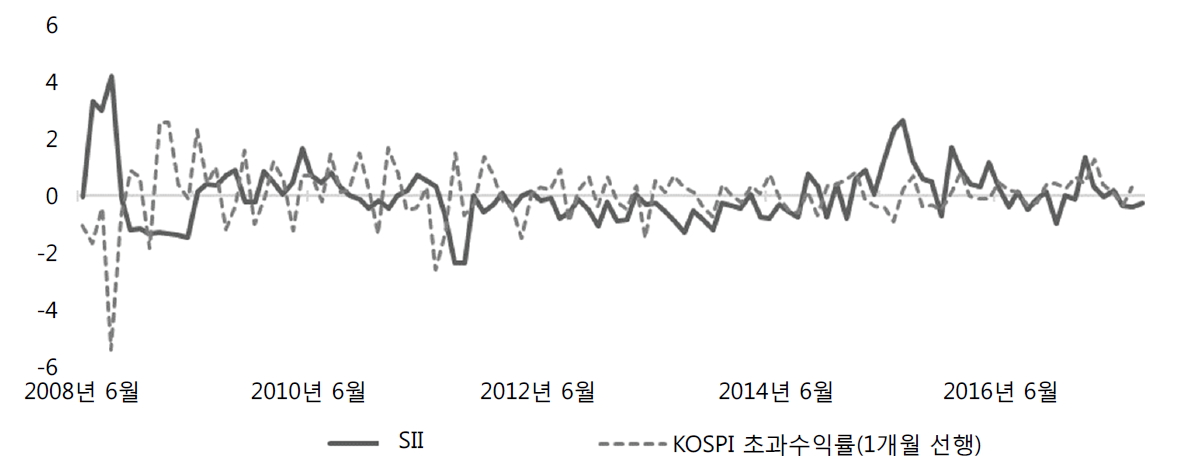

<Ēæ£ 3>ņØĆ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņÖĆ KOSPI ņ¦Ćņłś ņłśņØĄļźĀ Ļ░äņØś ĻĘĖļĀłņØĖņĀĖ ņØĖĻ│╝Ļ┤ĆĻ│äļź╝ ļČäņäØĒĢ£ Ļ▓░Ļ│╝ņØ┤ļŗż. <Ēæ£ 3>ņØś ņ▓½ ļ▓łņ¦Ė ņŚ┤ņØś ĻĘĆļ¼┤Ļ░ĆņäżņØĆ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)Ļ░Ć KOSPI ņ¦Ćņłś ņłśņØĄļźĀņØä ņäĀĒ¢ēĒĢśņ¦Ć ņĢŖļŖöļŗżļŖö Ļ▓āņØ┤ļ®░, ļīĆļ”ĮĻ░ĆņäżņØĆ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)Ļ░Ć KOSPI ņ¦Ćņłś ņłśņØĄļźĀņØä ņäĀĒ¢ēĒĢ£ļŗżļŖö Ļ▓āņØ┤ļŗż. ļČäņäØ Ļ▓░Ļ│╝, ņŗ£ņ░©Ļ░Ć 1Ļ░£ņøö, 2Ļ░£ņøö, 3Ļ░£ņøö, 4Ļ░£ņøöņØĖ Ļ▓ĮņÜ░ ņ£ĀņØśĒĢśĻ▓ī ĻĘĆļ¼┤Ļ░ĆņäżņØä ĻĖ░Ļ░üĒĢśņŚ¼ Ļ│Ąļ¦żļÅäņ¦ĆņłśĻ░Ć KOSPI ņ¦Ćņłś ņłśņØĄļźĀņØä ņäĀĒ¢ēĒĢśņ¦Ćļ¦ī ņŗ£ņ░©Ļ░Ć 5Ļ░£ņøöņØä ļäśņ¢┤Ļ░ł Ļ▓ĮņÜ░ ĻĘĆļ¼┤Ļ░ĆņäżņØä ĻĖ░Ļ░üĒĢĀ ņłś ņŚåņŚłļŗż. ņ”ē, Ļ│Ąļ¦żļÅä ņ¦Ćņłś (SII)ņØś KOSPI ņ¦Ćņłś ņłśņØĄļźĀ ļīĆĒĢ£ ņäĀĒ¢ēņä▒ņØĆ 4Ļ░£ņøö ņĀĢļÅä ņ£Āņ¦ĆļÉ£ļŗż. ņØ┤ļŖö Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉļōżņØ┤ ļ╣äĻĄÉņĀüņ£╝ļĪ£ ņ¦¦ņØĆ ĻĖ░Ļ░äņØś ņĀĢļ│┤ļź╝ ņØ┤ņÜ®ĒĢśņŚ¼ Ļ│Ąļ¦żļÅä Ļ▒░ļלļź╝ ĒĢśĻĖ░ ļĢīļ¼ĖņØ┤ļ®░, Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)Ļ░Ć ļŗ©ĻĖ░ ņśłņĖĪņŚÉ Ļ░ĢņĀÉņØä ļ│┤ņØ╝ Ļ▓āņØ┤ļØ╝Ļ│Ā ņśłņāüĒĢĀ ņłś ņ׳ļŗż.

