1. Introduction

The ultimate purpose of shareholder activism is to maximize shareholder wealth. How investors interpret activism and whether activism eventually increases shareholder wealth are pivotal questions to ask in shareholder activism research. Investors can maximize their profits either by following Wall Street rules or by engaging in activism. Institutional investors, including pension funds, choose to pursue activism because following Wall Street Rules has the potential to incur losses. Pension funds own substantial shares of their portfolio firms, and thus when they sell shares of a portfolio firm, stock prices decrease, and further losses are unavoidable. Hence, instead of following Wall Street rules, pension funds engage in activism to increase shareholder wealth.

Although extant empirical research examined whether activism increases shareholder wealth, the results are inconsistent. Low cost institutional activism ŌĆöshareholder proposals or announcing to vote against agendasŌĆö shows mixed results regarding its impact on the stock market (Kim et al., 2009). Shareholder proposals sponsored by institutional investors have either insignificant or weakly negative effects on stock prices (e.g. Del Guercio and Hawkins, 1999; Gillan and Starks, 2000; Smith, 1996; Thomas and Cotter, 2007). Announcing to vote against agendas in annual shareholder meetings either does not significantly affect the stock market reactions (Kim et al., 2014) or has a positive impact on stock prices (Kim and Yon, 2014). Only studies concerning proxy fights, the costliest activism strategy, show consistent results that proxy fights have a significantly positive impact on stock returns of target firms (e.g. Mulherin and Poulsen, 1998; Ikenberry and Lakonishok, 1993; Dodd and Warner, 1983; DeAngelo and DeAngelo, 1989).

Thus, we revisit the effect of institutional activism on the stock market. We zero in on a pension fundŌĆÖs announcements to vote against agendas of annual shareholder meetings. In many cases, voting yes is an empty ritual (Grundfest, 1992) and is not likely to have a meaningful impact on the stock market. On the other hand, a veto announcement receives investorsŌĆÖ attention because it is a public expression of shareholder discontent and is an action that publicly identifies poor managers (Grundfest, 1992). A ŌĆ£vote noŌĆØ announcement is a type of low-cost shareholder activism that can bring changes in governance (Ferri, 2013), shareholder wealth (Kim and Yon, 2014; Lim and Lee, 2019), performance (Del Guercio et al., 2008), and CEO pay (Ertimur et al., 2010).

The central goal of our study is to clarify whether activism increases shareholder wealth. Previous studies are limited in that it is unclear whether the event date is the day that investors first receive information about activism. Some studies used a proxy mailing date as the event date (e.g. Thomas and Cotter, 2007; Smith, 1996; Gillan and Starks, 2000). However, the mailing date might not be the first day that investors hear about the activism (Del Guercio and Hawkins, 1999; Gillan and Starks, 2007) because information on the activism could have leaked to capital markets prior to the mailing day. Other studies used the annual shareholder meeting date as the event date (e.g. Del Guercio and Hawkins, 1999; Smith, 1996; Thomas and Cotter, 2007), which also contains confounding factors. A large number of decisions are made at the annual meetings, and therefore it is difficult to single out the pure effect of shareholder activism on the stock market (Gillan and Starks, 2007).

Recent changes in proxy voting policies of the Korea National Pension Service (NPS) allow us to cleanly measure investorsŌĆÖ reactions to shareholder activism without confounding factors. Utilizing the policy change, we study how the stock market reacts to pension fund activism. The NPS is a Korean public pension fund, and it adopted a stewardship code in 2018. Starting in the 2019 proxy season, the NPS disclosed its proxy voting decisions ahead of the annual shareholder meetings. The NPS announced its voting decisions in the late afternoon or at night, after the stock market had closed. Therefore, the opening price of the subsequent day contains the effect of the NPSŌĆÖs proxy voting announcements without any contaminating factors. By using the subsequent dayŌĆÖs opening price, we are able to conduct a clean event study.

In addition to examining stock market reactions, this paper also explores a crucial but understudied market constituent - the media. Prior research found that target firmsŌĆÖ characteristics or the way firms deal with activism impacts shareholder wealth (Mulherin and Poulsen, 1998; Smith, 1996). We suggest that in addition to target firm characteristics, the media also affects shareholder wealth. The media influences the stock market by drawing shareholdersŌĆÖ attention to certain issues and by forming public opinion. Because low cost institutional activism aims at calling attention to governance reforms rather than pushing for instant changes in corporate governance, the role of the media should not be overlooked. Hence, we study how publicity of activism affects the stock market response.

Using a sample of 46 firms for which the NPS pre-disclosed to veto agendas of 2019 annual shareholder meetings, we find that the stock market reacts negatively to the NPSŌĆÖs ŌĆ£vote noŌĆØ announcements. However, the stock market responds positively when the NPSŌĆÖs veto announcement is highly covered in the media.

