1. 서론

주식시장에서 가격발견(price discovery)이란 주가가 기업정보를 반영하는 과정을 의미하며 (O’Hara, 1995), 새로 획득한 정보의 반영(information acquisition)이라든지 아니면 기존 정보를 반영하는 효율성(information efficiency)이 이를 결정하는 요소라 알려져 있다(Brogaard and Pan, 2022). 주가라는 게 자본주의 사회에서 한정된 자원을 효율적으로 배분하는 핵심 기제 역할을 하므로 가격발견은 거래소 기능 중에서도 가장 중요하다.1) 이에 세계 주요 거래소는 효율적인 주가 발견을 항시 염두에 두고 시장 미시구조를 설계·운영한다. 투자자의 하루 의사 결정에 잣대가 되는 ‘시가’(opening price) 단일가매매(call auction)는 거래소의 이같이 세심한 운영 철학을 엿볼 수 있는 좋은 예이다.2)

2019년 4월 29일 한국거래소(KRX: Korea Exchange, 이하 ”KRX”)는 유가증권시장 시가 단일가매매 호가접수시간을 기존 1시간(08:00~09:00+)에서 30분(08:30~09:00+)으로 단축 하였다. 1998년 12월 7일 1시간 30분 접수하던 것을 1시간으로 단축한 이후 20여 년 만에 시행한 제도 변경으로, 그 사이 온라인 거래 위주로 바뀐 시장환경을 고려해 가격발견 기능과 시장 운영 효율성을 높이려는 이유에서였다.3) KRX처럼 불특정 다수 투자자 간 주문 경합만으로 체결이 이루어지는 주문주도형 시장(order-driven market)에서 정보 생성과 적시 확산은 가격발견 효율성을 확보하는 데 더없이 중요한 요소이다. 수작업 당시는 말할 것도 없고 전산 자원이 지극히 제한적이던 1980년대 후반까지만 해도 호가 접수, 집계, 게시 및 체결에 필요한 시간이 지금보다 당연히 길게 필요했었고 정보 생성과 확산 속도도 훨씬 더 더뎌서, 만일 호가접수시간이 짧았더라면 오히려 가격발견에 방해가 되었을 것이다. 반면, IT가 급진전한 1990년대 후반부터 정보는 인터넷, 모바일 기기 등을 통해 매우 빠르게 생성·확산하기 시작하였다. 예로써, 모바일트레이딩시스템(MTS: mobile trading system)을 통한 주문이 일반화하면서 투자자는 시간과 장소에 구애받지 않고 정보를 취득하며 주문을 제출할 수 있게 되었다.4) 또한 글로벌 주요 주식시장에서는 호가접수시간을 대부분 30분 이내로 짧게 해 주문주도형 시장을 운영한다(<표 3> 참조).5) KRX 유가증권시장의 호가접수시간 단축은 이처럼 시장환경 변화에 따른 시장 운영 개선, 글로벌 주요 주식시장과의 정합성 등을 고려한 조치였다.

이 논문은 KRX 유가증권시장이 2019년 4월 29일 행한 시가 단일가매매 호가접수시간(이하 ”시가 단일가매매시간”) 30분 단축 조치가 가격발견을 개선하는 데 유용했는지를 분석 규명한다. 여느 시장과 마찬가지로 유가증권시장 시가 단일가매매에서도 시가 확정 전까지는 매매체결이 이루어지지 않는다. 대신, 투자 판단에 도움을 주고자 실시간으로 참조용 ”예상체결가격” (indicative price)과 ”예상체결수량”(indicative volume)을 계산·공표한다. 예상체결가격과 예상체결수량이란 시가 단일가매매시간에 호가가 접수될 때마다 그 시점에 단일가매매 체결 원칙에 따라 매매체결 한다면 형성될 것으로 예상하는 가격과 수량을 의미한다. 구체적으로, 이 논문에서는 유가증권시장 시가 단일가매매시간 단축을 사건(event)으로 하여 이렇게 공표되는 예상체결가격이 체결 시점(즉, 개장 시점)에 확정되는 균형가격(equilibrium price)을 사건 전후로 얼마나 정확하고 신속하게 대변하는지, 가격발견 개선을 목적으로 조치했는데 사건 발생 후에 실제 이 같은 효과가 나타났는지를 분석한다.

이 논문에서 분석은 두 가지 방법을 사용한다. 하나는 Biais et al.(1999)이 처음 사용한 방법으로 전일종가대비 시가와 예상체결가격 변화율을 각각 종속변수와 독립변수로 한 ”불편회귀분석”(unbiased estimation)이다. 시가 단일가매매시간대별 불편회귀분석 계수(이하 ”불편회귀계수”) 추정치 변화를 관찰함으로써 이른바 예상체결가격의 ”학습과정가설”(learning process hypothesis)을 검증해볼 수 있다. 이 가설에 따르면 예상체결가격이 전일종가 이후 발생하는 정보를 하나도 반영하지 못하거나(즉, 순수하게 잡음[noise]이거나) 기존에 발생한 정보를 전혀 효율적으로 반영하지 못한다면 불편회귀계수 값은 0에 수렴한다. 반대로 예상체결 가격이 전일종가 이후 발생한 새로운 정보를 온전히 반영하거나 기존에 발생한 정보를 완전히 효율적으로 반영한다면 불편회귀계수 값은 1로 수렴한다. 다른 하나는 Barclay and Warner (1993)6)가 소개한 방법으로 ”가중가격공헌도”(WPC: weighted price contribution)를 사용해 가격발견 속도를 측정·분석한다. WPC는 먼저 해당 종목의 전일종가대비 시가 수익률에서 해당 시간대가 이 시가 수익률에 공헌한 정도를 구한 후, 이를 해당 종목의 분석 기간 전체 정보 유입량에서 해당 일 정보 유입량을 가중치로 곱해 계산한 값이다(식 (2) 참조). 시가 단일가매매시간 중 해당 시간대가 시가라는 균형가격 발견에 공헌한 정도를 측정하고 시간대별 변화를 통해 가격발견 속도를 파악한다.

시가 단일가매매 동안 일어나는 가격발견에 관한 국외 연구는 ① 학습과정가설 검증과 ② 가격발견 속도나 정도, 또는 관련 정보성 등 특성 분석으로 크게 나눌 수 있다. 전자는 불편회귀분석을, 후자는 WPC를 각각 분석 방법으로 사용한다. ③ 파생상품거래 종가 결정 방식 변경 효과를 분석하며 비교 대상으로 시가 단일가매매를 분석하기도 하지만, 이 논문의 목적과 연결하기에는 얻고자 하는 경제적 의미나 분석 방법(예: 주가 반전[price reversal])이 사뭇 다르다(예: Chang et al., 2020; Lei et al., 2021; Park et al., 2022). 학습과정가설 검증은 파리거래소(Paris Bourse, 현재 Euronext Paris, Biais et al., 1999)와 KRX(Eom et al., 2021)를 대상으로 이루어졌으며 두 연구 다 이 가설을 지지하는 결과를 제시한다. 가격발견 특징 분석과 관련해서는 런던증권거래소(LSE: London Stock Exchange) 시가 결정에서 단일가매매(경쟁 매매 메커니즘)가 딜러매매(딜러 메커니즘)보다 가격발견을 더 정확하게 한다는 연구(Ellul et al., 2005)와 나스닥(Nasdaq) 개장 전 시장(pre-opening market)에서 시장조성자의 크로쓰 (cross, 매수호가가 매도호가보다 높은 경우)와 록(lock. 매수호가와 매도호가가 같은 경우)이 중요 정보를 제공한다는 연구(Cao et al., 2000)가 대표적이다.