<Ēæ£ 3>ņØś ļæÉ ļ▓łņ¦Ė ņŚ┤ņØś ĻĘĆļ¼┤Ļ░ĆņäżņØĆ KOSPI ņ¦Ćņłś ņłśņØĄļźĀņØ┤ Ļ│Ąļ¦żļÅä ņ¦Ćņłśļź╝ ņäĀĒ¢ēĒĢśņ¦Ć ņĢŖļŖöļŗżļŖö Ļ▓āņØ┤ļ®░, ļŗ©ĻĖ░ņŚÉņä£ļŖö ĻĘĆļ¼┤Ļ░ĆņäżņØä ĻĖ░Ļ░üĒĢśņ¦Ć ļ¬╗ĒĢ£ļŗż. ĒĢśņ¦Ćļ¦ī ņŗ£ņ░©Ļ░Ć 4, 5ņØĖ Ļ▓ĮņÜ░ ĻĘĆļ¼┤Ļ░ĆņäżņØä ĻĖ░Ļ░üĒĢśņŚ¼ KOSPI ņ¦Ćņłś ņłśņØĄļźĀņØ┤ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ļź╝ ņäĀĒ¢ēĒĢ£ļŗżļŖö Ļ▓āņØä ĒÖĢņØĖĒĢĀ ņłś ņ׳ņŚłļŗż. ņØ┤ Ļ▓░Ļ│╝ļŖö ļæÉ Ļ░Ćņ¦ĆļĪ£ ĒĢ┤ņäØĒĢĀ ņłś ņ׳ļŗż. ņ▓½ ļ▓łņ¦ĖļŖö ņŗ£ņןņŚÉ Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×Éļōż ņżæ ņØ╝ļČĆ ņČöņäĖņČöņóģņ×É(trend follower)ņØĖ ļ╣äņĀĢļ│┤Ļ▒░ļלņ×ÉĻ░Ć ņĪ┤ņ×¼ĒĢśņŚ¼ ņŻ╝Ļ░Ćņ¦ĆņłśņØś ņČöņäĖļź╝ ļ│┤Ļ│Ā ņØ╝ņĀĢ ņŗ£ņĀÉ ĒøäņŚÉ Ļ│Ąļ¦żļÅä Ļ▒░ļלļź╝ ņŗżĒ¢ēĒĢ£ļŗżļŖö ĒĢ┤ņäØņØ┤ļŗż. ļśÉ ļŗżļźĖ ĒĢ┤ņäØņØĆ ņŗ£ņן ņłśņØĄļźĀņØ┤ ņČ®ļČäĒ׳ ĒĢśļØĮĒĢ£ ņØ┤Ēøä Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉļōżņØ┤ Ļ│Ąļ¦żļÅäĒĢ£ ņŻ╝ņŗØņØä Ļ░ÜĻĖ░ ņ£äĒĢśņŚ¼ ņłÅņ╗żļ▓ä(Ļ│Ąļ¦żļÅä Ēżņ¦Ćņģś ņ▓Łņé░ņØä ņ£äĒĢ£ ņŻ╝ņŗØ ņ×¼ļ¦żņ×ģ)ĒĢĀ ļĢī Ļ│Ąļ¦żļÅä Ļ▒░ļלļ¤ēņØ┤ Ļ░ÉņåīĒĢśņŚ¼ ņŗ£ņן ņłśņØĄļźĀņØä ĒøäĒ¢ē ĒĢ£ļŗżļŖö Ļ▓āņØ┤ļŗż.

4.2 ļé┤Ēæ£ļ│Ė ņśłņĖĪĒÜīĻĘĆļČäņäØ Ļ▓░Ļ│╝

<Ēæ£ 4>ļŖö Ļ░ü ņśłņĖĪ ļ│ĆņłśļōżņØś ņśłņĖĪ ĻĖ░Ļ░äņŚÉ ļö░ļźĖ ļé┤Ēæ£ļ│Ė ņśłņĖĪĒÜīĻĘĆļČäņäØ Ļ▓░Ļ│╝ļź╝ ļéśĒāĆļéĖļŗż. Ļ░ü ņŚ┤ņŚÉļŖö 1Ļ░£ņøö(h = 1), 3Ļ░£ņøö(h = 3), 6Ļ░£ņøö(h = 6), 9Ļ░£ņøö(h = 9), 12Ļ░£ņøö(h = 12) ņśłņĖĪĒÜīĻĘĆļČäņäØņØś ╬▓ ņČöņĀĢņ╣śņÖĆ R2Ļ░ÆņØ┤ ņŻ╝ņ¢┤ņĀĖ ņ׳ļŗż. Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś 1Ļ░£ņøö ņśłņĖĪ Ļ▓░Ļ│╝ļź╝ ņé┤ĒÄ┤ļ│┤ļ®┤, ņśłņĖĪ ĒÜīĻĘĆ ļ¬©ĒśĢņØś ╬▓ ^

1Ļ░£ņøö ļŗ©ĻĖ░ ņśłņĖĪņØś Ļ▓ĮņÜ░ ļ│Ėņ¦łņĀüņ£╝ļĪ£ ņśłņĖĪļČłĻ░ĆļŖźĒĢ£ ņÜöņåīĻ░Ć ļ¦ÄņØ┤ ĒżĒĢ©ļÉśņ¢┤ ņ׳ņ¢┤ ņןĻĖ░ ņśłņĖĪĻ│╝ ļ╣äĻĄÉĒĢśļ®┤ R2Ļ░ÆņØ┤ ņāüļīĆņĀüņ£╝ļĪ£ ļé«ļŗż. Campbell and Thompson(2007)ļŖö ņøöļ│ä R2Ļ░ÆņØ┤ 0.5% ņØ┤ņāüņØ┤ļ®┤ Ļ▓ĮņĀ£ņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢ£ ņśłņĖĪļĀźņØä Ļ░¢ļŖöļŗżĻ│Ā ņŻ╝ņןĒĢśņśĆņ£╝ļ®░, Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś R2 Ļ░ÆņØĆ 11.10%ļĪ£ Ļ▓ĮņĀ£ņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢ£ Ļ░ÆņØ┤ļŗż. 3Ļ░£ņøöĻ│╝ 6Ļ░£ņøö ņśłņĖĪ Ļ▓░Ļ│╝ļź╝ ņé┤ĒÄ┤ļ│┤ļ®┤, Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ╬▓ ^

