1.ŌĆģņä£ļĪĀ

Ē¢ēļÅÖņ×¼ļ¼┤ĒĢÖ(behavioral finance)ņØ┤ ļ░£ņĀäĒĢ©ņŚÉ ļö░ļØ╝ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀ(overconfidence)ņØ┤ ņŻ╝ņŗØ ņŗ£ņןĻ│╝ ĻĖ░ņŚģņØś ņØśņé¼Ļ▓░ņĀĢņŚÉ ļīĆĒĢ£ ļäōņØĆ ļ▓öņ£äņØś ĒśäņāüņØä ņäżļ¬ģĒĢĀ ņłś ņ׳ļŗżļŖö ņŚ░ĻĄ¼Ļ░Ć ļō▒ņןĒĢśĻĖ░ ņŗ£ņ×æĒ¢łļŗż. Chen et al.(2007)ņØĆ ņŗĀĒØźņŗ£ņןņŚÉņä£ ņżæĻĄŁ Ēł¼ņ×Éņ×ÉļōżņØ┤ ļööņŖżĒżņ¦Ćņģś ĒÜ©Ļ│╝, Ļ│╝ņŗĀ, ĻĘĖļ”¼Ļ│Ā ļīĆĒæ£ņä▒ ĒÄĖĒ¢źņ£╝ļĪ£ ņØĖĒĢ┤ ļ╣äĒĢ®ļ”¼ņĀüņØĖ ņØśņé¼Ļ▓░ņĀĢņØä ĒĢśĻ│Ā Ļ▓░Ļ│╝ņĀüņ£╝ļĪ£ ļé«ņØĆ Ēł¼ņ×Éņä▒Ļ│╝ļź╝ Ļ░Ćņ¦äļŗżĻ│Ā ņŻ╝ņןĒĢ£ļŗż. Statman et al.(2006)ņØĆ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ ĒÄĖĒ¢źļÉ£ ņ×ÉĻĖ░ĻĘĆņØĖ(biased self-attribution)ņ£╝ļĪ£ ņØĖĒĢ┤ Ļ▒░ļלļ¤ēņØ┤ ņ”ØĻ░ĆĒĢśļŖö ĒśäņāüņØä ĒÖĢņØĖĒĢśĻ│Ā, Ļ▒░ļלļ¤ēĒÜīņĀäņ£©Ļ│╝ ņłśņØĄļźĀĻ░äņØś ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ┤ĆĻ│äļź╝ ļ░£Ļ▓¼ĒĢ£ļŗż. Daniel et al.(1998)ņØĆ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ ĒÄĖĒ¢źļÉ£ ņ×ÉĻĖ░ĻĘĆņØĖņØ┤ ņŻ╝ņŗØņŗ£ņןņØś Ļ│╝ņåīļ░śņØæ(underreaction)Ļ│╝ Ļ│╝ņ×ēļ░śņØæ(overreaction)ņØä ņäżļ¬ģĒĢĀ ņłś ņ׳ļŗżĻ│Ā ņŻ╝ņןĒĢ£ļŗż. Daniel et al.(1998)ņØś ļ¬©ĒśĢņŚÉ ļö░ļź┤ļ®┤, Ēł¼ņ×Éņ×ÉļŖö ņŖżņŖżļĪ£ņØś ļŖźļĀźņØä Ļ│╝ņŗĀĒĢśņŚ¼ ĻĘĖļōżņØś ņé¼ņĀüņØĖ ņĀĢļ│┤(private information)ņŚÉ ļīĆĒĢśņŚ¼ Ļ│╝ņ×ēļ░śņØæĒĢ£ļŗż. Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀņØĆ ĻĘĖļōżņØś ņ¢æņØś(ņØīņØś) ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ ņČöĻ░ĆņĀüņØĖ Ļ│╝ņ×ēļ░śņØæņØä ņĢ╝ĻĖ░ĒĢśļ»ĆļĪ£ Ļ│╝Ļ▒░ņłśņØĄļźĀņØĆ ļ»ĖļלņłśņØĄļźĀņØä ņśłņĖĪĒĢśĻ▓ī ļÉ£ļŗż. ņØ┤ņ▓śļ¤╝, Ļ│äņåŹņĀüņØĖ Ļ│╝ņ×ēļ░śņØæ(continuing overreaction, CO)ņØĆ Ēł¼ņ×Éņ×ÉĻ░Ć ņ×ÉņŗĀņØś ļŖźļĀźņØä Ļ│╝ņŗĀĒĢśņŚ¼ ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ Ļ│╝ņ×ēļ░śņØæĒĢśĻ│Ā ņ░©Ēøä ļ░£ņāØļÉśļŖö Ļ│ĄņĀüņØĖ ņŗĀĒśĖ(public signals)Ļ░Ć ĻĘĖļōżņØś Ļ│╝ņŗĀņØä ļŹöņÜ▒ ņ”ØĻ░Ćņŗ£ņ╝£, Ļ▓░Ļ│╝ņĀüņ£╝ļĪ£ ĻĘĖļōżņØś ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ ļŹö ļåÆņØĆ Ļ│╝ņ×ēļ░śņØæņØä ņĢ╝ĻĖ░ĒĢśļŖö Ļ▓āņØä ņØśļ»ĖĒĢ£ļŗż. ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ Ēł¼ņ×Éņ×ÉņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØ┤ ļŗ©ĻĖ░ņĀüņ£╝ļĪ£ ļ¬©ļ®śĒģĆ ĒśäņāüņØä ļ░£ņāØņŗ£Ēé©ļŗżļ®┤, ņØ┤ļŖö Ļ│╝Ļ▒░ņłśņØĄļźĀļ│┤ļŗż ļ»ĖļלņłśņØĄļźĀņØä ņל ņśłņĖĪĒĢĀ ņłś ņ׳ņØä Ļ▓āņØ┤ļŗż. Byun et al.(2016)ņØĆ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņŚÉ ļīĆĒĢ£ ņĖĪņĀĢņ╣śļź╝ ĻĄ¼ņä▒ĒĢśņŚ¼ Daniel et al.(1998)ņŚÉ ļīĆĒĢ£ ņŗżņ”ØņĀü ņ”ØĻ▒░ļź╝ ņĀ£Ļ│ĄĒĢ£ļŗż. ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś ņĖĪņĀĢņ╣śļź╝ ņØ┤ņÜ®ĒĢśņŚ¼ ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØ┤ Ļ│╝Ļ▒░ņłśņØĄļźĀļ│┤ļŗż ļ»ĖļלņłśņØĄļźĀņØä ļŹö ņל ņśłņĖĪĒĢśĻ│Ā, Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņ£╝ļĪ£ ņØĖĒĢ┤ ļ¬©ļ®śĒģĆ ĒÜ©Ļ│╝Ļ░Ć ņĢĮĒÖöļÉ©ņØä ļ│┤ņØĖļŗż.

ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ļéśĒāĆļé┤ļŖö COļ│Ćņłśļź╝ ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉ ļÅäņ×ģĒĢśņŚ¼ ļ»ĖļלņłśņØĄļźĀņØä ņśłņĖĪĒĢśļŖöņ¦Ć ņŚ¼ļČĆļź╝ Ļ▓ĆĒåĀĒĢ£ļŗż. COļ│ĆņłśļŖö ņøöļ│äĻ▒░ļלļīĆĻĖłĻ│╝ ļČĆĒśĖĒÖöļÉ£ ļÅÖņŗ£Ļ░äļīĆ ņłśņØĄļźĀļĪ£ ĻĄ¼ņä▒ĒĢśļ®░ Ļ│╝Ļ▒░ 12Ļ░£ņøö ļÅÖņĢł Ļ░Ćņżæņ╣śĻ░Ć ņĀüņÜ®ļÉ£ ņøöļ│ä ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ē(signed volume)ņØś ĒĢ®Ļ│äļĪ£ ļÅäņČ£ļÉ£ļŗż. Benos(1998)ņÖĆ Odean(1998)ņØĆ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀņØ┤ Ļ▒░ļלļ¤ēņØä ņ”ØĻ░Ćņŗ£ĒéżļŖö ĒśäņāüņØä ņĀ£ņŗ£ĒĢśņŚ¼ Ļ▒░ļלļ¤ēņØ┤ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ Ļ│╝ņ×ēļ░śņØæņØś ļīĆņÜ®ņ╣śļĪ£ ņé¼ņÜ®ļÉĀ ņłś ņ׳ļŗżĻ│Ā ņŻ╝ņןĒĢ£ļŗż. ņÜ░ļ”¼ļŖö COļ│ĆņłśĻ░Ć ļ»Ėļל ņłśņØĄļźĀņŚÉ ļīĆĒĢ£ ņśłņĖĪļĀźņØä Ļ░Ćņ¦ĆļŖöņ¦Ć ĒÅēĻ░ĆĒĢ£ļŗż. ļ©╝ņĀĆ, COļ│ĆņłśļĪ£ 10ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢśĻ│Ā, COĻ░Ć Ļ░Ćņן ļåÆņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļ¦żņ×ģĒĢśĻ│Ā Ļ░Ćņן ļé«ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļ¦żļÅäĒĢśļŖö COņĀäļץņØä ĻĄ¼ņä▒ĒĢ£ļŗż. ļ¦īņĢĮ, COļ│ĆņłśĻ░Ć ļ»Ėļל ņłśņØĄļźĀņŚÉ ņ£ĀņØśĒĢ£ ņśłņĖĪļĀźņØä Ļ░Ćņ¦äļŗżļ®┤, 6Ļ░£ņøöņŚÉņä£ 12Ļ░£ņøöĻ░äņØś ļ│┤ņ£ĀĻĖ░Ļ░äļÅÖņĢł ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ł Ļ▓āņØ┤ļŗż.