국내에서 시가 단일가매매 동안 예상체결가격을 사용해 가격발견을 분석한 연구는 Eom et al.(2021)이 유일하다. 이들은 시가·종가 단일가매매에 부가된 ‘임의종료(random-end)’ 방식7)이 시가 결정에서는 가격발견과 시장안정화에 효과적이었으나 종가 결정에서는 이에 못 미쳤다고 보고한다. 이에 비해, 이 논문은 국내외 통틀어서 처음으로 시가 단일가매매시간 단축이라는 ‘제도 변경’을 사건으로 해 사건 전후 시가 단일가매매의 가격발견 효과와 속도를 비교 분석한다. 시가 단일가매매시간은 전일 장마감 이후 발생한 정보가 한꺼번에 몰리면서 당일 주가 향방에 큰 영향을 미치는 아주 중요한 거래 시간대이다. 만일 이 시간대 단축이 시가 균형가격을 제대로 형성해주지 못하면 이는 계속해 정규거래시간대 가격발견에도 영향을 미칠 것이다. 반대로 시가 균형가격을 제대로 형성하면 시간대 단축은 시가 단일가매매 운용 효율성을 크게 개선해주는 조치일 것이다. 제도 변경 이전 세계 주요 주문주도형 거래소의 시가 단일가매매시간은 1시간인 일본을 제외하고 모두 30분 이내였다(<표 3> 참조). 1시간에서 30분으로 시간 단축 효과를 분석한 이 논문은 시가 단일가매매 운용 효율성에 대해 아주 의미 있는 정책 시사점을 제공한다.

이 논문에서 분석 기간은 2019년 4월 29일 제도 변경 사건일 전후 50 거래일(2019.2.25.~ 2019.7.10.)이다. 유가증권시장 상장 보통주를 대상으로 하며 예상체결가격 자료를 분석에 사용한다.

주요 결과는 다음과 같다. 첫째, 불편회귀분석 결과, 사건 이전 이후 모두 예상체결가격 불편회귀계수 값은 ‘전반적으로’ 계수 반전 없이 체결 시점에 이를수록 가파르게 계속 상승하며 1로 수렴한다(<표 5>, <그림 1> 참조). 유가증권시장에서 학습과정가설이 시간 단축 여부와 상관없이 강건하게 지지받는다는 결과이다. 또한 둘 다 계수 값이 개장 시점 직전인 9:00 정각에 평균 0.96~0.97일만큼 매우 높고 30초 내(9:00:30 내)라는 아주 짧은 시간이지만 임의종료로 0.03~0.04 계수 값에 해당하는 가격발견 효과를 보인다.8) 덧붙여 정보공개시간 1분 후 계수는 사건 이전(8:10부터 공개 시작) 0.1361에서 사건 이후(8:40부터 공개 시작) 0.1811로 증가하였다 (정보공개시간은 <표 3> 참조). 제도 변경 이전 제도 하에서 이 수준에 도달하려면 약 28분은 지나야 했으므로 이는 호가접수시간을 30분 단축했어도 시장 전체로 소요시간대비 가격발견 효과는 약해지지 않았음을 의미한다. 오히려 8시 58부터 개장 시점 직전까지는 사건 이후 계수 값이 사건 이전 계수 값을 넘어서기도 하였다. 종합해보면 사건 이후 시가 단일가매매의 가격발견 효과는 사건 이전 후반 30분과 최소한 같은 것으로 나타나 30분 단축 변경 조치는 시장 운영 효율성 개선에 일정 수준 유용했음을 알 수 있다.

둘째, WPC 분석 결과, 시가 단일가매매 예상체결가격의 가격공헌도는 사건 이전 이후 모두 ”역J자 패턴”(inverse J-shaped pattern)을 보였다. 체결이 일어날 수 없음에도 실거래가 발생하는 정규거래시간대에서와 비슷한 WPC 패턴(Eom et al., 2010)을 보인다는 게 꽤나 흥미롭다. 역J자 패턴은 사건 이후 곡선 기울기가 훨씬 더 가팔랐다. 사건 이전 호가개시 초반 15분까지 가격공헌도가 46.2%(8:15)였는데 사건 이후 79.0%(8:45)로 거의 1.7배 증가해, 시가 단일가매매시간 단축 이후 호가접수기간 초반의 가격공헌도가 훨씬 더 지배적이고 공격적으로 바뀌었음을 반영한다. 이는 또한 시가 단일가매매시간 초반부 가격발견 속도가 크게 향상된 것을 나타내주지만, 다른 한편으로는 그 속도가 너무 지나쳐(overshooting) 후반부 막판 5분간은 마이너스 WPC가 심화되어 균형가격을 찾아가는데 급격한 조정이 필요했음을 보여준다.

셋째, 유동성 수준별로 나누어 분석한 결과, 유동성이 제일 높은 그룹(Q5)의 불편회귀계수 값은 종목 전체를 분석한 경우와 비슷하게 수렴하였다. 이에 비해 유동성이 제일 낮은 그룹(Q1)에서는 사건 이후 계수 반전현상이 이전보다 크게 줄어들기는 했으나 시가에 수렴하는 정도(즉, 가격발견 효과)는 사건 이전보다 늦고 덜하였다. 시가 단일가매매시간 단축이 유동성이 낮은 종목의 가격발견에는 상대적으로 덜 효과적이었음을 시사한다. WPC 패턴도 대부분 그룹(Q5~Q2)에서 종목 전체를 분석한 경우와 비슷하였다. 하지만 이 역시 유동성이 제일 낮은 그룹(Q1)에서는 특이 현상을 보여, WPC가 다른 그룹에 비해 초반부에서는 현저히 낮고 30초간 임의종료시간에서는 가장 높았다.

논문 구성은 다음과 같다. 서론에 이어, 제2장에서는 시가 단일가매매 동안 가격발견 효과와 특징을 분석한 국내외 연구를 조사·정리한다. 제3장에서는 유가증권시장 시가 단일가매매 제도를 매매체결방법과 단일가매매 구성요소를 중심으로 설명한다. 제4장에서는 표본 선정과 분석 방법을, 제5장에서는 시가 단일가매매시간 단축에 따른 가격발견 효과와 속도를 비교 분석해 결과를 정리한다. 제6장에서는 결론과 함께 정책 시사점을 논하며 논문을 마무리한다.

2. 문헌 연구

국내외 재무학계에서 시가 단일가매매에 관한 연구는 분석에 사용한 방법론에 따라 분류·정리하면 의미 파악이 훨씬 수월하다. 방법론에 따라 단일가매매를 분석하는 측면이 서로 다르므로 단일가매매가 거래 메커니즘으로서 갖는 경제적 역할이나 의미를 구체적으로 파악할 수 있기 때문이다.