<Ēæ£ 4>ņØś PC+SII Ē¢ēņŚÉņä£ļŖö 3Ļ░Ćņ¦Ć ņŻ╝ņä▒ļČäņØä ĒåĄņĀ£ĒĢ£ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ņśłņĖĪĒÜīĻĘĆļČäņäØ Ļ▓░Ļ│╝ļź╝ ņĀ£ņŗ£ĒĢśĻ│Ā ņ׳ļŗż. Ļ▓░Ļ│╝ļź╝ ņé┤ĒÄ┤ļ│┤ļ®┤ 1Ļ░£ņøö, 3Ļ░£ņøö, 6Ļ░£ņøö ņśłņĖĪ ╬▓SII Ļ░ÆņØĆ Ļ░üĻ░ü -0.28, -0.22, -0.14ņØ┤Ļ│Ā, 1% ņŗĀļó░ņłśņżĆ ĒĢśņŚÉņä£ ņ£ĀņØśĒĢ£ Ļ░ÆņØ┤ļŗż.4) ļŗ©ĻĖ░ņŚÉņä£ ņןĻĖ░ļĪ£ Ļ░łņłśļĪØ ╬▓SII ņØś ņĀłļīĆĻ░ÆņØ┤ Ļ░ÉņåīĒĢśļŖöļŹ░, Ļ│Ąļ¦żļÅä Ļ▒░ļלļ¤ē ļ│ĆĒÖöņŚÉ ļö░ļźĖ ļ»Ėļל ņŗ£ņן ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņØś ļ░śņØæņä▒ņØ┤ Ļ░ÉņåīĒĢ©ņØä ņØśļ»ĖĒĢ£ļŗż. ļŗżņØīņ£╝ļĪ£ ņŻ╝ņä▒ļČäņØä ĒåĄņĀ£ĒĢśĻĖ░ ņĀäĒøäņØś Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII) ļ¬©ĒśĢ ņśłņĖĪ ĒÜīĻĘĆļČäņäØņØśR2 ļź╝ ļ╣äĻĄÉĒĢ┤ļ│┤ļ®┤ ļ│Ćņłś ĒåĄņĀ£ ņĀä Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ņäżļ¬ģļĀźņØĆ ļŗ©ĻĖ░(R2 =11.10%)ņŚÉņä£ ņןĻĖ░(R2 =0.4%)ļĪ£ Ļ░łņłśļĪØ Ēü¼Ļ▓ī Ļ░ÉņåīĒĢśļŖö ļ░śļ®┤, Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│Ćņłśļź╝ ĒżĒĢ©ĒĢ£ ļ¬©ĒśĢņØś ņןĻĖ░ ņäżļ¬ģļĀź(R2 =56.96%)ņØĆ ņŚ¼ņĀäĒ׳ ļåÆņØĆ Ļ▓āņØä ĒÖĢņØĖĒĢĀ ņłś ņ׳ļŗż. ĻĘĖļ¤¼ļ»ĆļĪ£ Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņןļ│ĆņłśņÖĆ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ļź╝ ĒĢ©Ļ╗ś ĒżĒĢ©ĒĢśļŖö ņśłņĖĪņØś Ļ▓ĮņÜ░ ļŗ©ĻĖ░ņŚÉņä£ļŖö Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII), ņןĻĖ░ņŚÉņä£ļŖö Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśĻ░Ć ņżæņÜöĒĢ£ Ļ▓āņØä ņĢī ņłś ņ׳ļŗż.

4factor+SII Ē¢ēņŚÉņä£ļŖö ĻĖ░ņŚģ ĒŖ╣ņä▒ ļ░Å ņŗ£ņן ņÜöņØĖļōżņØä ĒåĄņĀ£ĒĢ£ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ņśłņĖĪĒÜīĻĘĆļČäņäØ Ļ▓░Ļ│╝ļź╝ ņĀ£ņŗ£ĒĢśĻ│Ā ņ׳ļŗż. 1Ļ░£ņøö, 3Ļ░£ņøö, 6Ļ░£ņøö ╬▓SII ņØś Ļ░ÆņØä ņé┤ĒÄ┤ļ│┤ļ®┤ Ļ░üĻ░ü -1.89, -2.06, -2.24ļĪ£, ĻĖ░ņŚģĒŖ╣ņä▒ ļ░Å ņŗ£ņן ņÜöņØĖļōżņØä ĒåĄņĀ£ĒĢ£ ĒøäņŚÉļÅä Ļ│Ąļ¦żļÅä ņ¦ĆņłśļŖö ņŗ£ņן ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņŚÉ ļīĆĒĢ£ ņ£ĀņØśĒĢ£ ņśłņĖĪļĀźņØä Ļ░¢ļŖöļŗż. PC+SIIņØś Ļ▓░Ļ│╝ņÖĆ ņ£Āņé¼ĒĢśĻ▓ī ļŗ©ĻĖ░ņŚÉņä£ ņןĻĖ░ļĪ£ Ļ░łņłśļĪØ ╬▓SII ņØś ņĀłļīĆĻ░ÆņØ┤ Ļ░ÉņåīĒĢśļ®░, Ļ│Ąļ¦żļÅä Ļ▒░ļלļ¤ē ļ│ĆĒÖöņŚÉ ļö░ļźĖ ļ»Ėļל ņŗ£ņן ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņØś ļ░śņØæņä▒ņØ┤ Ļ░ÉņåīĒĢ£ļŗż.

4.3 ņÖĖĒæ£ļ│Ė ņśłņĖĪĒÜīĻĘĆļČäņäØ Ļ▓░Ļ│╝

<Ēæ£ 5>ļŖö Ļ░ü ņśłņĖĪ ļ│ĆņłśļōżņØś ņśłņĖĪ ĻĖ░Ļ░äņŚÉ ļö░ļźĖ ņÖĖĒæ£ļ│Ė ņśłņĖĪĒÜīĻĘĆļČäņäØ Ļ▓░Ļ│╝ļź╝ ļéśĒāĆļéĖļŗż. Ļ░ü ņŚ┤ņŚÉļŖö 1Ļ░£ņøö(h = 1), 3Ļ░£ņøö(h = 3), 6Ļ░£ņøö(h = 6), 9Ļ░£ņøö(h = 9), 12Ļ░£ņøö(h = 12), 15Ļ░£ņøö(h =15), 18Ļ░£ņøö(h =18) ņśłņĖĪ ĒÜīĻĘĆļČäņäØņØś R O S 2 R O S 2 R O S 2 R O S 2 R O S 2 R O S 2