ņÜ░ļ”¼ļŖö ĻĖ░ņĪ┤ņØś ņŚ░ĻĄ¼ņŚÉņä£ COņÖĆ ļ¬©ļ®śĒģĆĻ│╝ņØś Ļ┤ĆĻ│äņŚÉ ņ¦æņżæĒĢ£ Ļ▓āņØä ļ░£ņĀäņŗ£ņ╝£, ĒåĄņĀ£ļ│ĆņłśņØś ņśüĒ¢źņØä ĒÖĢņØĖĒĢ£ļŗż. ĒåĄņĀ£ļ│Ćņłśļź╝ ĒżĒĢ©ĒĢśļŖö Ļ▓āņØĆ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØ┤ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ņśüĒ¢źņØä ļ»Ėņ╣£ļŗżļŖö ĒāĆļŗ╣ņä▒ņØä ļåÆņØĖļŗż. ņäĀĒ¢ēņŚ░ĻĄ¼ņŚÉ ļö░ļź┤ļ®┤ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØĆ ļ¬©ļ®śĒģĆĒśäņāüņŚÉ ĒĢĄņŗ¼ņÜöņØĖņ£╝ļĪ£ ņ×æņÜ®ĒĢ£ļŗż. ļ©╝ņĀĆ, ņÜ░ļ”¼ļŖö ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØä ĒåĄĒĢ┤ COņĀäļץĻ│╝ ļ¬©ļ®śĒģĆņĀäļץņØś ņłśņØĄņä▒ņØä ļ╣äĻĄÉļČäņäØĒĢ£ļŗż. ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņן ņŚÉņä£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś ļ¬©ļ®śĒģĆ ņĪ░ņĀĢņłśņØĄļźĀņØĆ COņÖĆ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ┤ĆĻ│äņŚÉ ņ׳ļŗżļŖö Ļ▓āņØä ĒÖĢņØĖĒĢśļŖö ļ░śļ®┤, ļ¬©ļ®śĒģĆ ņłśņØĄļźĀņØĆ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņŚÉ ņØśĒĢ┤ ļČĆļČäņĀüņ£╝ļĪ£ ĒåĄņĀ£ļÉ©ņØä ĒÖĢņØĖĒĢ£ļŗż. ļæśņ¦Ė, COĻ░Ć ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņŚÉ ņØśĒĢ┤ ĒåĄņĀ£ ļÉśļŖöņ¦Ć ņŚ¼ļČĆļź╝ ĒÖĢņØĖĒĢśĻĖ░ ņ£äĒĢ┤ ļŗżļ│Ćļ¤ē ļČäņäØņØä ņ¦äĒ¢ēĒĢ£ļŗż. ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØĆ ĻĖ░ņĪ┤ņØś ņŚ░ĻĄ¼ļōżņŚÉ ņØśĒĢ┤ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ņ£ĀņØśĒĢ£ ņśüĒ¢źņØä ņżĆļŗżĻ│Ā ļéśĒāĆļé£ ņŗ£ņןļ▓ĀĒāĆ(BETA), ĻĖ░ņŚģĻĘ£ļ¬©(SIZE), ņןļČĆĻ░Ćņ╣ś ļīĆ ņŗ£ņןĻ░Ćņ╣ś(BEME), Ļ│╝Ļ▒░ņłśņØĄļźĀ(PRET), ļŗ©ĻĖ░ņłśņØĄļźĀļ░śņĀä(REV), ņ£ĀļÅÖņä▒(ILLIQ), Ļ│Āņ£Āļ│ĆļÅÖņä▒(IVOL)ņØ┤ļ®░, ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ ņé¼ņÜ®ĒĢśļŖö COļŖö Ļ▒░ļלļ¤ēņØä ĻĖ░ļ░śņ£╝ļĪ£ ļÅäņČ£ļÉśĻĖ░ ļĢīļ¼ĖņŚÉ Ļ▒░ļלļ¤ēĒÜīņĀäņ£©(TURN)ņØä ņČöĻ░ĆņĀüņ£╝ļĪ£ Ļ│ĀļĀżĒĢ£ļŗż. ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖļōżņØä ĒåĄņĀ£ĒĢ£ Ļ▓ĮņÜ░ņŚÉ CO ņĀäļץņØś ņłśņØĄņä▒ņØĆ ņŚ¼ņĀäĒ׳ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļ®░, ņØ┤ļŖö COņĀäļץņØ┤ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ Ļ░Ćņ¦ĆļŖö ņśłņĖĪļĀźņØĆ ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņŚÉ ņØśņĪ┤ĒĢ£ Ļ▓āņØ┤ ņĢäļŗśņØä ļéśĒāĆļéĖļŗż. ņģŗņ¦Ė, Grinblatt and Moskowitz(2004)ņÖĆ Da et al.