A major contribution of our study is that it is one of the first studies that cleanly examines stock market reactions to shareholder activism. This paper also underscores the importance of using media reports for pension funds. Lastly, this paper furthers the literature on pension fund activism by providing reasons why the stock market responds negatively to pension fund activism.

1.1 Backgrounds on the NPS

The NPS was established in 1987 to help secure the retirement benefits of Korean citizens (National Pension Service, n.d.). It is now the largest public pension fund in Korea and the worldŌĆÖs third largest public pension fund (National Pension Service Investment Management, n.d.). The NPS manages approximately $568 billion in assets and has a stake of more than five percent in the Korean stock market (Song, 2018).

In 2018, the NPS adopted a stewardship code to improve the corporate governance of Korean companies. The stewardship code is ŌĆ£the principles on the duty of fiduciaries that manage client assetsŌĆØ (Nam, 2017), and stresses the stewardship responsibilities of institutional investors. After the adoption of the stewardship code, the NPS decided to actively exercise its shareholder rights in an effort to carry out the duty of fiduciaries and maximize shareholder wealth. Notably, in the 2019 proxy season, the NPS disclosed its proxy voting decisions in advance of annual shareholdersŌĆÖ meetings. Firms in which the NPS has more than 10 percent stake or more than one percent in domestic equity are the subjects of pre-disclosure. By this criterion, the NPS targeted 96 firms in total. Among the 96 firms, the NPS announced to veto 101 agendas of 48 firms. The authors excluded two firms - Hyundai Motors and Hyundai Mobis - and the final sample consists of 46 firms.

<Table 2> shows that in the 2019 proxy season, the disapproval rate of pre-disclosed agendas is 14 percent, which is notably higher than the disapproval rate of past years. Previous studies that examined the NPSŌĆÖs voting decisions demonstrate that the NPSŌĆÖs disapproval rate is lower than 10 percent in general. Kim and Yon (2014), Lee et al. (2017), Kim et al. (2014), and Kang (2010) each presented the NPSŌĆÖs average disapproval rate, and the disapproval rate was 7.46 percent between 2005 and 2011, 9.38 percent between 2005 and 2014, 5.25 percent between 2006 and 2009, and 6.87 percent in 2010.

<Table┬Ā1>

Variable Descriptions

This table reports the definitions of variables collected for the 46 firms in our final sample.

<Table┬Ā2>

Pre-announced Agenda Types

This table reports the disapproval rate of agendas and firms by agenda types. The same firm can be counted several times because the NPS can veto multiple agendas of the same company.

The NPS plays a leading role in institutional activism in Korea. In Korea, institutional investors have been criticized for serving as a rubber stamp (Kwon, 2017). Institutional investorsŌĆÖ disapproval rate at annual shareholdersŌĆÖ meetings was a mere two percent in 2016 and 2017 (Ahn and Jang, 2019). The NPS disapproval rate is higher than that of other institutional investors and continues to increase, implying that the NPS is an active monitor and is a leader among Korean institutional activists.

2. Literature Review and Hypotheses

2.1 The Effect of Pension Fund Activism on the Stock Market

Though the stock market response to shareholder activism has been examined in many earlier studies, the results are inconclusive. Only proxy contests, the costliest shareholder activism strategy, have a positive influence on shareholder wealth, while less costly strategies yield mixed results. Low cost activism strategies include disapproving agendas of annual shareholder meetings, shareholder proposals, and being included in the California Public EmployeesŌĆÖ Retirement System (CalPERS) focus list.

Voting against agendas of annual shareholder meetings is the weakest form of institutional activism, and several Korean papers examine its influence on the financial market. Kim et al. (2014) analyze the NPSŌĆÖs veto over shareholder meeting agendas and show that the NPSŌĆÖs veto does not significantly impact the stock market. Kim and Yon (2014) examine firms that their annual meetingsŌĆÖ agendas are vetoed by institutional investors between 2005 and 2011 and present that the institutional investorsŌĆÖ veto increases stock prices of target firms. Sohn and Bae (2018) analyze institutional investorsŌĆÖ proxy voting decisions between 2005 and 2014 and find that the institutional investorsŌĆÖ disapproval rate is negatively related to target firmsŌĆÖ credit ratings. Lim and Lee (2019) examine the NPSŌĆÖs pre-disclosure of proxy voting decisions and report that the stock market responds negatively to the NPSŌĆÖs veto announcement.

One U.S based study, Del Guercio et al. (2008), analyzes ŌĆ£just vote noŌĆØ campaigns, which are similar to voting against agendas at the annual shareholder meetings. ŌĆ£Just vote noŌĆØ campaigns are efforts to convince other shareholders ŌĆ£to withhold their vote from one or more directors in an effort to communicate a message of shareholder dissatisfaction to the board.ŌĆØ This study finds that ŌĆ£just vote noŌĆØ campaigns increase shareholder wealth and firm performance.