4.4 ņ×Éņé░ļ░░ļČä ņä▒Ļ│╝ļČäņäØ

ļ│Ė ņןņŚÉņä£ļŖö Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś Ļ▓ĮņĀ£ņĀü Ļ░Ćņ╣śļź╝ ĒÅēĻ░ĆĒĢśĻĖ░ ņ£äĒĢ┤ ņ×Éņé░ļ░░ļČä ņĖĪļ®┤ņŚÉņä£ Ļ│Ąļ¦żļÅäņ¦Ćņłś(SII)ņØś ņśłņĖĪļĀźņØä ļČäņäØĒĢśņśĆļŗż. <Ēæ£ 6>ņØĆ ņśłņĖĪļ│ĆņłśļōżņØś ņśłņĖĪ ĻĖ░Ļ░äņŚÉ ļö░ļźĖ ņÖĖĒæ£ļ│Ė ĒÖĢņŗżņä▒ ļō▒Ļ░Ć ņłśņØĄļźĀ ņØ┤ņØĄņØä ļéśĒāĆļéĖļŗż. ĒÖĢņŗżņä▒ ļō▒Ļ░Ć ņłśņØĄļźĀ ņØ┤ņØĄņØĆ ĻĖ░ņżĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż(Ļ│╝Ļ▒░ĒÅēĻĘĀļ¬©ĒśĢ) ļīĆņŗĀņŚÉ ņśłņĖĪĒÜīĻĘĆļ¬©ĒśĢņØä ņé¼ņÜ®ĒĢśĻĖ░ ņ£äĒĢ┤ Ēł¼ņ×Éņ×ÉļōżņØ┤ ĻĖ░Ļ║╝ņØ┤ ņ¦ĆļČłĒĢĀ ņČöĻ░Ć ļ╣äņÜ®ņØä ņØśļ»ĖĒĢśļ®░, Ļ░ÆņØ┤ Ēü┤ņłśļĪØ ņśłņĖĪ ņä▒Ļ│╝Ļ░Ć ņóŗņØīņØä ņØśļ»ĖĒĢ£ļŗż. 1Ļ░£ņøö Ēł¼ņ×É ĻĖ░ņżĆņ£╝ļĪ£ SIIņØś ĒÖĢņŗżņä▒ ļō▒Ļ░Ć ņłśņØĄņØ┤ ņäĖ ļ▓łņ¦ĖļĪ£ ņóŗņØĆ ņä▒Ļ│╝ļź╝ ļ│┤ņśĆĻ│Ā(0.59), 3Ļ░£ņøö Ēł¼ņ×É ĻĖ░ņżĆņ£╝ļĪ£ļŖö SIIņØś ņä▒Ļ│╝Ļ░Ć Ļ░Ćņן ņóŗņĢśļŗż(0.21). ļ░śļ®┤ ņżæņןĻĖ░ Ēł¼ņ×É(h = 9, h = 12)ņØś Ļ▓ĮņÜ░ ņāüļīĆņĀüņ£╝ļĪ£ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII) ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĒÖĢņŗżņä▒ ļō▒Ļ░Ć ņłśņØĄņØ┤ ļé«ņØĆ Ļ▓āņØä ĒÖĢņØĖĒĢĀ ņłś ņ׳ļŗż.

<Ēæ£ 7>ņØĆ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņÖĆ ĻĖ░ņĪ┤ Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśņØś ņĀĢļ│┤ļź╝ ĒÖ£ņÜ®ĒĢśņŚ¼ ņ×Éņé░ ļ░░ļČäĒĢ£ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņāżĒöä ļ╣äņ£©ņØä ļéśĒāĆļéĖļŗż. DeMiguel et al.(2007)ņŚÉ ņØśĒĢśļ®┤ ĒÅēĻĘĀ-ļČäņé░ ļ¬©ĒśĢņØś Ļ▓ĮņÜ░ ļŗ©ĻĖ░ņŚÉņä£ ņ×ģļĀź ļ│ĆņłśņØĖ ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņØś ņČöņĀĢ ņśżņ░©Ļ░Ć ņāüļīĆņĀüņ£╝ļĪ£ Ēü¼Ļ│Ā ņןĻĖ░ņŚÉņä£ļŖö ĻĘĖ ņČöņĀĢ ņśżņ░©Ļ░Ć ņżäņ¢┤ļōĀļŗż. ļö░ļØ╝ņä£ ņØ╝ļ░śņĀüņ£╝ļĪ£ ļŗ©ĻĖ░(h = 1, h = 3)ņŚÉņä£ļŖö ņāüļīĆņĀüņ£╝ļĪ£ ņāżĒöäļ╣äņ£©ņØ┤ ļé«Ļ│Ā, ņןĻĖ░ļĪ£ Ļ░łņłśļĪØ ļåÆņĢäņ¦äļŗż. ņśłļź╝ ļōżņ¢┤ DP, DY, INFLņØś Ļ▓ĮņÜ░ ļŗ©ĻĖ░(h = 1, h = 3) ņ×Éņé░ļ░░ļČäņŚÉņä£ ņØīņØś ņāżĒöä ļ╣äņ£©ņØä Ļ░Ćņ¦Ćļéś ņןĻĖ░(h = 6, h = 9, h = 12) ņ×Éņé░ļ░░ļČäņØś Ļ▓ĮņÜ░ ņ¢æņØś ņāżĒöä ļ╣äņ£©ņØä Ļ░Ćņ¦äļŗż. ļ░śļ®┤, Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ļź╝ ĒÖ£ņÜ®ĒĢ£ ņ×Éņé░ļ░░ļČäļ¬©ĒśĢņØĆ ļŗ©ĻĖ░ņŚÉņä£ ņ×Éņé░ļ░░ļČäņØś ņä▒Ļ│╝Ļ░Ć ļø░ņ¢┤ļéśļéś, ņןĻĖ░ņŚÉņä£ ņ×Éņé░ļ░░ļČäņØś ņä▒Ļ│╝Ļ░Ć ļ¢©ņ¢┤ņ¦äļŗż. ņØ┤ ņŚŁņŗ£, ņŗ£ņן ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņŚÉ ļīĆĒĢ£ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ļŗ©ĻĖ░ ņśłņĖĪļĀźņØ┤ ņāüļīĆņĀüņ£╝ļĪ£ ļø░ņ¢┤ļéśĻĖ░ ļĢīļ¼ĖņØ┤ļŗż.

4.5 ņŻ╝Ļ░Ć ņłśņØĄļźĀ ļČäĒĢ┤ ļČäņäØ Ļ▓░Ļ│╝

ļ│Ė ņןņŚÉņä£ļŖö ļ»Ėļל ņŻ╝Ļ░Ć ņłśņØĄļźĀņØä 3Ļ░Ćņ¦Ć ņÜöņåīļĪ£ ļČäĒĢ┤ĒĢśņŚ¼ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ņśłņĖĪļĀźņŚÉ Ļ┤ĆĒĢ£ ĒĢĄņŗ¼ļÅÖņØĖ(ÕŗĢÕøĀ)ņØä ļČäņäØĒĢśĻ│Āņ×É ĒĢ£ļŗż. ļ©╝ņĀĆ ņŻ╝Ļ░Ć ņłśņØĄļźĀņØĆ ņŗØ (19)ņÖĆ Ļ░ÖņØ┤ ĻĖ░ļīĆņłśņØĄļźĀ, ĒĢĀņØĖņ£©(Discount rate) ĻĘĖļ”¼Ļ│Ā ĒśäĻĖłĒØÉļ”ä ļē┤ņŖż(Cash flow news)ļĪ£ ļČäĒĢ┤ĒĢĀ ņłś ņ׳ņØīņØ┤ ņĢīļĀżņĀĖ ņ׳ļŗż.