(2014)ņØĆ ņłśņØĄļźĀ ņ¦ĆņåŹņä▒(return consistency)Ļ│╝ ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒(information discreteness)ņØ┤ Ļ│╝Ļ▒░ņłśņØĄļźĀĻ│╝ ņŻ╝ņŗØņłśņØĄļźĀĻ░äņØś Ļ┤ĆĻ│äņŚÉ ņśüĒ¢źņØä ļ»Ėņ╣śļŖöņ¦Ć ĒÖĢņØĖĒĢ£ļŗż. Grinblatt and Moskowitz(2004)ļŖö Ļ│╝Ļ▒░ņłśņØĄļźĀņØ┤ ņ¢æņØś Ļ░Æņ£╝ļĪ£ ņ¦ĆņåŹļÉ£ļŗżļ®┤ ĻĖ░ļīĆņłśņØĄļźĀņØĆ Ļ│╝Ļ▒░ņłśņØĄļźĀņØś ņ¦ĆņåŹņä▒ņŚÉ ņ£ĀņØśĒĢ£ ņśüĒ¢źņØä ļ░øļŖöļŗżĻ│Ā ļéśĒāĆļéĖļŗż. Da et al.(2014)ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äļÅÖņĢł ņĀĢļ│┤ņØś ĒØÉļ”äņØ┤ ņŚ░ņåŹņĀüņØĖņ¦Ć ņŚ¼ļČĆļź╝ ĒÖĢņØĖĒĢśļŖö ņĖĪņĀĢņ╣śļĪ£ ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒(information discreteness, ID)ņØä ņĀ£ņŗ£ĒĢśĻ│Ā, ņŚ░ņåŹņĀüņØĖ ņĀĢļ│┤ļŖö ļŹö Ļ░ĢĒĢ£ ņłśņØĄļźĀņØś ņ¦ĆņåŹņØä ņ£ĀļÅäĒĢ£ļŗżĻ│Ā ļéśĒāĆļéĖļŗż. ļö░ļØ╝ņä£ ļÅÖņØ╝ĒĢ£ ļ░®Ē¢źņØś ņłśņØĄļźĀ ņŗ£Ļ│äņŚ┤ņØä Ļ░Ćņ¦ä ņŻ╝ņŗØņØĆ ĻĘ╣ļŗ©ņĀüņØĖ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ĒżĒĢ©ļÉĀ Ļ▓ĮĒ¢źņØ┤ ņ׳Ļ│Ā, ņØ┤ļ¤¼ĒĢ£ ņŻ╝ņŗØņØĆ ļåÆņØĆ ņłśņżĆņØś ņłśņØĄļźĀ ņ¦ĆņåŹņä▒Ļ│╝ ļé«ņØĆ ņłśņżĆņØś ņĀĢļ│┤ ļČłņŚ░ņåŹņä▒ņØä Ļ░Ćņ¦ł Ļ░ĆļŖźņä▒ņØ┤ ņ׳ļŗż. ņÜ░ļ”¼ļŖö ĒżĒŖĖĒÅ┤ļ”¼ņśż ļČäņäØņØä ĒåĄĒĢśņŚ¼ COņĀäļץņØ┤ ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ņØś ĒÜ©Ļ│╝ņŚÉ ĻĖ░ņØĖĒĢśļŖöņ¦Ć ņŚ¼ļČĆļź╝ ĒÖĢņØĖĒĢ£ļŗż. ļŹö ļéśņĢäĻ░Ć, Fama and MacBeth(1973)ņØś ĒÜĪļŗ©ļ®┤ ĒÜīĻĘĆļČäņäØņØä ņØ┤ņÜ®ĒĢśņŚ¼ ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖĻ│╝ Ē¢ēĒā£ņĀü ņÜöņØĖņØä ļÅÖņŗ£ņŚÉ ĒåĄņĀ£ĒĢ£ ĒøäņŚÉļÅä COņĀäļץņØ┤ ĒÜĪļŗ©ļ®┤ņĀüņ£╝ļĪ£ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ņ£ĀņØśĒĢ£ ņśłņĖĪļĀźņØä Ļ░Ćņ¦ĆļŖöņ¦Ć ĒÖĢņØĖ ĒĢ£ļŗż. ļäĘņ¦Ė, Grinblatt and Han(2005)ņŚÉ ļö░ļź┤ļ®┤ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØś ļīĆņÜ®ļ│ĆņłśĻ░Ć ļ¬©ļ®śĒģĆņĀäļץņØś ņłśņØĄņä▒ņØä ņ░ĮņČ£ĒĢśļŖö ĒĢĄņŗ¼ļ│ĆņłśņØ┤ļ»ĆļĪ£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄ ļ│Ćņłśļź╝ ĒåĄņĀ£ĒĢ£ Ļ▓ĮņÜ░ņŚÉļŖö Ļ│╝Ļ▒░ņłśņØĄļźĀņØ┤ ĒÜĪļŗ©ļ®┤ņĀüņ£╝ļĪ£ ņłśņØĄļźĀņØä ņśłņĖĪĒĢśņ¦Ć ļ¬╗ĒĢ£ļŗż. ņÜ░ļ”¼ļŖö ļ¬©ļ®śĒģĆņĀäļץņØś ĒĢĄņŗ¼ļ│ĆņłśļĪ£ ļéśĒāĆļé£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄĻ│╝ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś ļÅÖņŗ£Ļ░äļīĆ ņśüĒ¢źņØä ĒÖĢņØĖĒĢ£ļŗż. ļŗżļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśż ļČäņäØņØä ĒåĄĒĢśņŚ¼ ļæÉ ļ│Ćņłś