Shareholder proposals sponsored by pension funds do not have a statistically significant impact on the stock market (Wahal, 1996; Thomas and Cotter, 2007; Del Guercio and Hawkins, 1999). However, they are significant when the target firms are analyzed separately according to their response to the proposals (Smith, 1996). Smith (1996) analyzes 51 firms targeted by CalPERS from 1987 to 1993 and presents both positive and negative stock market reactions. When a target firm settles with CalPERS, shareholder wealth increases, but when a target firm does not settle, shareholder wealth decreases. Studies that analyze shareholder proposals sponsored by pension funds as well as other types of investors such as individuals and religious organizations also show that shareholder proposals do not have a significant effect on the stock market (Gillan and Starks, 2000; Karpoff et al., 1996).

Research on the effect of CalPERSŌĆÖs focus list announcements on the stock market presents mixed results. CalPERS is a U.S. pension fund and is a leader in shareholder activism (Nelson, 2006). From 1992 to 2009, CalPERS released an annual focus list, naming its target firms (Burr, 2010; Nelson, 2006). CalPERS urged firms in the focus list to improve performance, become shareholder oriented, and initiate governance structure reforms (English II et al., 2004). English II et al. (2004) and Barber (2007) examine the effect of being included in the CalPERSŌĆÖs focus list and show that it creates shareholder wealth. In contrast, Nelson (2006) reports that the CalPERSŌĆÖs focus list does not affect the shareholder wealth of target firms.

The costliest strategy, proxy contest, is found to increase shareholder wealth. Dodd and Warner (1983), Mulherin and Poulsen (1998), and DeAngelo and DeAngelo (1989) show that proxy contests increase stock prices of target firms. One exception is the study of Ikenberry and Lakonishok (1993). They examine 97 proxy contests from 1968 to 1987 and present negative abnormal returns.

Our study addresses low cost institutional activism, specifically, the disapproval of agendas of annual shareholdersŌĆÖ meetings. We move one step forward from prior studies in two ways. First, instead of using the proxy mailing date or the annual shareholdersŌĆÖ meeting date as the event day, we use the day subsequent to the NPSŌĆÖs pre-disclosure. It is challenging to eliminate confounding factors when an event date is defined as a mailing date or the annual shareholder meeting date. Investors might hear about the activism prior to the mailing date due to information leakage (Del Guercio and Hawkins, 1999; Thomas and Cotter, 2007). Also, a great number of decisions are made at the annual meetings, and thus it is complex to single out the pure effect of shareholder activism on the stock market. Defining the event day as the day following the NPSŌĆÖs pre-disclosure enables us to remove confounding factors and conduct a clean event study.

Second, we use the market adjusted model instead of the market model when conducting an event study. Lim and Lee (2019) use the market model to examine the effect of the NPSŌĆÖs pre-disclosure on the stock market. However, we use the market adjusted model to alleviate methodological problems that the market model has.

2.2 Hypotheses

2.2.1 The effect of ŌĆ£vote noŌĆØ Announcements on the Stock Market

Based on the signaling theory (Spence, 2002), we view the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-announcement as a signal sent to the stock market. When the stock market receives a signal, it interprets the signal, and its interpretation is reflected in stock price changes. If the stock market views ŌĆ£vote noŌĆØ announcements positively, then the stock price will rise, increasing shareholder wealth. On the contrary, if the stock market views ŌĆ£vote noŌĆØ announcements negatively, then the stock price will decline, decreasing shareholder wealth.

The market interprets the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-announcements positively if it expects that target firms will improve their governance structure or performance. The stock market can expect future improvements for two reasons. First, management is sensitive to reputational damage caused by the NPSŌĆÖs targeting. The NPSŌĆÖs veto disclosure implies that the NPS is dissatisfied with the current managementŌĆÖs decisions (Del Guercio et al., 2008; Grundfest, 1992). Hence, ŌĆ£vote noŌĆØ announcements impair managementŌĆÖs reputation and positive image associated with having membership on the target firmsŌĆÖ board (Grundfest, 1992). Management has elite status owning to their titles (DŌĆÖAveni and Kesner, 1993; Mills, 2000). Managers are sensitive to reputational damage and feel shame on the ŌĆ£vote noŌĆØ announcements because, to them, non-pecuniary rewards such as pride, reputation, and honor are as valuable as pecuniary rewards (Grundfest, 1992). Hence, the target firmŌĆÖs managers will make an effort to rebuild their reputation and avoid being targeted in the future.

Second, management is likely to improve governance structures and performance due to their concern for career paths. Management is less likely to be invited to other boards or other prestigious positions when targeted by activists (Grundfest, 1992). The literature on outside directors shows that vigilant directors are assessed as good monitors, which contributes to a positive reputation. This type of reputation confers them additional board seats and prestigious positions. In contrast, negligent directors lose reputation and are unlikely to be appointed to other boards (Fama and Jensen, 1983; Fich and Shivdasani, 2007). Because NPS targeting implies that management made shareholder value-destroying decisions, the target firmŌĆÖs management would experience a decline in its reputation. Therefore, it is unlikely to be appointed to other boards or other prestigious positions. To restore its reputation and prevent jeopardizing future career opportunities, the target firmŌĆÖs management would improve corporate governance structure. All things considered, we can reason that the stock market would react positively to the NPSŌĆÖs veto pre-announcements.