Campbell(1991)Ļ│╝ Campbell and Ammer(1993)ņØś ļ░®ļ▓ĢļĪĀņØä ĒÖ£ņÜ®ĒĢśļ®┤ VAR ļČäņäØņØä ĒåĄĒĢ┤ ņśłņāüņ╣ś ļ¬╗ĒĢ£ ņŻ╝Ļ░ĆņłśņØĄļźĀ ņČ®Ļ▓®(Žå t + 1 r = r t + 1 - E t r t + 1 Žå t + 1 C F Žå t + 1 D R

ņØ┤ ļĢī, ņŗØ (3)ņŚÉņä£ņØś Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ĒÜīĻĘĆ Ļ│äņłśļź╝ ņŗØ (23)Ļ│╝ Ļ░ÖņØ┤ ĻĖ░ļīĆņłśņØĄļźĀ(╬▓E), ĒśäĻĖłĒØÉļ”ä ņĀĢļ│┤(╬▓CF), ĒĢĀņØĖņ£© ņĀĢļ│┤(╬▓DR)ļĪ£ ļČäĒĢ┤ĒĢĀ ņłś ņ׳ļŗż.

<Ēæ£ 8>ņØĆ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ĻĖ░ļīĆņłśņØĄļźĀ, ĒśäĻĖłĒØÉļ”ä ļē┤ņŖż, ĒĢĀņØĖņ£© ļē┤ņŖżņŚÉ ļīĆĒĢ£ Ļ│Ąļ¦żļÅäņ¦Ćņłś(SII)ņØś ņśłņĖĪļĀźņØä ņØśļ»ĖĒĢ£ļŗż. Ēæ£ņØś ╬▓kļŖö ļŗżņØī ņśłņĖĪĒÜīĻĘĆļ¬©ĒśĢņØś OLS ņČöņĀĢņ╣śļź╝ ņØśļ»ĖĒĢ£ļŗż.

ņŚ¼ĻĖ░ņä£, yt+1ļŖö ņøöļ│ä KOSPI ļĪ£ĻĘĖ ņłśņØĄļźĀņŚÉņä£ļČĆĒä░ ņČöņĀĢļÉ£ E t r t + 1 ^ Žå t + 1 C F ^ Žå t + 1 D R ^

ņĀłļīĆĻ░ÆņØä ĻĖ░ņżĆņ£╝ļĪ£ ļ¬©ļōĀ ņśłņĖĪĒÜīĻĘĆļČäņäØņŚÉņä£ ╬▓CF ņČöņĀĢņ╣śĻ░Ć Ļ░Ćņן Ēü¼ļ®░, DEļź╝ ņČöĻ░Ć ĒåĄņĀ£ ļ│ĆņłśļĪ£ ņé¼ņÜ®ĒĢ£ Ļ▓ĮņÜ░ļź╝ ņĀ£ņÖĖĒĢśĻ│Ā ĒĢŁņāü ņ£ĀņØśĒĢśļŗż. ņØ┤ļŖö ņŗ£ņןņĀäļ░śņØś Ļ│Ąļ¦żļÅä Ļ▒░ļלņÖĆ ļ»Ėļל ĒśäĻĖłĒØÉļ”äļē┤ņŖżĻ░Ć ņØīņØś ņāüĻ┤ĆĻ┤ĆĻ│äļź╝ Ļ░Ćņ¦Ćļ®░, ĻĘĖ ņśüĒ¢źļĀźļÅä Ļ░Ćņן Ēü¼ļŗżļŖö Ļ▓āņØä ņØśļ»ĖĒĢ£ļŗż. Ļ▓░ļĪĀņĀüņ£╝ļĪ£ Ļ│Ąļ¦żļÅäĻ▒░ļלņ×ÉļŖö ļ»Ėļל ĒśäĻĖłĒØÉļ”ä ļē┤ņŖżņŚÉ ļīĆĒĢ£ ņĀĢļ│┤ļź╝ Ļ░Ćņ¦ä ņĀĢļ│┤Ļ▒░ļלņ×ÉņØ┤ļ®░ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ņŻ╝Ļ░Ćņ¦Ćņłś ņśłņĖĪļĀźņØ┤ ļ»Ėļל ĒśäĻĖłĒØÉļ”ä ļē┤ņŖż ņĀĢļ│┤ņŚÉ ĻĖ░ņØĖĒĢ£ Ļ▓āņ×äņØä ņŗ£ņé¼ĒĢ£ļŗż.