ņżæ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆĒĢ┤ ļŹö Ļ░ĢĒĢ£ ņśłņĖĪļĀźņØä Ļ░Ćņ¦ĆļŖö ļ│Ćņłśļź╝ ĒÖĢņØĖĒĢśĻ│Ā, ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ļéśĒāĆļéśļŖö ļ╣äļīĆņ╣ŁņĀü ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä Ļ│ĀļĀżĒĢśņŚ¼ COņĀäļץņØś ņłśņØĄņä▒ņØä ĒÖĢņØĖĒĢ£ļŗż. ļŗżņä»ņ¦Ė, Blitz et al.(2011)ņŚÉņä£ ņĀ£ņŗ£ĒĢ£ ņ×öņŚ¼ļ¬©ļ®śĒģĆ(residual momentum)ņŚÉ ļö░ļØ╝ ņ×öņŚ¼ņłśņØĄļźĀņØä ņØ┤ņÜ®ĒĢ£ ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ļÅäņČ£ĒĢ£ļŗż. ņ×öņŚ¼ļ¬©ļ®śĒģĆ ņĀäļץņØ┤ ĻĖ░ņĪ┤ņØś ļ¬©ļ®śĒģĆ ņĀäļץļ│┤ļŗż 2ļ░░Ļ░Ćļ¤ē ļåÆņØĆ ņłśņØĄļźĀĻ│╝ ņ¦ĆņåŹņä▒ņØä Ļ░Ćņ¦äļŗżļŖö ņäĀĒ¢ēņŚ░ĻĄ¼ņÖĆļŖö ļŗ¼ļ”¼, ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ ņĀäļץņØĆ ĻĖ░ņĪ┤ņØś ņłśņØĄļźĀ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņŚÉ ļ╣äĒĢśņŚ¼ ļé«ņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ĻĘĖļ¤╝ņŚÉļÅä ļČłĻĄ¼ĒĢśĻ│Ā, ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØĆ ņŻ╝ņŗØ ņłśņØĄļźĀņŚÉ ļīĆĒĢ┤ ņ£ĀņØśĒĢ£ ņ¢æņØś ņśłņĖĪļĀźņØä Ļ░Ćņ¦Ćļ®░ ņ×öņŚ¼ļ¬©ļ®śĒģĆņŚÉ ņØśĒĢ┤ ĒåĄņĀ£ļÉśņ¦Ć ņĢŖļŖöļŗż.

ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢśļŖö Ļ│╝Ļ▒░ ĻĖ░Ļ░äĻ│╝ ņŗ£ņןņāüĒā£, ņŗ£ņןļÅÖĒā£ņŚÉ ļö░ļźĖ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ĒÖĢņØĖĒĢśņŚ¼ COņĀäļץņØś ņłśņØĄņä▒ņØä ņ×¼ņĀÉĻ▓ĆĒĢ£ļŗż. ļ©╝ņĀĆ, ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äņØä Ļ│╝Ļ▒░ 6Ļ░£ņøö, 9Ļ░£ņøö, 18Ļ░£ņøöĻ│╝ 24Ļ░£ņøöļĪ£ ļ│ĆĻ▓ĮĒĢśņŚ¼ļÅä ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆĒĢ£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś ņ¢æņØś ņśüĒ¢źņØĆ ņ¦ĆņåŹļÉśļŖö Ļ▓āņØä ĒÖĢņØĖĒĢ£ļŗż. ļśÉĒĢ£, ļŗ©ĻĖ░ ļ¬©ļ®śĒģĆ ņłśņØĄļźĀņØ┤ ņŗ£ņןņāüĒā£ņÖĆ ņŗ£ņןļÅÖĒā£ņŚÉ ļö░ļØ╝ Ļ▓░ņĀĢļÉ£ļŗżļŖö Cooper et al.(2004)Ļ│╝ Asem and Tian(2010)ņØś ņŚ░ĻĄ¼ļź╝ ļö░ļØ╝ ņŗ£ņןņāüĒā£ņÖĆ ņŗ£ņןļÅÖĒā£ņŚÉ ļö░ļźĖ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ│╝ ņŻ╝ņŗØ ņłśņØĄļźĀ Ļ░äņØś Ļ┤ĆĻ│äļź╝ ĒÖĢņØĖĒĢ£ļŗż. ņŗ£ņןņāüĒā£ļź╝ ĻĖ░ņżĆņ£╝ļĪ£ ļČäņäØĒĢ£ Ļ▓░Ļ│╝ņŚÉ ļö░ļź┤ļ®┤ ņāüņŖ╣ņŗ£ņןĻ│╝ ĒĢśļØĮņŗ£ņן ņŚÉņä£ COņĀäļץņØĆ ļ¬©ļæÉ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ņāüņŖ╣ņŗ£ņןĻ│╝ ĒĢśļØĮņŗ£ņן Ļ▓░Ļ│╝Ļ░äņØś ņ░©ņØ┤ļź╝ ĒåĄĒĢ┤ ļæÉ ņŗ£ņןņØś ņłśņØĄļźĀ ņ░©ņØ┤Ļ░Ć ņŚåļŗżļŖö Ļ▓āņØä