A competing argument posits that shareholders do not expect future improvements and are concerned about the negative signal of the NPSŌĆÖs veto pre-announcements. The management ignores ŌĆ£vote noŌĆØ announcements and not initiate any reforms (Grundfest, 1992) if they think the impact of a veto announcement is negligible. In many Korean firms, controlling shareholdersŌĆÖ opinion is more influential than institutional investorsŌĆÖ opinion. Even if controlling shareholders and their families own small amounts of shares, they maintain control using pyramidal, or circular patterns of ownership (Joh, 2003). Hence, investors might assume that the NPS does not have enough power to bring about changes in target firms. Investors might emphasize the fact that the firm is engaging in shareholder value-destroying behavior. From this point of view, the stock market would interpret the NPSŌĆÖs veto pre-announcements as a negative signal that indicates the NPSŌĆÖs dissatisfaction with management. Thus, the stock market would react negatively to the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-announcements (Kim and Yon, 2014; Sohn and Bae, 2018). Since both positive and negative responses are expected, the paper empirically tests whether the stock market responds positively or negatively to the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-announcements.

2.2.2 The Role of Publicity

The media is an external constituent that shapes public opinion. Hence, the influence of media needs to be examined when studying stock market responses. Publicity over pension fund activism spreads information about the NPSŌĆÖs pre-announcements, but there are conflicting views about the effects of publicity. From one perspective, extensive media coverage about the NPSŌĆÖs veto disclosure could increase shareholder wealth by promoting target firms to improve governance structure and firm performance. If shareholders assume that media coverage initiates such improvements, the stock market will show a positive reaction to news about the NPSŌĆÖs veto pre- announcements. The ŌĆ£vote noŌĆØ announcement implies that the NPS is dissatisfied with the current managementŌĆÖs decisions and signals that the firm is engaging in shareholder value-destroying behavior (Del Guercio et al., 2008; Ertimur et al., 2010; Kim and Yon, 2014; Sohn and Bae, 2018). If the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-announcements receive considerable media attention, the management feels a sense of shame because their prestige is damaged. Since directors and managers are sensitive to reputational damage (Grundfest, 1992), they might voluntarily reform corporate governance structure. The degree of shame would heighten as publicity increases. Therefore, when publicity is high, shareholders expect improvements in the governance structure, and such expectations lead to a positive stock market response. An interview with Richard Koppes, a former Chief Counsel of CalPERS, supports this view. Koppes stated that publicity is a powerful tool to gain leverage with management and that the mediaŌĆÖs attention to governance promoted market-wide changes (Del Guercio and Hawkins, 1999).

Not only a shame but also pressure from the public might cause corporate governance reform. The media renders public opinion by drawing peopleŌĆÖs attention to certain issues that would otherwise go unnoticed (McCombs and Shaw, 1972). Through public opinion, the media shapes the public image of corporations. Firms conform to social norms and behave in a way that is considered desirable to avoid being negatively reported in the media and having a negative public image (Dyck and Zingales, 2002). News about the NPSŌĆÖs veto pre-announcements denotes the NPSŌĆÖs negative evaluation of target firms and can harm the target firmsŌĆÖ public image. If the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-disclosures are extensively covered in the media, the management feels pressure to reform governance structure in a legally and socially appropriate way. Previous studies found that media reports about a firm substantially influence its managersŌĆÖ decisions. For instance, media coverage about a firm can change its strategy (Bednar et al., 2013) and make the firm more responsive to shareholdersŌĆÖ demand (Dyck and Zingales, 2002). To sum up, when the NPSŌĆÖs veto pre-announcements are covered in the media, the management will feel a sense of shame and feel pressure to reform governance structure in a socially and legally appropriate way. Hence, shareholders might expect that the management will improve corporate governance, and such expectation would cause a positive stock market reaction.

Another view states that publicity decreases shareholder wealth because news about the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-announcements spreads negative information about target firms and because shareholders do not expect that the target firmsŌĆÖ governance structure will be improved. A signal spreads further in the public when it is covered extensively in the media (Andrews and Caren, 2010). If the media works as a mechanism to diffuse negative information about target firms (i.e. the NPSŌĆÖs dissatisfaction with the management), then extensive media coverage regarding the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-disclosure will result in negative stock market reactions. A past study has found that negative news about a firm decreases its market value. DeAngelo et al. (1994) showed that negative media coverage of First Executive CorporationŌĆÖs investment in junk bonds caused a sharp decrease in its market value, even though the market value of similar firms that were also invested in junk bonds did not sharply decline.