첫 번째는 불편회귀분석을 사용한 연구이다. Biais et al.(1999)이 시가 단일가매매 동안 Paris Bourse 예상체결가격의 가격발견 효과를 분석하며 최초로 사용하였다. 실증분석 결과, 불편회귀계수 값이 시가 체결 시점에 다가갈수록 1로 계속 상승 수렴하는 것으로 나타나 학습과정 가설을 지지하였다. 이 방법은 한국 자본시장 분석에도 사용되었다. Park et al.(2003)에 따르면 시가 단일가매매시간 8:45까지는 불편회귀계수 값 평균이 0.2 이하로 아주 낮지만, 이후부터 시가 체결 시점 9:00까지는 가파르게 상승하며 계수 값 평균이 0.7까지 수렴하였다(당시에는 임의종료 방식을 사용하지 않음). 이를 근거로 2001년 5월(분석 기간: 2001.5.2.~2001.5.31.) 유가증권시장에서는 학습과정가설이 어느 정도 지지받는다고 주장하였다. 하지만 데이터를 구할 수 없어 가중평균호가를 예상체결가격 대용변수(proxy)로 사용해야 했기에 시가 단일가매매 시간 역할에 대한 직접적인 결과를 제시하지는 못하였다. 한편, Eom et al.(2021)은 임의종료 방식에 초점을 두고 KRX 시가·종가 단일가매매 동안 가격발견 효과를 분석하였고, 그중 특정 분석에 불편회귀분석 방법을 사용하였다. 연구 결과, 분석 기간 당시 채택했던 ”조건부 임의종료 방식”9)은 시가에서 가격발견과 시장 효율성을 의미 있게 개선했으나, 종가에서는 이에 다소 못 미친다고 보고하였다.

두 번째는 WPC를 사용한 연구이다. Cao et al.(2000)은 Nasdaq 개장 전 시장에서 시장조성자 호가 중 cross와 lock의 WPC가 특히 커 시가 발견에 아주 중요한 정보를 제공할 뿐만 아니라 해당일 가격변동에서도 그 영향력이 상당 비중을 차지한다고 하였다. Ellul et al.(2005)에 따르면 런던증권거래소(LSE: London Stock Exchange)에서 시가와 종가를 결정할 때 단일가매매 메커니즘이 딜러 메커니즘보다 가격발견을 더 정확하게 하나 시가나 종가 체결률은 딜러 메커니즘보다 훨씬 저조하였다. 또한 시장참가자에게는 유동성이 높거나 기업규모가 큰 주식 일수록 단일가매매가 유용하고 기업규모가 작은 주식일수록 딜러매매가 유용하였다. 두 메커니즘의 전형적인 장점을 보여주는 결과이다. 한국주식시장에 대해서는 Eom et al.(2010)과 Seon and Lee(2015)가 주시장(유가증권시장)과 성장형시장(코스닥시장) 간 가격효율성을 비교하려 WPC를 사용하였다. 둘 다 시가 단일가매매시간이 아니라 정규거래시간을 분석 하였다.10) 그 결과, 코스닥시장의 가격발견 효율성은 유가증권시장보다 전체적으로는 낮지만, 코스닥시장 최상위 유동성 그룹에 속하는 40개 기업의 가격발견은 유가증권시장 유동성 순위 160~200위에 속하는 40개 기업과 속도, 정도, 정확도 측면에서 비슷하였다(Eom et al., 2010). 또한 코스닥시장의 가격효율성은 속도와 정도 측면에서는 유가증권시장보다 떨어지지만, 정확도에서는 뒤지지 않았다(Seon and Lee, 2015).

세 번째는 그 외 다른 방법론을 사용하여 시가 단일가매매를 분석한 연구이다. Madhavan and Panchapagesan(2000)은 자신들이 고안한 이론모형과 이에 기반한 회귀분석모형을 사용해 뉴욕증권거래소(NYSE: New York Stock Exchange)에서 스페셜리스트(specialist)의 존재는 100% 전산화된 단일가매매보다 시가 발견을 더 촉진해주는 긍정적 역할을 한다고 보고하였다.11) 이는 바로 위에서 서술한 Ellul et al.(2005)의 LSE 경우와는 뉘앙스가 다소 다른 결과이다. 이 밖에도 단일가매매에 부가하는 임의종료 방식이나(예: Eom et al., 2021; Hauser et al., 2012; Zimmermann, 2013), 파생상품 만기일 종가 결정 때 사용하는 단일가매매에 초점을 두면서(예: Chang et al., 2020; Lei et al., 2021; Park et al., 2022) 시가·종가 단일가매매의 가격발견이나 시장 효율성(예: 변동성 감소, 가격조작 감소)을 검증한 연구가 있다. 이들 연구에 따르면 시가·종가 결정에서 임의종료 방식 또는 단일가매매는 가격발견과 시장 효율성을 의미 있게 개선한다.

3. KRX 시가단일가매매 개요

3.1 매매체결 일반 원칙

KRX 주식시장은 주문주도형 시장으로 불특정 다수 투자자의 매도와 매수주문이 일정 원칙에 따라 경합하며 매매가 체결된다.12) 매매체결 원칙 1순위는 가격우선(price priority) 원칙이다. 매수에는 가격이 높은 호가가 낮은 호가에 우선하고, 매도에는 가격이 낮은 호가가 높은 호가에 우선한다.13) 2순위는 시간우선(time priority) 원칙으로 가격이 같은 호가 간에는 거래소 시스템에 먼저 접수된 호가가 나중에 접수된 호가에 우선한다. 단, 단일가매매 체결가격이 상·하한가로 결정될 때는 매수의 경우 상한가에 제출한 매수호가끼리, 매도의 경우 하한가에 제출한 매도호가끼리는 시간우선 원칙을 적용하지 않는다.14) 체결 가능성을 높이려고 더는 우선호가를 제출할 수 없는 가장 불리한 상·하한가로 호가했는데도 시간우선 원칙을 적용하면 고민 끝에 늦게 제출된 투자자의 주문은 체결되지 못할 수도 있다. 이러한 상황을 배려해 단일가매매에서 모든 상·하한가 주문은 늦더라도 동시에 제출된 것으로 간주한다.15)

3.2 단일가매매 체결방법

단일가매매는 ”단일가격에 의한 개별경쟁매매”의 준말로 일정 시간 접수한 호가를 가장 많이 체결할 수 있는 하나의 가격(“합치가격”이라 함)으로 체결하는 방식이다. 시가·종가 결정, 거래정지 후 재개, 변동성완화장치(VI: volatility interruption)와16) 같이 시장안정화장치 발동이나 기타 ”주기적 단일가매매 체결종목 매매체결”17) 등에 적용한다. 구체적으로는 합치 가격을 중심으로 다음에 해당하는 수량을 체결한다. ① 합치가격보다 낮은 매도호가와 합치가격 보다 높은 매수호가의 모든 수량, ② 합치가격 호가에서는 매도호가 또는 매수호가 중 어느 한쪽의 전 수량을 체결하고, 다른 한쪽 매매수량단위 이상의 수량을 체결한다(<표 1>참조).18) 이러한 합치가격은 2개 이상일 수 있는데 이때는 복수의 합치가격 중 직전 가격과 같은 가격이 있으면 그 가격으로, 없으면 가장 가까운 가격으로 체결해 가격연속성을 보장하도록 제도를 운용한다(<표 2> 참조).