ĒÖĢņØĖĒĢśņŚ¼ COņĀäļץņØĆ ņŗ£ņןņāüĒā£ņŚÉ Ēü░ ņśüĒ¢źņØä ļ░øņ¦Ć ņĢŖņØīņØä ļéśĒāĆļéĖļŗż. ļŹö ļéśņĢäĻ░Ć, ņŗ£ņןļÅÖĒā£ņŚÉ ļö░ļØ╝ COņĀäļץņØä ļČäņäØĒĢ£ļŗż. Ļ│╝Ļ▒░ņŗ£ņןņØ┤ ņāüņŖ╣ņŗ£ņן ņØ┤ļØ╝ļ®┤ ņāüļīĆņĀüņ£╝ļĪ£ ļåÆņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦Ćļ®░, ļÅÖņŗ£Ļ░äļīĆ ņŗ£ņןņØ┤ ņāüņŖ╣ņŗ£ņןņØ╝ ļĢī ĻĘĖļĀćņ¦Ć ņĢŖņØĆ Ļ▓ĮņÜ░ņŚÉ ļ╣äĒĢśņŚ¼ ļŹö ļåÆņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ņóģĒĢ®ĒĢśļ®┤ Ļ│╝Ļ▒░ņŗ£ņןņØ┤ ņāüņŖ╣ņŗ£ņןņØ┤ļ®░ ļÅÖņŗ£Ļ░äļīĆ ņŗ£ņןļÅä ņāüņŖ╣ņŗ£ņן ņ£╝ļĪ£ ņ£Āņ¦ĆļÉĀ Ļ▓ĮņÜ░ņŚÉ COņĀäļץņØś ņłśņØĄņä▒ņØĆ Ļ░Ćņן ļåÆĻ│Ā, ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆĒĢ£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś ņśłņĖĪļĀźņØ┤ Ļ░Ćņן Ļ░ĢĒĢśļŗż.

ļ│Ė ņŚ░ĻĄ¼ļŖö ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ Ēł¼ņ×Éņ×ÉņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØ┤ ņŻ╝ņŗØņłśņØĄļźĀņØ┤ ļ»Ėņ╣śļŖö ĒśäņāüņØä ņĪ░ņé¼ĒĢ£ļŗż. ņøöļ│äĻ▒░ļלļīĆĻĖłĻ│╝ ņøöļ│äņłśņØĄļźĀņØä ĻĖ░ļ░śņ£╝ļĪ£ ļÅäņČ£ļÉ£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś ņĖĪņĀĢņ╣śļŖö ņŻ╝ņŗØ ņłśņØĄļźĀĻ░äņØś ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ┤ĆĻ│äņŚÉ ņ׳ļŗż. ļŗżņŗ£ ļ¦ÉĒĢ┤, ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ Ēł¼ņ×Éņ×ÉļŖö ĻĘĖļōżņØś ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢ┤ Ļ│╝ņ×ēļ░śņØæĒĢ£ļŗż. ļŹö ļéśņĢäĻ░Ć, ļŗżņ¢æĒĢ£ ĒåĄņĀ£ļ│Ćņłśļź╝ ļÅäņ×ģĒĢśņŚ¼ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆĒĢ£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś ņśłņĖĪļĀźņØä ņ×¼ņĀÉĻ▓ĆĒĢ£ļŗż. ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖĻ│╝ Ē¢ēĒā£ņĀü ņÜöņØĖņØä Ļ│ĀļĀżĒĢ£ ĒøäņŚÉļÅä Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ ņĀäļץņØś ņłśņØĄņä▒ņØ┤ ņ£Āņ¦ĆļÉśļ»ĆļĪ£ ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ Ļ▒░ļלļ¤ēņØä ņØ┤ņÜ®ĒĢ£ Ēł¼ņ×ÉņĀäļץņØ┤ ņłśņØĄņä▒ņØä Ļ░Ćņ¦äļŗżļŖö ņé¼ņŗżņØä ĒÖĢņØĖĒĢ£ļŗż. ļ│Ė ņŚ░ĻĄ¼ļŖö Ēł¼ņ×Éņ×ÉņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ│╝ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ņ£ĀņØśĒĢ£ Ļ┤ĆĻ│äļź╝ ĒÖĢņØĖĒĢśņŚ¼ Ļ┤ĆļĀ©ļČäņĢ╝ņØś ņŗ£ņé¼ņĀÉņØä ņĀ£ņŗ£ĒĢ£ļŗż. ļśÉĒĢ£, Ē¢ēļÅÖņ×¼ļ¼┤ĒĢÖ Ļ┤ĆņĀÉņŚÉņä£ Ēł¼ņ×Éņ×ÉņØś ļ╣äĒĢ®ļ”¼ņĀüņØĖ Ē¢ēļÅÖņØä ĒÖĢņØĖ ĒĢ£ļŗżļŖö ņĀÉņŚÉņä£ ĻĖ░ņŚ¼ļź╝ Ļ░Ćņ¦äļŗż.