Moreover, shareholders might not expect future improvements despite the NPSŌĆÖs veto pre-announcements being covered in the media. Media attention lasts for a short period of time and hence might not exert enough pressure on the target firmŌĆÖs management to change governance structures or increase performance. Time and effort are required to improve corporate governance, and the duration of media attention would not long enough to enhance corporate governance (Kim et al., 2014). Therefore, itŌĆÖs possible that publicity is negatively associated with stock market reactions. Because the stock market response is predicted in both positive and negative directions, the paper examines which direction is correct.

3. Methods

3.1 Data and Sample

Our sample consists of firms for which the NPS announced its voting decisions ahead of the annual meetings. To define target firms, we searched newspaper articles, the Voting Information Plaza website, and the NPS website. Newspaper articles are collected from BIGKINDS, the Korean news archive maintained by the Korea Press Foundation (Choi et al., 2016). Financial and stock price data are collected from DataGuide.

The NPS pre-announced to veto 101 agendas of 48 firms. The authors exclude two firms - Hyundai Motors and Hyundai Mobis - and the final sample consists of 46 firms. Most of the agendas the NPS vetoed are management proposals, while the vetoed agendas of these two firms are shareholder proposals. Vetoing management proposals and vetoing shareholder proposals deliver different meanings to the market. Vetoing management proposals implies that the NPS is not satisfied with the current managementŌĆÖs decisions or corporate governance structure while vetoing a shareholder proposal means that the NPS disagrees with the shareholders who proposed the agendas. The paper explores the relationship between the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-announcement and the stock market reaction. The critical factor determining the stock market reaction is the prediction of investors regarding whether the management improves corporate governance structure. Because vetoing shareholder proposals does not represent the NPSŌĆÖs stance on the managementŌĆÖs decisions and thus does not directly related to the arguments of this paper, the authors exclude the two firms.

3.2 Measures

3.2.1 Dependent Variables

We use an event study methodology to measure the stock market reaction to the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-announcement. The event day is defined as the day after a ŌĆ£vote noŌĆØ pre-announcement. The NPS announced its voting decision in the late afternoon or at night, after the stock market had closed. Hence, the opening price on the day after the announcement contains the effect of the NPSŌĆÖs proxy voting announcement without any contaminating factors. We first collected each firmŌĆÖs daily adjusted opening price and used the market adjusted model to estimate abnormal returns. Because most firms hold annual shareholder meetings in late March, events are clustered in our analysis. When events are clustered, the market adjusted model gives less biased results than the market model (Kim and Yon, 2014).

Market adjusted abnormal returns (AR) are calculated by subtracting daily market returns from daily stock returns of each company. Cumulative abnormal returns (CAR) are the sum of the ARs during the event window. The event window in our study is four days, including the event day itself plus the three preceding days. Many firms in our sample held annual shareholdersŌĆÖ meetings soon after the NPS announcements. If the event window included the days after the shareholdersŌĆÖ meetings, decisions made at the meetings would affect the event study result. To single out confounding factors, the authors do not include the days after the announcement in the event window. The specification to test the hypotheses is as follows:

3.2.2 Independent Variables and Control Variables

Our main independent variable is publicity, which measures the degree of media coverage at the firm level. We collected newspaper articles about the NPSŌĆÖs vote no pre-announcements and counted the number of articles published between the ŌĆ£vote noŌĆØ announcement time and the subsequent dayŌĆÖs stock market opening time. Only news articles published during this time affect the subsequent dayŌĆÖs opening price. Publicity is a dummy variable that takes the value of one if the number of news articles is higher than the median and zero otherwise.

Control variables include firm size, the NPS ownership ratio, past performance, dividend ratio, and debt ratio. Firm size is the log of total assets, and NPS ownership is a dummy variable that takes the value of one if the NPS ownership is higher than the median and zero otherwise. Past performance is the past five-year average ROE, and dividend ratio is a dummy variable that takes the value of one if the cash dividend divided by asset is higher than the median value and zero otherwise. The debt ratio is the past five-year average of debt divided by asset. All explanatory variables are lagged by one year.

4. Results

4.1 Determinants to ŌĆ£Vote noŌĆØ

Before analyzing the stock market response and the effect of publicity, we examine the determinants of the NPSŌĆÖs veto. The <Table 2> shows that, in general, the NPS disapproved because they were discontent with the severance pay arrangements, the limit on the remuneration of directors, and the election of directors and auditors. The most disapproved agenda type is the executive severance pay arrangements. Its disapproval rate amounts to 70 percent. The reason for disapproval is that the target firms gave excessive severance pay to executives (<Table 3>).

<Table┬Ā3>

Stated Reasons to ŌĆ£vote noŌĆØ

This table presents the NPSŌĆÖs stated reasons to ŌĆ£vote noŌĆØ by agenda type.