<표 1>

일반적인 단일가매매 체결 방법 예시19)

단일가매매 기본원칙은 가장 낮은 매도주문과 가장 높은 매수주문을 순차적으로 체결해서 최종적으로는 거래가 가장 많이 이루어질 수 있는 하나의 가격(합치가격)에서 매매체결을 확정함. 아래 예에서 합치가격은 15,250원, 체결수량은 2,000주임. ① 합치가격 15,250원을 초과하는 매수호가 전수량, 이 가격 미만 매도호가 전수량이 체결되며(수량이 0인 것을 포함), ② 합치가격 15,250원에서는 매수호가 전수량과 매매수량단위(1주) 이상의 상대방 매도호가 수량이 체결됨. ○, ◑, ●는 각각 미체결 호가, 일부 체결호가, 전량체결호가를 나타냄.

| 매도 | 가격 | 매수 |

|---|---|---|

| 15,400 | ● 1000 | |

| ○ ○ | 15,350 | ● 300 |

| ○ ○ ○ | 15,300 | ● 200 |

| ○ ○ ◑ ● 2,000 1,000 500 100 | 15,250 | ● ● 200 300 |

| 150 ● | 15,200 | ○ ○ |

| 150 ● 500 ● | 15,150 | ○ |

| 500 ● | 15,100 | ○ ○ ○ |

| 150 ● | 15,050 |

<표 2>

단일가매매에서 합치가격이 2개인 경우 매매체결 방법 예시

단일가매매에서 합치가격이 2개인 경우에는 합치가격 중 직전 가격과 같은 가격이 있으면 그 가격을, 그렇지 않으면 직전 가격과 가장 가까운 가격을 체결가격으로 함. 이 예에서 합치가격은 15,300원과 15,350원인데 직전 가격(15,250원)과 가장 가까운 15,300원이 체결가격이 됨. 여기서 <표 1>의 단일가매매 합치가격 ②번 요건에 따르면 합치가격에서는 어느 일방의 전체 수량과 상대편 호가수량 중 매매수량단위(1주) 이상의 수량이 체결되어야 하는데 아래 예는 이 요건을 충족하지 못함. 그렇다 해도 합치가격이 이렇게 2개면 ②번 요건을 충족하지 않아도 합치가격으로 인정해 거래를 성립시킴. 자세한 내용은 유가증권시장 업무규정 제23조 제4항~제6항을 참조하기 바람.

| 매도 | 가격 | 매수 |

|---|---|---|

| 15,400 | ||

| 15,350 | ● 200 | |

| 200 ● | 15,300 | |

| <직전 가격> | 15,250 |

단일가매매는 체결 즉시성을 희생하는 대신 호가를 집적하여 일시에 체결함으로써 변동성을 낮추고 불공정거래도 일정 부분 예방할 수 있다고 알려져 있다. 하지만 그렇다 해도 글로벌 주요 거래소는 단일가매매 제도에 불공정거래 예방장치나 시장안정화장치 등을 추가로 설치해 시장 안정성을 더욱 강화하는 경향을 보인다.20)

3.3 시가 단일가매매, 구성요소와 특징

KRX 시가 단일가매매는 호가접수시간, 정보공개범위(즉, 투명성), 종료 방식, 시장안정화장치 운영 등 여러 요소를 결합해 주요국 거래소와 구분되는 자신만의 고유한 특징을 보인다. 각각의 구성요소와 특징을 살펴보면 첫째, 호가접수시간으로 기존에 1시간(08:00~09:00)을 하다가 2019년 4월 29일 30분(08:30~09:00)으로 단축하였다. 전일 장종료 이후 발생한 정보가 시가에 한꺼번에 반영되므로 적절한 호가접수시간 부여는 정보반영 효율성 측면에서 아주 중요하다. 만일 호가접수시간이 너무 길면 정보반영 신속성이 떨어져 효율성이 저해되고, 너무 짧으면 호가 집적에 따른 균형가격을 발견하기 어려울 수 있기 때문이다. 세계 주요 거래소는 각자의 시장 환경과 상황에 맞게 호가접수시간을 운영하는데 주문주도형 시장을 근간으로 하는 거래소는 대개 30분 내 시간을 부여한다(<표 3> 참조).

<표 3>

세계 주요 거래소 시가 단일가매매 운영 현황

세계 주요 주식거래소가 채택하고 있는 시가 단일가매매제도임. 호가접수시간, 정보공개시간, 종료 방식(고정 또는 임의종료), 부가한 시장안정화장치를 간략히 소개함. * Core Open Auction 기준임. 그 전에 03:30~04:00 사이에는 Early Open Auction이라는 세션을 운영하나 거의 활용하지 않는 것으로 알려짐.

<표 4>

시가 단일가매매시간 단축 전·후 호가와 체결데이터 현황

단축 이전과 이후 기간 각각 분석대상 종목 전체의 일평균 호가와 체결데이터임.

둘째, 상당한 수준의 투명성 그중에서도 사전적 투명성(pre-trade transparency) 제공이다. 주식시장 미시구조에서 사전적 투명성은 거래 체결 전에 투자자가 제출한 매도·매수주문과 관련 정보를 일반에게 공개하는 정도를 말한다(Eom et al., 2007). 적정 수준의 사전적 투명성은 투자자가 해당 주식의 본질가치를 판단해 최적 투자전략을 수립하는 데 필수 정보이다.21) KRX는 시가단일가매매 동안 예상체결가격과 예상체결수량, 최우선매도·매수호가를 포함한 3단계 우선호가와 해당 수량, 1~3단계 우선호가수량의 매도·매수별 합계를 공개한다.22)

셋째, ”정적 VI”(static volatility interruption) 적용이다. 정적 VI는 잠정체결가격이 직전 단일가격23) 대비 ±10% 이상 변동하면 체결을 종료하지 않고 단일가매매 주문접수시간을 2분 연장하는 제도이다. 추가 주문접수시간을 통해 투자자는 가격급변 상황을 점검해 제출했던 주문을 정정하거나 취소할 수 있고, 또 다른 가격대 주문을 새로 제출해 대응할 수도 있다.

넷째, 단일가매매 마감을 ”임의종료”(random end) 방식으로 처리한다. 단일가매매는 주문제출시점에 즉시 체결되지 않기 때문에 이를 악용해 불공정거래가 이루지기도 한다. 허수주문(spoofing)이 대표적이다. 예컨대 주식을 보유하고 있는 투자자가 해당 종목의 대량 매수주문을 제출해 예상체결가격을 끌어올린 후 단일가매매시간 마지막에 보유주식을 고가 매도주문으로 제출하고 동시에 제출했던 대량 매수주문을 취소해 인위적으로 시세보다 높게 매도하는 행위이다(Lee et al., 2013). 일부 거래소는 이러한 행위를 방지하고자 단일가매매 체결 시점 전 일정 시간동안 취소나 정정 주문 제출을 금지한다. 또한 단일가는 전통적으로 접수 마감 즉시(예: 09:00, 15:00 정각) 체결이 이루어지는데 임의시간 내 종료하여 허수주문 취소를 어렵게 하기도 한다. KRX는 2005년부터 시가 단일가매매를 조건부로 5분 내 임의종료하다가 2015년 6월 15일 이후 30초 내 무조건부 임의종료 방식을 사용한다(Eom et al., 2021).