5. Ļ▓░ļĪĀ ļ░Å ņŗ£ņé¼ņĀÉ

ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö ĒĢ£ĻĄŁņŗ£ņןņŚÉ ņĪ┤ņ×¼ĒĢśļŖö ņŻ╝ņŗØ, ETFs, ļ”¼ņĖĀņØś Ļ│Ąļ¦żļÅä ņĀĢļ│┤ļź╝ ĒÖ£ņÜ®ĒĢśņŚ¼ ņŗ£ņן ņĀäļ░śņØś Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ļź╝ ĻĄ¼ņČĢĒĢśņśĆļŗż. ĻĖ░ņĪ┤ Ļ│Ąļ¦żļÅäņÖĆ ņŻ╝Ļ░ĆņłśņØĄļźĀ Ļ░äņØś Ļ┤ĆĻ│äļź╝ ļČäņäØĒĢ£ ĻĄŁļé┤ ņŚ░ĻĄ¼ņØś Ļ▓ĮņÜ░ ļīĆļČĆļČä Ļ░£ļ│ä ĻĖ░ņŚģņØä ņżæņŗ¼ņ£╝ļĪ£ ļČäņäØĒĢ£ ļ░śļ®┤, ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö ņŗ£ņן ņĀäļ░śņØś Ļ│Ąļ¦żļÅä ņĀĢļ│┤ņÖĆ ĒĢ£ĻĄŁ ĻĖłņ£Ą ņŗ£ņןņØś ņĀäļ░śņØś ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäĻ░äņØś Ļ┤ĆĻ│äļź╝ ļČäņäØĒĢśņśĆļŗż. Ļ│Ąļ¦żļÅä ņ¦ĆņłśņØś ņŗ£ņןņśłņĖĪļĀźņØä ĒÖĢņØĖĒĢśĻĖ░ ņ£äĒĢ┤ ĻĘĖļĀłņØĖņĀĖ ņØĖĻ│╝Ļ┤ĆĻ│ä ļČäņäØ, ņśłņĖĪĒÜīĻĘĆļČäņäØ, ņ×Éņé░ļ░░ļČä ļČäņäØ ļō▒ ļŗżļ░®ļ®┤ņØś ļČäņäØņØä ņŗ£Ē¢ēĒ¢łņ£╝ļ®░, Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ļŗ©ĻĖ░ ņśłņĖĪļĀźņØ┤ ĒåĄĻ│äņĀü, Ļ▓ĮņĀ£ņĀüņ£╝ļĪ£ ļ¬©ļæÉ ņ£ĀņØśĒĢ£ Ļ▓āņØä ĒÖĢņØĖĒĢśņśĆļŗż. ņÖĖĒæ£ļ│Ė ņśłņĖĪĒÜīĻĘĆļČäņäØĻ│╝ ņ×Éņé░ļ░░ļČä ļČäņäØĻ▓░Ļ│╝, ņŗ£ņן ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņŚÉ ļīĆĒĢ£ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ņśłņĖĪļĀźņØĆ ļŗ©ĻĖ░ņŚÉņä£ ļø░ņ¢┤ļéśĻ│Ā ņןĻĖ░ņŚÉņä£ ņĢĮĒÖöļÉśļŖö Ļ▓āņØä ĒÖĢņØĖĒĢśņśĆļŗż. ņØ╝ļ░śņĀüņ£╝ļĪ£ Ļ▒░ņŗ£Ļ▓ĮņĀ£ ļ░Å ņŗ£ņן ļ│ĆņłśļōżņØś ļŗ©ĻĖ░ ņśłņĖĪļĀźņØ┤ ļé«ņØĆ Ļ▓āņØä Ļ│ĀļĀżĒĢśļ®┤ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ļåÆņØĆ ļŗ©ĻĖ░ ņŗ£ņן ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚä ņśłņĖĪņØĆ Ļ▓ĮņĀ£ņĀüņØĖ Ļ░Ćņ╣śļź╝ Ļ░¢ļŖöļŗż. ņŗ£ņן ņłśņØĄļźĀ ļČäĒĢ┤ļź╝ ĒåĄĒĢ£ ņśłņĖĪĒÜīĻĘĆļČäņäØ Ļ▓░Ļ│╝, Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉļŖö ļ»Ėļל ņŗ£ņןņĀäļ░śņŚÉ Ļ┤ĆĒĢ£ ĒśäĻĖłĒØÉļ”ä ļē┤ņŖżļź╝ ņĘ©ļōØĒĢśļŖöļŹ░ ņØ┤ņĀÉņØ┤ ņ׳ņŚłļŗż. ļśÉĒĢ£, ĻĖ░ņĪ┤ Ļ│Ąļ¦żļÅä Ļ┤ĆļĀ© ņŚ░ĻĄ¼Ļ▓░Ļ│╝ņŚÉ ļö░ļź┤ļ®┤, Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉļŖö ļ»Ėļל Ļ░£ļ│ä ĻĖ░ņŚģņŚÉ Ļ┤ĆĒĢ£ ņĀĢļ│┤ļź╝ ņĘ©ļōØĒĢśļŖö ļŖźļĀźņØ┤ ņ׳ļŗż. ļæÉ Ļ▓░Ļ│╝ļź╝ ņóģĒĢ®ĒĢśļ®┤, Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉļŖö ņ×Éņé░Ļ░ĆĻ▓®ņŚÉ ļīĆĒĢ£ Ļ░£ļ│ä Ļ│Āņ£Ā(Idiosyncratic)ņØś ņÜöņåīļ┐Éļ¦ī ņĢäļŗłļØ╝, ņ▓┤Ļ│äņĀü(Systemic) ņÜöņåīļź╝ ĒÅēĻ░ĆĒĢśļŖö ņĀĢļ│┤Ļ▒░ļלņ×Éņ×äņØä ņŗ£ņé¼ĒĢ£ļŗż.