ļ│Ė ņŚ░ĻĄ¼ļŖö ļŗżņØīĻ│╝ Ļ░ÖņØ┤ ĻĄ¼ņä▒ļÉ£ļŗż. ņĀ£ŌĆģ2ņןņØĆ ņäĀĒ¢ēņŚ░ĻĄ¼ļź╝ ļéśĒāĆļé┤Ļ│Ā, ņĀ£ŌĆģ3ņןņŚÉņä£ļŖö Ļ│äņåŹņĀü Ļ│╝ņ×ē ļ░śņØæĻ│╝ ņŻ╝ņÜö ļ│Ćņłś, ņ×ÉļŻī ļ░Å ļ░®ļ▓ĢļĪĀņŚÉ ļīĆĒĢ┤ ņäżļ¬ģĒĢ£ļŗż. ņĀ£ŌĆģ4ņןņŚÉņä£ļŖö Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ│╝ ņŻ╝ņŗØņłśņØĄļźĀņØś Ļ┤ĆĻ│äļź╝ ĒÖĢņØĖĒĢ£ļŗż. ļ¬©ļ®śĒģĆ, ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖ, ņłśņØĄļźĀ ņ¦ĆņåŹņä▒, ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒, ĻĘĖļ”¼Ļ│Ā ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĒåĄņĀ£ĒĢ£ Ļ▓░Ļ│╝ļź╝ ļéśĒāĆļé┤Ļ│Ā ĻĘĖ ļé┤ņÜ®ņØä ĒĢ┤ņäØĒĢ£ļŗż. ņČöĻ░ĆņĀüņ£╝ļĪ£ ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ│╝ ņŻ╝ņŗØņłśņØĄļźĀĻ░äņØś Ļ┤ĆĻ│äļź╝ ĒÖĢņØĖĒĢ£ļŗż. ņĀ£ŌĆģ5ņןņŚÉņä£ļŖö Ļ░ĢĻ▒┤ņä▒ Ļ▓ĆņĀĢņØä ļéśĒāĆļé┤Ļ│Ā, ņĀ£ŌĆģ6ņןņŚÉņä£ļŖö Ļ▓░ļĪĀņØä ņĀ£ņŗ£ĒĢ£ļŗż.

2.ŌĆģņäĀĒ¢ēņŚ░ĻĄ¼

Daniel et al.(1998)ņŚÉ ļö░ļź┤ļ®┤ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ ĒÄĖĒ¢źļÉ£ ņ×ÉĻĖ░ĻĘĆņØĖņØ┤ ņŻ╝ņŗØņŗ£ņןņØś Ļ│╝ņåīļ░śņØæĻ│╝ Ļ│╝ņ×ēļ░śņØæņØä ņäżļ¬ģĒĢ£ļŗż. Ēł¼ņ×Éņ×ÉļŖö ņŖżņŖżļĪ£ņØś ļŖźļĀźņØä Ļ│╝ņŗĀĒĢśņŚ¼ ĻĘĖļōżņØś ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢśņŚ¼ Ļ│╝ņ×ē ļ░śņØæĒĢ£ļŗż. ņ░©ĒøäņŚÉ ļ░£ņāØĒĢśļŖö Ļ│ĄņĀü ņŗĀĒśĖ(public signal)ļŖö ĻĘĖļōżņØś ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ Ļ│╝ņ×ēļ░śņØæņØä ņ┤ēņ¦äņŗ£Ēé©ļŗż. ņØ┤ņÖĆ Ļ░ÖņØĆ Ļ│╝ņ×ēļ░śņØæņØĆ ĒÄĖĒ¢źļÉ£ ņ×ÉĻĖ░ĻĘĆņØĖņ£╝ļĪ£ ņØ┤ņ¢┤ņĀĖ ņČöĻ░ĆņĀüņØĖ Ļ│╝ņŗĀņØä ņĢ╝ĻĖ░ĒĢ£ļŗż. ļö░ļØ╝ņä£ ļåÆņØĆ(ļé«ņØĆ) Ļ│╝Ļ▒░ņłśņØĄļźĀņØĆ Ēł¼ņ×Éņ×ÉĻ░Ć ĻĘĖļōżņØś ņ¢æņØś(ņØīņØś) ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļŹöņÜ▒ Ļ│╝ņŗĀĒĢśĻ▓ī ĒĢśļ®░ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀņØĆ ņ¢æņØś(ņØīņØś) ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ ņČöĻ░ĆņĀüņØĖ Ļ│╝ņ×ēļ░śņØæņØä ņĢ╝ĻĖ░ĒĢ£ļŗż. ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ Ēł¼ņ×Éņ×ÉņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ(continuing overreaction: CO)ņØĆ ļŗ©ĻĖ░ņĀüņ£╝ļĪ£ ļ¬©ļ®śĒģĆ ĒśäņāüņØä ņĢ╝ĻĖ░ĒĢśļ®░ Ļ│╝Ļ▒░ņłśņØĄļźĀņØĆ ļ»Ėļל ņłśņØĄļźĀņØä ņśłņĖĪĒĢśĻ▓ī ļÉ£ļŗż. Daniel et al.(1998)ņØś Ļ▓░Ļ│╝ņÖĆ Ļ░ÖņØ┤ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØ┤ ļ¬©ļ®śĒģĆ ĒśäņāüņØä ņ£Āļ░£ĒĢ£ļŗżļ®┤, ņØ┤ļŖö Ļ│╝Ļ▒░ņłśņØĄļźĀ ļ│┤ļŗż ļ»ĖļלņłśņØĄļźĀņØä ņל ņśłņĖĪĒĢĀ Ļ▓āņØ┤ļŗż.