정리해보면, 2019년 4월 시가 단일가매매시간을 단축함으로써 이제 KRX는 호가제출시간을 30분간(08:30~9:00+) 운영한다. 이와 더불어 상당 수준의 사전적 투명성을 제공하며, 불공정거래 방지 조치로 VI를 비롯한 시장안정화장치와 30초 내 임의종료 방식을 채택하고 있다. 이로써 DB, Euronext, LSE 등 유럽 주요 거래소와 비슷한 수준의 시가 단일가매매 제도를 구축·운영하고 있다.

4. 표본과 분석 방법

4.1 표본과 데이터 구성

이 논문의 실증분석 표본 기간은 2019년 2월 15일부터 7월 10일까지 약 5개월이다. 시가 단일가매매시간 30분 단축 사건일인 2019년 4월 29일을 전후로 각각 50 거래일, 총 100 거래일을 표본으로 한다. KRX 유가증권시장 상장 주권 중 우선주와 관리종목을 제외한 보통주만을 대상으로 하며, 자료 연속성을 담보할 목적으로 이 중 분석 기간 내 상장, 상장폐지, 매매거래정지가 발생한 종목은 표본에서 제외한다.

이외, 데이터 필터링(data filtering)은 다음과 같다. 시가 단일가매매 동안 예상체결가격이 시가에 이르는 가격발견 효과를 분석하기 때문에 매도·매수 불균형으로 예상체결가격이 형성되지 않거나 시가가 결정되지 않은 경우는 데이터 구성에서 제외한다. 분석의 유효성을 확보하고자 종목별로 사건일 전후 각 50일 분석 기간 중 20일 이상 관측치가 없으면 분석대상 종목에서 제외한다.

시가 단일가매매 호가접수시간 단축 이후 분석대상 종목의 일평균 호가건수와 수량, 체결건수와 금액은 모두 감소하였다(<패널 A> 참조). 이는 호가접수시간이 30분이나 단축됐기에 쉽게 예상할 수 있는 사항이다. 그런데도 체결수량은 단축 이후 증가했는데, 이는 단축 이후 시장 전체적으로 주문이나 거래가 증가했기에 나타난 현상으로 보인다(<패널 B> 참조). 따라서 분석 결과가 영향을 받을 만큼 사건 전·후 표본 데이터에 질적으로 급격한 변화는 발생하지 않았다.

4.2 분석 방법

4.2.1 가격발견 효과

이 논문에서는 예상체결가격의 시가 가격발견 효과 측정에 Biais et al.(1999)의 불편회귀분석 모형 식 (1)을 사용한다.

여기서 특정 종목별로 V는 관측일 시가단일가, Pt는 시간대별 예상체결가격, E(V\I0)는 관측일 전일종가, ∊t는 N(0, σ∊2)오차항을 각각 나타낸다. 따라서 종속변수는 관측일 시가의 전일종가대비 수익률, 독립변수는 관측일 특정 시간대(t. 관측 시점) 예상체결가격의 전일종가대비 수익률이다. 전체 종목을 대상으로 거래일별 특정 시간대 횡단면 회귀분석(cross-section regression)을 실시하여 구한 회귀계수를 전체 분석기간에 걸쳐 시계열 평균해 해당 특정 시간대 불편회귀계수 β ^ t

연구자마다 조금씩 다르게 해석하기도 하지만, 불편회귀계수 β ^ t

4.2.2 가격발견 속도

가격발견 속도 분석 방법으로는 Barclay and Warner(1993)의 WPC(가중가격공헌도)를 사용한다. 관측일(d) 특정 시간대(t)에서 WPC는 다음과 같이 계산한다.

여기서 ri,d는 특정 종목(i) 특정 관측일(d) 시가단일가의 전일(d-1) 종가대비 로그수익률 (ln(Pd,open)-ln(Pd-1,close))을, ri,t는 특정 종목 특정 관측일 시가 단일가매매 호가접수시간 중 특정 시간대 예상체결가격의 바로 전 시간대(t-1) 예상체결가격대비 로그수익률(ln(Pt)-ln(Pt-1))을 나타낸다. 측정일 전일종가대비 시가수익률에서 시가단일가매매 특정 시간대 예상체결가격 수익률이 공헌한 정도(price contribution)를 측정하되, 특정 종목 수익률 절댓값이 전체 종목 수익률 절댓값에서 차지하는 비중을 가중치(weight)로 부여해 계산한다. 이렇게 계산한 관측일 시점별 WPC를 전체 분석 기간에 걸쳐 시계열 평균하여 WPC를 추정한다.

특정 관측일에 어떤 종목의 수익률 절댓값이 크다는 것은 해당 종목에 새 정보가 많이 유입한 것으로 볼 수 있다. 따라서 가중치는 해당 관측일 전체 포트폴리오에서 해당 종목의 새 정보 유입량으로 해석할 수 있다. 따라서 WPC는 정보 유입량으로 가중 평균한 특정 시간대의 가격공헌도를 의미하고, 특정 시간대에서 WPC가 크다는 것은 균형가격을 발견해 가는 속도가 빠르다는 것으로 해석할 수 있다.

한편, 특정 시간대까지 WPC를 누적한 측정치인 ”누적가중가격공헌도”(CWPC: cumulative weighted price contribution)를 보조적으로 사용한다.

WPC가 특정 시간대 가격발견 속도를 측정하는 것이라면 CWPC는 예상체결가격 공개 시점(08:40)부터 특정 시간대까지 도달한 가격발견 속도로 해석할 수 있다.

5. 실증분석 결과

5.1 시가 단일가매매 예상체결가격의 가격발견 효과 변화

5.1.1 시장 전체 분석 결과

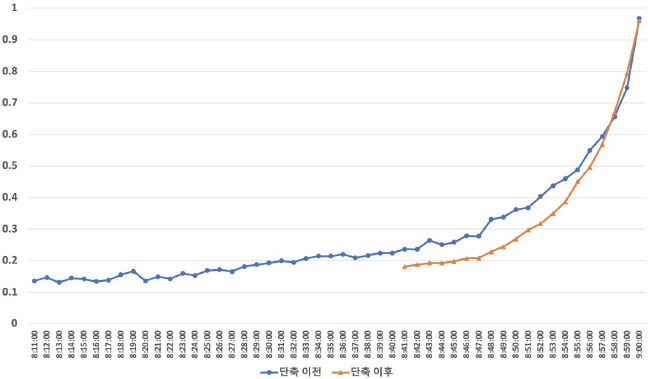

<표 5>와 <그림 1>은 유가증권시장 표본 종목 전체를 대상으로 불편회귀분석 모형 식 (1)을 추정해 얻은 1분 단위 불편회귀계수 결과이다. 불편회귀계수는 시가 단일가매매 동안 시간대별로 횡단면 회귀분석을 해 추정한 회귀계수를 표본 기간에 걸쳐 시계열로 평균한 값이다.