The disapproval rate regarding the limit on the remuneration of directors greatly increased compared to previous years. In the 2019 proxy season, 28 pre-disclosed agendas were disapproved, and the disapproval rate was 30 percent (<Table 2>). From 2005 to 2014, the NPS disapproved 39 agendas, and the disapproval rate was 1.17 percent (Lee et al., 2017), and from 2006 to 2009, it disapproved 18 agendas (Kim et al., 2014). The NPS stated that it disapproved because the suggested compensation was inappropriately high, considering firm performance (<Table 3>). The disapproval rate and the reasons to vote no implies that the NPS views the managers as entrenched. It also demonstrates that the NPS is making an effort to reduce managerial entrenchment through active monitoring and the adoption of a stewardship code.

The election of directors and auditors accounts for more than half of the total disapproved agendas (<Table 2>). The major reason to vote no is that the candidates are not independent of management (<Table 3>). Managers are inclined to elect directors and auditors with whom they can cooperate and are reluctant to elect those who are fully independent and capable of actively monitoring managers. By voting no to candidates who lack independence, the NPS tries to improve corporate governance structure.

4.2 Stock Market Response and the Role of Media

<Table 4> reports descriptive statistics for the final sample of 46 target firms. Because publicity is an important variable in this study, <Table 4> presents the descriptive statistics of the number of news articles. Its standard deviation is larger than other variables. We can infer that some firms are extensively covered in the media while others barely caught attention.

<Table┬Ā4>

Descriptive Statistics

This table reports descriptive statistics for the final sample of target firms. Mean, standard deviation, minimum, median, and maximum values are presented. The sample includes 46 firms. Definitions for each of the variables are given in <Table 1>.

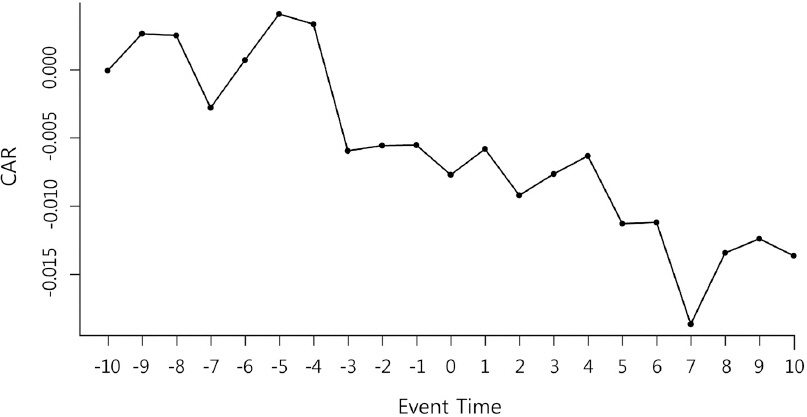

In <Table 5>, Panel A shows the event study results. The first row of Panel A in <Table 5> shows that the average four-day cumulative abnormal returns (CAR (-3, 0)) is -1 percent, which is significantly different from zero with p values below five percent. The results indicate that the stock market reacts negatively to the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-announcements. The stock market interprets the ŌĆ£vote noŌĆØ announcement as a negative signal that reflects the NPSŌĆÖs dissatisfaction with current management, and assumes that managers are engaging in shareholder value-destroying behavior. The CARs are also graphed in <Figure 1>. As days get closer to an event day, CAR tends to decrease, which suggests the negative stock market response.

<Table┬Ā5>

Event Study Results

Panel A reports the average four-day cumulative abnormal returns (CAR (-3,0)) associated with the announcement of the NPS targeting a firm. The event window includes the event day itself plus the three preceding days. Cumulative abnormal returns are calculated using the market adjusted model. The first row of Panel A presents the average four-day cumulative abnormal returns of all target firms. The second and the third row of Panel A report the average four-day cumulative abnormal returns of firms with low publicity and those of firms with high publicity, respectively. Panel B presents the univariate comparison between the low publicity group firms and high publicity groups firms. Publicity indicates the degree of media attention a target firm receives and is defined in <Table 1>. t values are in parenthesis. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

<Figure┬Ā1>

Cumulative Abnormal Returns (CARs) around the NPSŌĆÖs Pre-Announcement

The figure presents the averages of cumulative abnormal returns during the 21 trading days around the event day. Abnormal returns are based on the market adjusted model.

The results further suggest that the market evaluates management as entrenched and adversarial to institutional investors. If the market presumed that management was shareholder oriented and kept a friendly relationship with institutional investors, the market would assume that management acknowledges problems the NPS pointed out. Hence, the market would expect that the target firms reform corporate governance structure and would react positively to ŌĆ£vote noŌĆØ announcements. However, because the market suspects that management is entrenched and takes an adversarial position to institutional investors, the market does not expect future improvements. The results also validate the claim that investors assume that the NPS is not powerful enough to exert its influence on controlling shareholders.