ļŗ©ĻĖ░ņŚÉņä£ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ņśłņĖĪļĀźņØś ĻĘ╝ņøÉņØĆ ņĀĢļ│┤ ĒÜŹļōØ ļ░Å ļ”¼ņŖżĒü¼ Ļ░Éļé┤ņŚÉ ļīĆĒĢ£ ļ│┤ņāü, ĻĘĖļ”¼Ļ│Ā ņ░©ņØĄĻ▒░ļל ņĀ£ņĢĮ(Limit to arbitrage)ņØś Ļ┤ĆņĀÉņ£╝ļĪ£ ņĀæĻĘ╝ĒĢĀ ņłś ņ׳ļŗż. ņ▓½ņ¦Ė, ņĀĢļ│┤ņØś Ļ┤ĆņĀÉņŚÉņä£ ņŗ£ņן ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņŚÉ ļīĆĒĢ£ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ņśłņĖĪļĀźņØĆ Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉĻ░Ć ļ»Ėļל ņŗ£ņןņĀäļ░śņØś ņĀĢļ│┤ļź╝ ĒÜŹļōØĒĢśĻ│Ā ļČäņäØĒĢśļŖö Ē¢ēņ£äņŚÉ ļīĆĒĢ£ ļ│┤ņāüņ£╝ļĪ£ ĒĢ┤ņäØĒĢĀ ņłś ņ׳ļŗż. Grossman and Stiglitz(1980)ņØś ņŚ░ĻĄ¼Ļ▓░Ļ│╝ņŚÉ ļö░ļź┤ļ®┤, Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉļŖö ļ»Ėļל ņŗ£ņן ņĀĢļ│┤ļź╝ ņ¢╗Ļ│Ā, ņØ┤ļź╝ ĒĢ┤ņäØĒĢśļŖöļŹ░ ļ│┤ņāüņØä ļ░øļŖöļŗż. ĻĘĖļ¤¼ļéś, Ļ▒░ļלņåīņŚÉņä£ Ļ│Ąļ¦żļÅä Ļ▒░ļלĻ░Ć Ļ│ĄņŗØņĀüņ£╝ļĪ£ ļ░£Ēæ£ļÉśļŖö Ļ▓ĮņÜ░ņŚÉļÅä Ēł¼ņ×Éņ×ÉļōżņØĆ ņŗ£ņן ņĀäļ░śņØś Ļ│Ąļ¦żļÅä Ļ▒░ļלņĀĢļ│┤ļź╝ ņĀüĻĘ╣ņĀüņ£╝ļĪ£ ĒÖ£ņÜ®ĒĢśņ¦Ć ņĢŖļŖöļŹ░, ĻĘĖ ņØ┤ņ£ĀļŖö ņĄ£ĻĘ╝Ļ╣īņ¦Ć Ļ│Ąļ¦żļÅä Ļ▒░ļל ņ×ÉļŻīĻ░Ć ņĀäņ×É Ļ│Ąņŗ£ ļÉśņ¦Ć ņĢŖņĢśĻĖ░ ļĢīļ¼ĖņØ┤ļŗż. ĒŖ╣Ē׳, ĒĢ£ĻĄŁ ņŗ£ņןņØś Ļ▓ĮņÜ░, Ļ░£ļ│äĻĖ░ņŚģņŚÉ ļīĆĒĢ£ Ļ│Ąļ¦żļÅä ņ×ÉļŻīļŖö 2008ļģä ņØ┤Ēøä Ļ│Ąņŗ£ļÉśņŚłĻĖ░ ļĢīļ¼ĖņŚÉ ņĀäņ▓┤ ĻĖ░ņŚģņŚÉ ļīĆĒĢ£ Ļ│Ąļ¦żļÅä ņ×ÉļŻīļź╝ ļ¬©ņ£╝ĻĖ░ ņ£äĒĢ┤ņä£ļŖö ņāüļŗ╣ĒĢ£ ļ╣äņÜ®ņØ┤ ņåīļ¬©ļÉ£ļŗż. ļæśņ¦Ė, Ļ│Ąļ¦żļÅäļź╝ ĒåĄĒĢ£ ņ░©ņØĄĻ▒░ļל ĻĖ░ĒÜī(Arbitrage opportunity) ņŗżĒśä ņŗ£ ņŗ£ņן ļ¦łņ░░ ņÜöņØĖņŚÉ ņØśĒĢ£ ņ£äĒŚśņØ┤ ņĪ┤ņ×¼ĒĢśļŖöļŹ░, ņŗ£ņן ļ”¼ņŖżĒü¼ Ēöäļ”¼ļ»ĖņŚäņŚÉ ļīĆĒĢ£ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ņØś ņśłņĖĪļĀźņØĆ ņØ┤ņŚÉ ļīĆĒĢ£ ļ│┤ņāüņ£╝ļĪ£ ĒĢ┤ņäØĒĢĀ ņłś ņ׳ļŗż(Shleifer and Vishny, 1997). Engelberg et al.(2018)ņŚÉ ļö░ļź┤ļ®┤, Ļ│Ąļ¦żļÅä Ļ▒░ļלņ×ÉļŖö ņ”ØĻČīļīĆņ░©ņŗ£ņןņŚÉņä£ ņŻ╝ņŗØņØä ļ╣īļ”┤ ļĢī, ļŗżņ¢æĒĢ£ Ļ│Ąļ¦żļÅä Ļ│Āņ£ĀņØś ņ£äĒŚśņŚÉ ņ¦üļ®┤ĒĢ£ļŗż. ņśłļź╝ ļōżļ®┤, ļīĆņ░©ņŗ£ņןņŚÉņä£ ņŻ╝ņŗØ ļīĆņČ£ņØ┤ ņĘ©ņåīļÉśĻ▒░ļéś, ņŗ£ņןņØ┤ļéś Ļ░£ļ│ä ĻĖ░ņŚģņØś ņāüĒÖ®ņŚÉ ļö░ļØ╝ ļīĆņČ£ ļ╣äņÜ®ņØ┤ Ēü¼Ļ▓ī ļ│ĆļÅÖĒĢĀ ņ£äĒŚśņØ┤ ņ׳ļŗż. ņØ┤ļĪ£ ņØĖĒĢśņŚ¼, ņŗ£ņןņŚÉņä£ ņ░©ņØĄĻ▒░ļלņØś ĻĖ░ĒÜīĻ░Ć ņĪ┤ņ×¼ĒĢśņŚ¼ļÅä, Ēł¼ņ×Éņ×ÉļŖö Ļ│Ąļ¦żļÅä Ļ▒░ļלļź╝ ĒåĄĒĢ┤ ņ░©ņØĄņØä ņ¢╗ļŖöļŹ░ ņ£äĒŚśņØä ņłśļ░śĒĢ£ļŗż. Ļ│Ąļ¦żļÅäņ¦Ćņłś(SII)ņØś ņśłņĖĪļĀźņØĆ ņØ┤ļ¤¼ĒĢ£ ļ”¼ņŖżĒü¼ņŚÉ ļīĆĒĢ£ ļ│┤ņāüņ£╝ļĪ£ ĒĢ┤ņäØĒĢĀ ņłś ņ׳ļŗż. ļśÉĒĢ£, ņŗ£ņןņŚÉ Ļ│Ąļ¦żļÅä ņĀ£ņĢĮņØ┤ ņĪ┤ņ×¼ĒĢśļŖö Ļ▓ĮņÜ░, Ēł¼ņ×Éņ×ÉļŖö Ļ│Ąļ¦żļÅä Ļ▒░ļלļĪ£ ņØĖĒĢ£ ņØ┤ņØĄņØ┤ ļ╣äņÜ® ņØ┤ņāüņØ╝ ļĢīļ¦ī Ļ│Ąļ¦żļÅä Ļ▒░ļלļź╝ ņŗżņŗ£ĒĢ£ļŗż. ļö░ļØ╝ņä£ ņ░©ņØĄĻ▒░ļלņØś ņĀ£ņĢĮņØ┤ ņĪ┤ņ×¼ĒĢ£ļŗżļ®┤, ņĀĢļ│┤Ļ▒░ļלņ×ÉļōżņØś ņŗ£ņןņ░ĖņŚ¼Ļ░Ć ņĀ£ĒĢ£ļÉśņ¢┤ ņŗ£ņןņŚÉ ņĀĢļ│┤Ļ░Ć ņÖäļ▓ĮĒ׳ ļ░śņśüļÉśņ¦Ć ņĢŖņØä ņłś ņ׳ļŗż. ņŗżņĀ£ ĒĢ£ĻĄŁ ņŗ£ņןņŚÉņä£ļŖö Ļ│Ąļ¦żļÅä Ļ▒░ļלĻ░Ć ĒÖ£ļ░£ĒĢśņ¦Ć ņĢŖņ£╝ļ®░, Ļ│Ąļ¦żļÅä Ļ▒░ļלĻ░Ć Ļ░Ćņן ļ¦ÄņĢśļŹś 2008ļģä 7ņøöņŚÉļÅä ņŗ£ņן ņĀäņ▓┤ņØś ļ░£Ē¢ēņŻ╝ņŗØņłś ļīĆļ╣ä Ļ│Ąļ¦żļÅä Ļ▒░ļלņØś ļ╣äņ£©ņØĆ 0.16%ļĪ£ ļé«ņØĆ ņłśņżĆņØ┤ņŚłļŗż. Lamont and Stein(2004)ļŖö IT ļ▓äļĖö ĻĖ░Ļ░äļÅÖņĢł(1998ļģä~2000ļģä)ņŚÉ ļ»ĖĻĄŁ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ļ░£ņāØĒĢ£ Ļ│Ąļ¦żļÅä Ļ▒░ļלĻ░Ć ņŗ£ņןņĀäļ░śņØś Ļ░ĆĻ▓® Ļ┤┤ļ”¼ļź╝ ņĀĢņāüĻ░ĆĻ▓®ņ£╝ļĪ£ ļÉśļÅīļ”¼ļŖöļŹ░ ļČĆņĪ▒ĒĢ©ņØä ņ¦ĆņĀüĒĢśņśĆļŗż. Ļ░ÖņØĆ ļ¦źļØĮņŚÉņä£ ĒĢ£ĻĄŁ ņŗ£ņןņØś ņĀäļ░śņĀüņØĖ Ļ│Ąļ¦żļÅä Ļ▒░ļלļ¤ēņØĆ ņŗ£ņןņŚÉņä£ ļ░£ņāØĒĢśļŖö Ļ░ĆĻ▓® Ļ┤┤ļ”¼ļź╝ ņ¦äņĀĢĒĢ£ Ļ░ĆĻ▓®ņ£╝ļĪ£ ļÉśļÅīļ”¼ļŖöļŹ░ ļČĆņĪ▒ĒĢśļŗżĻ│Ā ļ│╝ ņłś ņ׳ļŗż. ĒĢ┤ņåīļÉśņ¦Ć ļ¬╗ĒĢ£ Ļ░ĆĻ▓® Ļ┤┤ļ”¼ļŖö Ļ▓░ĻĄŁ ļ»ĖļלņŚÉ ņŗżĒśäļÉśĻĖ░ ļĢīļ¼ĖņŚÉ, ņŗ£ņן ņĀäļ░śņØś Ļ│Ąļ¦żļÅä ņĀĢļ│┤ņØĖ Ļ│Ąļ¦żļÅä ņ¦Ćņłś(SII)ļŖö ļ»Ėļל ņŗ£ņן ņłśņØĄļźĀņŚÉ ļīĆĒĢ£ ņśłņĖĪļĀźņØä Ļ░Ćņ¦ĆĻ▓ī ļÉ£ļŗż.