<표 5>

시간대별 불편회귀계수 평균 추이와 신뢰구간

유가증권시장 상장 전체 표본종목 대상으로 불편회귀분석 모형 식 (1)을 추정해 얻은 불편회귀계수 결과임. 불편회귀계수는 시가 단일가매매 동안 시간대별로 횡단면 회귀분석을 해 추정한 회귀계수를 표본 기간에 걸쳐 시계열로 평균한 값임. 신뢰구간은 이 시계열 회귀계수의 표준오차를 이용하여 구한 95% 신뢰수준 에서의 상한과 하한을 나타냄. **, ***는 단축 이전과 이후 불편회귀계수 평균 차이에 대한 t-검정(paired t-test) 결과 각각 5%, 1% 유의수준에서 통계적으로 유의함을 표시. <그림 1>과 마찬가지로 식 (1)의 불편회귀모형을 사용해 1분 단위로 추정함. 단지, 08:50분까지는 간략히 보여주고자 10분 단위 스냅샷을 제시하고, 08:55분부터는 단축 이전과 이후의 회귀계수가 급격히 수렴하는 모습을 비교해 보여주고자 1분단위로 제시. 전 시간대 1분 단위 회귀계수는 <부록 표 1>을 참고하기 바람.

사건 이전에는 여러 군데에서 소폭의 계수 반전이 발생했지만 예상체결가격 불편회귀계수 값은 사건 여부와 상관없이 체결 시점에 이를수록 가파르게 계속 상승하며 개장 시점(09:00+)에 1로 수렴한다. 구체적으로 살펴보면, 단축 이후 호가접수시간 초반 계수 값은 단축 이전 0.1361 (08:11)에서 0.1811(08:41)로 소폭 증가한다. 단축 이전 이 정도 가격발견 수준에 도달하려면 08:28은 되어야 가능한 수준이다. 호가접수시간 초반 가격발견이 단축 이후 보다 더 효과적으로 응집해 나타남을 시사한다. 단축 이후 가격발견 효과가 단축 이전 수준과 통계적으로 차이가 나지 않게 되는 시점은 08:55부터이다. 물론 이때도 단축 이전(0.4882)이 이후(0.4500)보다 효과가 크지만 통계적 유의성은 사라진다. 이런 상황은 08:58부터 달라져 08:59에는 단축 이후 가격발견 효과가 오히려 통계적으로 유의하게 더 크다. 또한 개장 시점 직전인 9:00에는 이전 이후 계수 값 평균에 차이가 없고 0.96~0.97일만큼 매우 높으며 30초 내(9:00:30 내) 임의종료 시간에도 계수 값 0.03~0.04에 해당하는 가격발견 효과가 추가로 나타난다.

한편, 학습과정가설에 따라 시간이 지남에 따라 불편회귀계수가 꾸준하게 1로 수렴해 나아가는지를 보고자 계수가 이전 시간대 보다 작아지는 반전현상을 관찰하였다. 단축 이전에는 49개 1분 단위 시간대 중 14개 시간대(29%)에서 직전 시간대 계수보다 작아지는 현상이 나타났으나, 단축 이후에는 19개 시간대 중 단 한 개 시간대에서도 반전현상은 나타나지 않았다.

이상을 종합하면, 시가 단일가매매 호가접수시간을 1시간에서 30분으로 단축했어도 소요시간 대비 가격발견 효과는 최소 약해지지 않았고 오히려 더 매끄러운 가격발견 과정을 보였다. 시간을 단축했음에도 유가증권시장 시가 단일가매매에서 학습과정가설은 강건하게 지지받았다.