To examine the effect of publicity on the stock market, stock reactions for subsamples of target firms are analyzed. The second row of Panel A in <Table 5> reports that the average CAR (-3, 0) of target firms that received little media attention is -2 percent, which is significantly different from zero at the one percent level. The third row shows that the average CAR (-3, 0) of target firms that received extensive media attention is 0.4 percent, which is statistically insignificant. The results suggest that the negative response is driven by firms in low publicity groups and that extensive media coverage mitigates the negative market response, increasing shareholder wealth.

The results presented in Panel B of <Table 5> demonstrate that the average CAR (-3, 0) of low publicity group firms and that of high publicity group firms are significantly different at the five percent level. The results confirm that the two groups show significantly different average CAR. In sum, <Table 5> shows that the stock market responds negatively to the NPSŌĆÖs veto pre-announcements and that media attention to the NPSŌĆÖs activism induces positive market response.

<Table 6> presents the OLS regression results using the CAR (-3, 0) as a dependent variable. The results are similar to univariate results in <Table 5>. The coefficient of publicity in Model 1 and Model 2 is 0.024 and 0.022, both significant at the five percent level. The results show that the CAR of firms that received high publicity is 0.02 higher than the CAR of firms that received low publicity. In other words, the higher the publicity, the higher the CAR is. High publicity mitigates the negative stock market response, suggesting that investors expect future improvements when the NPSŌĆÖs ŌĆ£vote noŌĆØ activities are highly covered in the media. Management feels ashamed when ŌĆ£vote noŌĆØ announcements are heavily covered in the media because veto announcements are a public expression of the NPSŌĆÖs discontent (Grundfest, 1992). To sum up, investors interpret the NPSŌĆÖs ŌĆ£vote noŌĆØ announcement as a negative signal that the current management is engaging in shareholder value-destroying behavior. Investors expect future improvements in corporate governance when the ŌĆ£vote noŌĆØ announcement receives high publicity.

<Table┬Ā6>

Regression Results Using CAR (-3, 0) as a Dependent Variable

The table reports results for OLS regression for the sample of 46 target firms. The dependent variable is the average four-day cumulative abnormal returns (CAR (-3, 0)). The independent variables are (1) publicity, (2) firm size, (3) NPS ownership, (4) past performance, (5) dividend ratio, (6) debt ratio. <Table 1> provides definitions for the variables. t values are in parenthesis. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

Among control variables, firm size is worth noticing. Generally, firm size is positively correlated with media coverage (Batten and Vo, 2015; Bushee and Miller, 2012). However, Model 2 shows that publicity and firm size influence CAR (-3, 0) in the opposite direction; while publicity has a positive effect, firm size has a negative effect on the stock market. We can infer that large firms are visible in the stock market and thus receive more attention than small firms. Hence, a negative signal could be amplified for large firms. Although publicity can shame and pressure management by widely publicizing the NPSŌĆÖs discontent, firm size is not a driver for improvement.

4.3 Additional Analyses

4.3.1 The Event Study using the Market Model

In addition to the major analysis, the authors conducted the event study using the market model. We estimate the market model parameters over the 200-day period, ending 20 days prior to the NPSŌĆÖs announcements. The results are in <Table 7> and are similar to the market adjusted model results. As for the stock market response, the event study using the market model also indicates that the stock market reacts negatively to the NPSŌĆÖs ŌĆ£vote noŌĆØ announcements. The first row of Panel A in <Table 7> shows that the CAR of the average four-day event window (-3, 0) is -1 percent, which is significantly different from zero with p values below five percent.

<Table┬Ā7>

Event Study Results Estimated by the Market Model

Panel A reports the average four-day cumulative abnormal returns (CAR (-3,0)) associated with the announcement of the NPS targeting a firm. The event window includes the event day itself plus the three preceding days. Cumulative abnormal returns are calculated using the market model. The first row of Panel A presents the average four-day cumulative abnormal returns of all target firms. The second and the third row of Panel A report the average four-day cumulative abnormal returns of firms with low publicity and those of firms with high publicity, respectively. Panel B presents the univariate comparison between the low publicity group firms and high publicity groups firms. Publicity indicates the degree of media attention a target firm receives and is defined in <Table 1>. t values are in parenthesis. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

Regarding the effect of publicity on the stock market, the market model results also indicate that media coverage alleviates the negative stock market response and increases shareholder return. The second row of Panel A in <Table 7> reports that the average CAR (-3, 0) of target firms that received little media attention is -2 percent, which is significantly different from zero at the one percent level. The third row shows that the average CAR (-3, 0) of target firms that received extensive media attention is 0.3 percent, which is statistically insignificant. The results presented in Panel B of <Table 7> illustrate that the average CAR (-3, 0) of low publicity group firms and high publicity group firms are significantly different at the five percent level.