ļ│Ė ņŚ░ĻĄ¼Ļ░Ć ņŗ£ņé¼ĒĢśļŖö ļ░öļŖö ļŗżņØīĻ│╝ Ļ░Öļŗż. ļ©╝ņĀĆ, ņŗ£ņןņŚÉņä£ Ļ░ĆĻ▓® Ļ┤┤ļ”¼Ļ░Ć ĒĢ┤ņåīļÉśļŖö ņåŹļÅäļŖö ļ»ĖĻĄŁ ņŗ£ņןņŚÉ ļ╣äĒĢ┤ ĒĢ£ĻĄŁ ņŗ£ņןņØ┤ ļ│┤ļŗż ļ╣Āļź┤ļŗż. Rapach et al.(2016)ņØś ņŚ░ĻĄ¼Ļ▓░Ļ│╝ņŚÉ ļö░ļź┤ļ®┤, ļ»ĖĻĄŁņŚÉņä£ļŖö Ļ│Ąļ¦żļÅä ņ¦ĆņłśņØś ņśłņĖĪļĀźņØ┤ ņŗ£Ļ░äņØ┤ ņ¦ĆļéśļÅä ņ¦ĆņåŹļÉśļŖö ļ░śļ®┤, ĒĢ£ĻĄŁ ņŗ£ņןņØś Ļ▓ĮņÜ░ ļŗ©ĻĖ░ ņśłņĖĪļĀźņØĆ ļø░ņ¢┤ļéśļéś ņןĻĖ░ņŚÉņä£ņØś ņśłņĖĪļĀźņØĆ ņé¼ļØ╝ņ¦äļŗż. ņØ┤ļŖö ĒĢ£ĻĄŁ ņŗ£ņןņØś Ēł¼ņ×Éņ×ÉļōżņØ┤ Ļ│Ąļ¦żļÅä Ļ▒░ļלņŚÉ ĻĖ░ļ»╝ĒĢśĻ▓ī ļ░śņØæĒĢ£ Ļ▓░Ļ│╝ ņŗ£ņןņŚÉņä£ņØś Ļ░ĆĻ▓® Ļ┤┤ļ”¼Ļ░Ć ļ╣Āļź┤Ļ▓ī ĒĢ┤ņåīļÉśņ¢┤ ņןĻĖ░ ņśłņĖĪļĀźņØä ņ×āļŖö Ļ▓āņ£╝ļĪ£ ĒĢ┤ņäØĒĢĀ ņłś ņ׳ļŗż. ļéśņĢäĻ░Ć ĻĖłņ£Ąļŗ╣ĻĄŁņØś Ļ│Ąļ¦żļÅä ņĀ£ņĢĮ ņÖäĒÖö ņĀĢņ▒ģņØä ņĀ£ņĢłĒĢĀ ņłś ņ׳ļŗż. Ļ│Ąļ¦żļÅä ņĀ£ņĢĮņØĆ ņĀĢļ│┤Ļ▒░ļלņ×ÉņØś ņŗ£ņן ņ░ĖņŚ¼ļź╝ ļ¦ēņĢä, ņŗ£ņןņØś ņĀĢļ│┤ĒÜ©ņ£©ņä▒ņØä ņĀĆĒĢ┤ĒĢĀ Ļ░ĆļŖźņä▒ņØ┤ ņ׳ļŗż. ļ░śļ®┤, ņĀüņĀłĒĢ£ Ļ│Ąļ¦żļÅä ņĀ£ņĢĮ ņÖäĒÖöļŖö ņĀĢļ│┤Ļ▒░ļלņ×ÉņØś ņĀĢļ│┤ļź╝ ņŗ£ņןņŚÉ ļ░śņśüĒĢśņŚ¼, Ļ░ĆĻ▓® Ļ┤┤ļ”¼ ĒĢ┤ņåīļź╝ ļÅäņÜĖ ņłś ņ׳ļŗż.