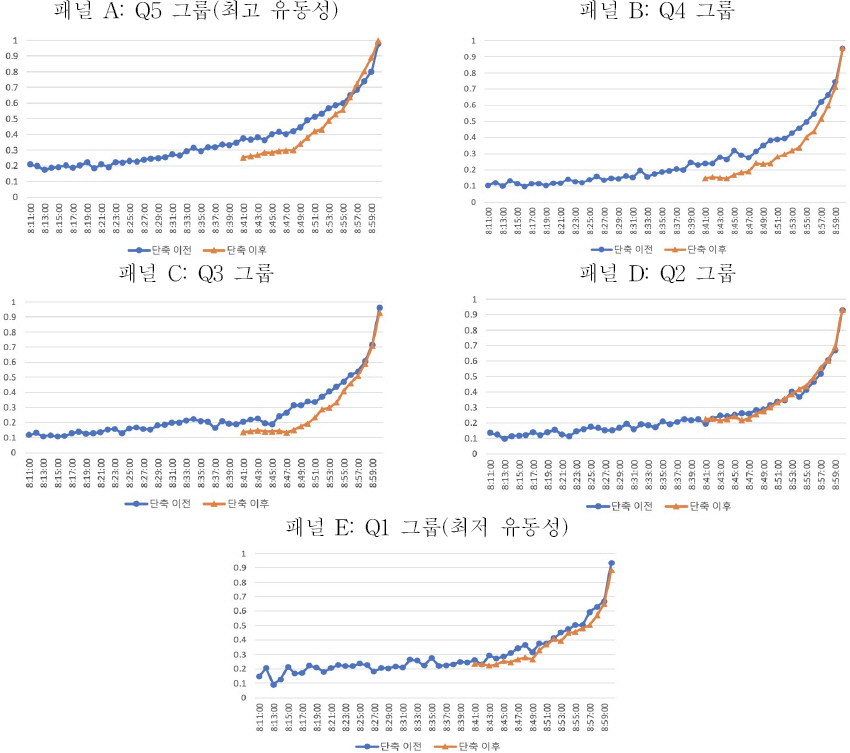

5.1.2 유동성 수준별 분석 결과

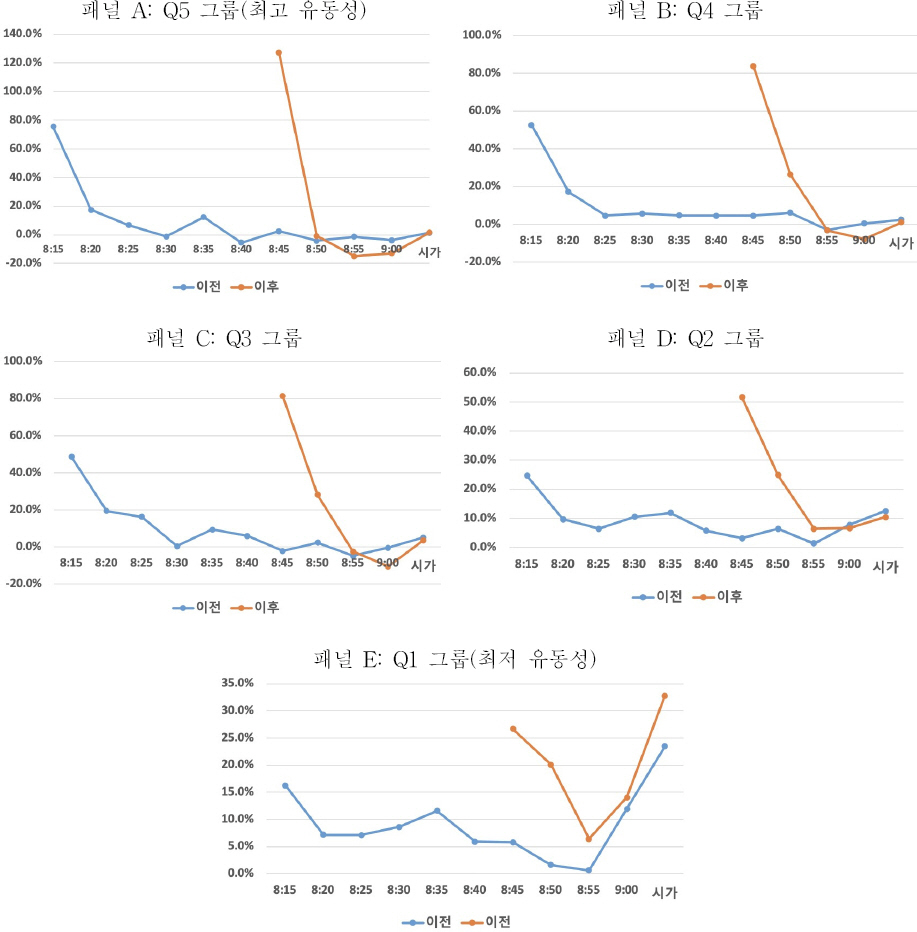

시가 단일가매매시간 단축 사건이 유가증권시장 상장 주식 전체에 골고루 영향을 미쳤는지 살펴보고자 상장 주식을 유동성 수준(단축 이전과 이후 전체 분석 기간 중 평균거래량)에 따라 5개 그룹으로 나누어 효과를 분석하였다. 그 결과, 유동성 그룹별 가격발견 효과는 ‘전반적으로’ 시장 전체 분석에서와 비슷한 특징을 보이나, 유동성이 가장 낮은 그룹의 가격발견에서는 상대적으로 덜 효과적이었다(<표 6>, <그림 2> 참조).

<표 6>

유동성 수준별 불편회귀계수 반전 횟수와 비율

유동성 그룹은 단축 이전과 이후 전체 분석 기간 중 평균 거래량을 5분위로 구분한 것임. Q5가 유동성이 가장 높은 그룹이며 차례로 내려와 Q1이 유동성이 가장 낮은 그룹임. 관측 시점 불편회귀계수 추정치가 직전 시점 회귀계수 추정치보다 작아지는 경우를 계수 반전이라 정의. 반전 비율은 전체 관측치(단축 이전: 49개, 단축 이후: 19개) 중 계수 반전 횟수 비율임.

| 유동성 그룹 | 단축 이전 | 단축 이후 | |||

|---|---|---|---|---|---|

|

|

|

||||

| 반전 횟수 | 반전 비율 | 반전 횟수 | 반전 비율 | 비율 변화 | |

| Q5(최고) | 14 | 28.6% | 1 | 5.3% | -23.3%p |

| Q4 | 17 | 34.7% | 3 | 15.8% | -18.9%p |

| Q3 | 16 | 32.7% | 3 | 15.8% | -16.9%p |

| Q2 | 17 | 34.7% | 2 | 10.5% | -24.2%p |

| Q1(최저) | 18 | 36.7% | 4 | 21.1% | -15.6%p |

구체적으로, 유동성이 제일 높은 그룹(Q5)의 불편회귀계수 값은 시장 전체 분석에서보다 1분(08:57) 일찍 더 크게 나타나고, 유동성이 두 번째로 높은 그룹(Q4)과 두 번째로 낮은 그룹(Q2)은 각각 09:00와 08:59에 이전 대비 역전 현상이 일어나지만, 나머지 그룹에서는 시장 전체 분석에서와는 달리 이러한 역전 현상이 일어나지는 않았다. 특히, 유동성이 제일 낮은 그룹(Q1)은 사건 이후 가격발견 효과가 사건 이전보다 더 늦고 계수 값은 0.9에 미치지 못할 정도로 낮았다. 가격 반전 횟수와 비율도 사건 이후 상당 폭 감소했지만 역시 그룹 Q1에서 반전현상이 여전히 제일 컸다.

5.2 시가 단일가매매 예상체결가격의 가격발견 속도 변화

5.2.1 시장 전체 분석 결과

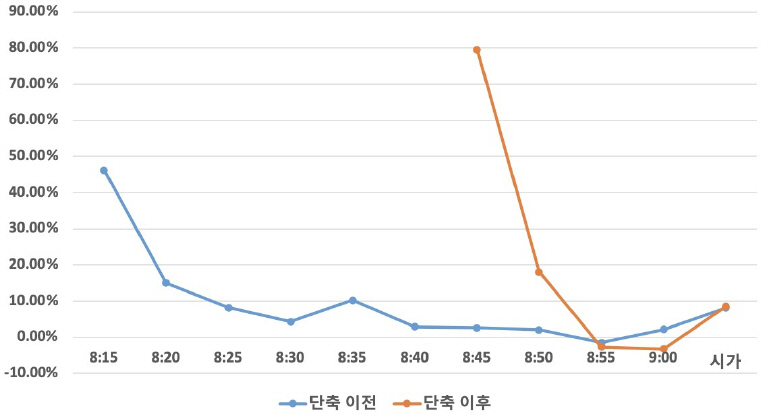

유가증권시장 접속매매시간에서 WPC는 장 초반 가장 높고 12:00~13:00까지 계속 감소하다가 장 후반에 소폭 상승하는 역J자 패턴을 보인다고 알려져 있다(Eom et al., 2010).25) 시장 전체 분석 결과(<그림 3> 참조), 실거래가 이루어지지 않는 시가 단일가매매 동안에도 예상체결가격의 시간대별 WPC는 이와 비슷한 특징을 보인다. 구체적으로, 단축 사건 이전에는 기존 접속매매시간 분석 결과와 비슷한 완만하고 들쑥날쑥한 패턴을 띠지만, 사건 이후에는 이보다는 훨씬 더 강하고 확실한 역J자 패턴을 보였다. 예를 들어, 호가접수시간 개시 후 15분 동안 단축 이전 WPC는 46.2%(08:15)였으나, 이후 WPC는 무려 79.5%(08:45)로 크게 뛰었다. 이는 단축 이전 08:33분에 해당하는 수치로(<그림 4> 참조), 단축 이후 호가접수시간 초반 가격공헌도가 훨씬 더 지배적이고 공격적으로 변해 시가 단일가매매시간 초반 가격발견 속도가 크게 향상됐음을 시사한다.