4.3.2 The Event Study of Firms that the NPS did not Veto

The paper further examines whether the negative stock market response is driven not by the NPSŌĆÖs pre-disclosure to ŌĆ£vote no,ŌĆØ but just by the pre-disclosure. An event study is conducted using a sample of firms for which the NPS disclosed proxy voting decisions ahead of 2019 annual meetings but did not announce to veto. The 48 firms are in the sample, and two firms are excluded because they were not listed during the estimation period. The final sample includes 46 firms. The market model parameters are estimated over the 200-day period, ending 20 days prior to the NPSŌĆÖs announcements. In the third column of <Table 8>, the average CAR (-3, 0) of the market adjusted model is 0.4 percent, and the average CAR (-3, 0) of the market model is 0.2 percent, both of which are statistically insignificant. The results suggest that the pre-announcement itself does not affect the stock market reaction. The first column of <Table 8> shows the event study result of the total firms that are the subjects of pre-announcements. The average CAR (-3, 0) is not significant, which also indicates that the results of our main analysis is not caused by the pre-disclosure but caused by the NPSŌĆÖs pre-disclosure to ŌĆ£vote no.ŌĆØ

<Table┬Ā8>

Event Study Results of the Total Firms the NPS Pre-announced Its Voting Decisions

The first column reports the average four-day cumulative abnormal returns (CAR (-3,0)) of the firms that are the subjects of pre-announcement. The second column presents the average four-day cumulative abnormal returns of firms for which the NPS pre-announced to veto agendas of 2019 annual shareholder meetings. The third column reports the average four-day cumulative abnormal returns of firms for which the NPS pre-announced its voting decisions but did not veto. The fourth column shows the differences of the mean CAR (-3, 0) between firms for which the NPS pre-announced to vetoed agendas of 2019 annual shareholder meetings and the firm for which the NPS pre-announced its voting decisions but did not veto. For each of the four columns, the first row reports the market adjusted model methodology results, and the second row reports the market model methodology results. t values are in parenthesis. *, **, and *** indicate statistical significance at the 10%, 5%, and 1% level, respectively.

The fourth column of <Table 8> presents the difference between the average CAR (-3, 0) of the firms the NPS vetoed agendas and that of the firms the NPS did not veto. The difference is statistically significant at the ten percent level when we used the market adjusted model methodology. However, when we used market model methodology, the difference between the two groups is statistically insignificant. The result that the two groups have different average CAR (-3, 0) confirms the key assumption of this paper - people regard voting yes as an empty ritual (Grundfest, 1992) and are indifferent about voting yes.

5. Discussion and Conclusion

This study examines how the stock market responds to pension fund activism. The stock market showed a negative reaction to the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-announcements. Rather than expecting future improvements on governance structure or firm performance, shareholders pay attention to the fact that the NPS is dissatisfied with management. Shareholders assume that the target firmsŌĆÖ management made shareholder value destroying decisions. Since shareholders are concerned about the negative message the NPSŌĆÖs veto implies, the stock market shows a negative response.

We further analyze the role of publicity in the stock market. When the NPSŌĆÖs ŌĆ£vote noŌĆØ pre-announcements are highly covered in the media, the stock market showed a positive reaction. Because managers feel ashamed when the NPSŌĆÖs disapproval receives widespread media coverage, shareholders expect that management will improve corporate governance structure.

A major contribution of this study is that it utilizes a policy change regarding the NPSŌĆÖs proxy voting decision. Our study is one of the first studies that successfully examined the stock market reaction to shareholder activism. We show that investors respond even to a low cost mechanism of activism, namely ŌĆ£vote noŌĆØ announcements. These results suggest that investors will also show a meaningful response to more costly activism tactics.

This paper also highlights the value of using publicity for pension fund activism. Investors do not expect management to initiate any changes following the NPSŌĆÖs activism. However, if the NPSŌĆÖs activism is heavily covered in the media, investors will assume that managers would be pressured to improve their corporate governance.

The limitation of the study is its small sample size. As 2019 is the first year the NPS pre-disclosed its proxy voting decisions, we have a small sample size and are not able to extend the sample period. However, we can extend our sample in future studies as this practice continues. The second limitation of this study is that it does not examine the long term valuation effects of shareholder activism. This limitation also arises from the fact 2019 is the first year of pre-disclosing voting decisions. In future studies, we can examine whether firm value increased in the long term. The third limitation of our study is that we do not compare the event study results using pre-announcement date, shareholdersŌĆÖ meeting date, and proxy mailing date as an event date. Comparing the results of these three different event dates would highlight the value of using pre-announcement date as an event date. The future study could compare the three event dates to find the most significant one.

Institutional activism in Korea is at a nascent stage, with the NPS taking a leading role to increase institutional activism in Korea. The NPS enthusiastically engages in institutional activism, with the expectation that it can improve the governance structures of Korean firms and as a result, shareholder wealth. However, concerns about the NPSŌĆÖs activism remain. The possibility of pension socialism is the most urgent concern that needs to be resolved. To become fully independent from the Korean government, the NPS needs to consider reforming its governance structure. By doing so, the NPS will be free from concerns about pension socialism and can thus, engender positive changes in the Korean financial market.