단축 사건 이후 시가 단일가매매에서는 기존 접속매매시간 연구에서는 볼 수 없던 역J자 패턴의 특이 사항이 하나 나타났다. 이는 호가접수시간 초반에 나타났던 가격발견 속도의 급격한 개선과 관계가 있다. 단축 사건 이전에는 가격공헌이 08:55에 -1.53%로 잠깐 소폭 마이너스를 보였으나, 단축 사건 이후에는 08:55부터 이후 09:00까지 계속 나타나 누적하여 -6.05%로 마이너스 가격공헌이 크게 증가하였다.26) 이는 단축 이후 호가접수시간 초반부 가격발견 속도가 크게 향상되기는 했지만, 그 속도가 너무 빨라 과잉 반응한 부분이 막판 5분여간 조정을 거쳐 균형가격을 찾아갔음을 의미한다.

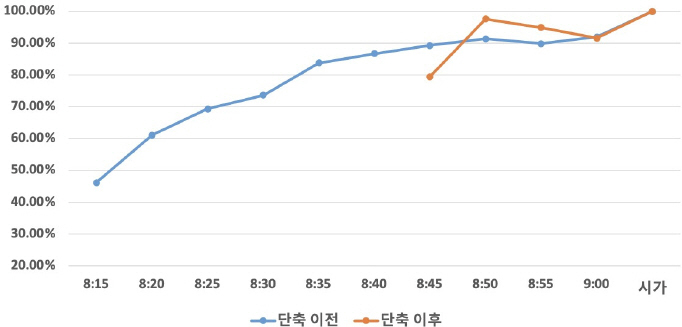

CWPC(누적가중가격공헌도)를 보면(<그림 4> 참조), 단축 이전에는 호가접수 개시 33분 정도 지나야 가격발견의 80% 수준에 도달하고 이후 9:00 정각 92% 선까지 완만한 속도로 역전 없이 가격발견이 이루어졌다. 이에 비해, 단축 이후에는 호가접수 개시 15분(08:45)만 지나도 가격발견의 79.5%에 도달하고 5분 더 지나면(8:50) CWPC가 97.6%까지 치솟았다. 08:55 이후부터는 WPC가 음(-)으로 돌아서(<그림 3> 참조) CPWC가 감소하다가 임의종료 직전에 100%로 반등하였다.

WPC 결과에 근거해 바로 위에서는 이를 가격발견이 호가접수시간 초반에 과도하게 빨라 후반에 조정을 거쳐 균형가격을 발견해 가는 현상으로 해석하였다. 여기에 시중 풍문에 기대어 추가 해석을 해보면, 아마도 외국인투자자, 기관투자자 등 정보거래자(informed traders)가 호가접수시간 막바지에 호가를 적극적으로 조정(정정, 취소 호가 제출)하는 바람에 상대적으로 큰 이들 영향력이 가격에 반영되며 가격발견에 조정이 발생한다고 추정해볼 수 있다.27)

5.2.2 유동성 수준별 분석 결과

유동성 그룹별 WPC 분석 결과, 단축 이전이나 이후 모두 유동성이 제일 낮은 그룹(Q1)을 제외하고는 단축 이후에도 WPC 특징은 ‘전반적으로’ 유지되었다(<그림 5> 참조). 단지 단축 이후 역J자 WPC 패턴을 보이는 유동성 그룹(Q5~Q2) 중에서도 유동성이 제일 높은 그룹에서 중간 그룹(Q5~Q3)까지는 호가접수시간 막바지에 마이너스 가격공헌이 더 심화되어 시장 전체 분석에서와 마찬가지 특징을 보였으나, 유동성이 두 번째로 낮은 Q2에서는 단축 이전과 마찬가지로 마지막까지 마이너스 가격공헌 현상은 일어나지 않았다. Q1은 단축 이전에는 W자 패턴을 단축 이후에는 V자 패턴을 보이며 둘 다 마지막 5+분에 가격발견이 가속하는 양상을 보였다.

요컨대, 단축 이후 유동성 그룹 Q5~Q3에서는 호가접수시간 초반 가격공헌에 오버슈팅이 있다가 막바지에 접어들면서 과잉 반응한 부분에 대한 조정 현상이 벌어졌다. 유동성이 제일 낮은 Q1 그룹에서는 다른 유동성 그룹과는 달리 막바지에 가격발견이 서둘러 이루어지는 듯한 모습을 보였다. 또한 호가접수 초반의 가격발견 속도는 제도 변경 이후 모든 유동성 그룹에서 크게 개선되었다. 이러한 특징은 CWPC 패턴을 통해서도 확인할 수 있다(<그림 6> 참조).

6. 결론

2019년 4월 29일 KRX 유가증권시장은 20여 년 만에 시가 단일가매매시간을 기존 1시간 (08:00~09:00+)에서 30분(08:30~09:00+)으로 단축하였다. 시장환경 변화에 따른 시장 운영 개선, 글로벌 주요 주식시장과의 정합성 등을 고려한 조치였다. 이 논문은 바로 이 호가접수시간 30분 단축이 유가증권시장의 가격발견을 개선하는 데 유용했는지를 분석 규명한다. 사건 전후 50 거래일 예상체결가격을 각각의 분석 기간으로 삼았고, 불편회귀분석으로는 가격발견 효과를, 가중가격공헌도(WPC)로는 가격발견 속도를 비교 분석하였다.

그 결과 첫째, 사건 이전 이후 둘 다 예상체결가격 불편회귀계수 값은 체결 시점에 이를수록 가파르게 계속 1로 상승 수렴하며, 학습과정가설을 시간 단축 여부와 상관없이 강건하게 지지하였다. 사건 이후 시가 단일가매매 가격발견 효과도 사건 이전 후반 30분과 최소한 같아, 단축 조치로 시장 운영 효율성이 ‘일정 수준’ 개선되었다. 둘째, 사건 이전 이후 예상체결가격 WPC는 두 기간 모두 기존 정규거래시간대 일중 패턴과 유사하게 역J자 패턴을 보였다. 그렇지만 역J자 패턴 기울기는 사건 이후에 훨씬 더 가팔랐다. 이는 30분 시간 단축이 초반부 가격발견 속도를 엄청나게 향상시켰지만, 다른 한편으로 후반부 막판 5분여간은 이러한 초반의 과잉반응을 조정해서 균형가격을 찾아가는 과정이 필요했음을 보여준다. 셋째, 유동성 수준별 분석 결과, 대부분 시장 전체 분석 결과와 비슷한 특징을 보였으나, 30분 시간 단축이 유동성이 제일 낮은 그룹(Q1)의 가격발견 효과와 속도에는 현저하게 덜 효과적이었다.

단축 사건 이후 호가접수시간 초반의 가격발견 속도가 지나쳐 후반부에 마이너스 가격공헌이 심화되는 현상은 호가접수시간을 30분 단축하여 정보반영 시간이 부족해진 것인지, 아니면 다른 요인이 있는지 이 시간대 동안 가격발견 결정요인을 다각도로 분석해보면 실마리를 찾을 수도 있다고 본다. 이 경우 투자자유형별 자료를 동원해 함께 분석해야 하는데 데이터 구득 문제로 이 논문에서는 해낼 수 없었다. 또한 방법론으로 사용한 불편회귀분석은 가격발견 결정 두 요소(새로 획득한 정보반영과 기존 정보반영 효율성)를 구분하지 못하는 한계가 있다. 뜻 있는 학자의 관련 후속 연구를 기대해본다.