ņØ┤ņÖĆ ņ£Āņé¼ĒĢśĻ▓ī ļ¦ÄņØĆ ņŗżņ”ØņŚ░ĻĄ¼ļōżņØĆ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ Ļ▒░ļלļ¤ēņØś Ļ┤ĆĻ│äņŚÉ ļīĆĒĢ£ ņ”ØĻ▒░ļź╝ ņĀ£ņŗ£ĒĢ£ļŗż. Benos(1998)ņŚÉ ļö░ļź┤ļ®┤ ņØ╝ļČĆ ņ£äĒŚś ņżæļ”ĮņĀü Ēł¼ņ×Éņ×ÉļōżņØ┤ ĻĘĖļōżņØś ņé¼ņĀüņØĖ ņĀĢļ│┤ļź╝ Ļ│╝ļīĆĒÅēĻ░ĆĒĢśņŚ¼ Ļ│╝ņŗĀĒĢśļŖö ĒśäņāüņØ┤ ļ░£ņāØĒĢśĻ│Ā, Ļ▓░Ļ│╝ņĀüņ£╝ļĪ£ Ļ│╝ņŗĀņØ┤ Ļ▒░ļלļ¤ēņØä ņ”ØĻ░Ćņŗ£Ēé©ļŗż. Gervais and Odean (2001)ņØĆ Ļ▒░ļלņ×ÉĻ░Ć ĻĘĖļōżņØś ļŖźļĀźņŚÉ ļīĆĒĢ┤ Ļ│╝ņŗĀĒĢ£ļŗżļŖö ņé¼ņŗżņØä ĒÖĢņØĖĒĢśĻ│Ā Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀņŚÉ ļö░ļźĖ Ļ▒░ļלļ¤ēĻ│╝ ĻĖ░ļīĆņØ┤ņØĄ, Ļ░ĆĻ▓®ļ│ĆļÅÖņä▒, ĻĖ░ļīĆĻ░ĆĻ▓®ņØś ļ│ĆĒÖöĒī©Ēä┤ņØä ļČäņäØĒĢ£ļŗż. Glaser and Weber(2009)ņŚÉ ļö░ļź┤ļ®┤ Ļ│╝Ļ▒░ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØĆ Ļ░£ņØĖ Ēł¼ņ×Éņ×ÉņØś Ļ▒░ļלĒÖ£ļÅÖ(Ļ▒░ļלļ¤ē, ĒżĒŖĖĒÅ┤ļ”¼ņśż ĒÜīņĀäņ£© ļō▒)ņŚÉ ņśüĒ¢źņØä ļ»Ėņ╣śļ®░ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀņŚÉ ņØśĒĢ┤ ļåÆņØĆ ņłśņżĆņØś Ļ▒░ļלļ¤ēņØ┤ ļ░£ņāØĒĢ£ļŗż. ņ£äņØś ņŗżņ”Ø Ļ▓░Ļ│╝ņŚÉ ļö░ļź┤ļ®┤ Ļ▒░ļלļ¤ēņØĆ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ Ļ│╝ņ×ēļ░śņØæņØä ļéśĒāĆļé┤ļŖö ļīĆņÜ®ņ╣śĻ░Ć ļÉ£ļŗż.

ņĄ£ĻĘ╝ņØś ļ¦ÄņØĆ ņŚ░ĻĄ¼ļŖö Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀņØ┤ ņŻ╝ņŗØņŗ£ņןņŚÉ ļ»Ėņ╣śļŖö ņśüĒ¢źņØä ļéśĒāĆļé┤ļ®░ ĻĖ░ņĪ┤ ņŚ░ĻĄ¼Ļ▓░Ļ│╝ļź╝ ņ¦Ćņ¦ĆĒĢśļŖö ņŗżņ”ØņĀü ņ”ØĻ▒░ļź╝ ņĀ£ņŗ£ĒĢ£ļŗż. Luo et al.(2021)ņØĆ ņĀĢļ│┤ņŚÉ ļīĆĒĢ┤ Ļ│╝ņŗĀĒĢśļŖö Ēł¼ņ×Éņ×ÉļŖö ņŻ╝ņŗØņŗ£ņןņŚÉ Ļ│╝ņ×ē ņ£ĀļÅÖņä▒ņØä Ļ│ĄĻĖēņØä ņ£ĀļÅäĒĢśļ®░, ņØ┤ļŖö ļ¬©ļ®śĒģĆ ĒśäņāüĻ│╝ ņØ┤ņ¢┤ņ¦äļŗżĻ│Ā ņŻ╝ņןĒĢ£ļŗż. Chuang and Lee(2006)ņŚÉ ļö░ļź┤ļ®┤ Ēł¼ņ×Éņ×ÉļŖö ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ Ļ│╝ņ×ēļ░śņØæĒĢśĻ│Ā Ļ│ĄņĀüņØĖ ņĀĢļ│┤ņŚÉ Ļ│╝ņåīļ░śņØæĒĢ£ļŗż. ļö░ļØ╝ņä£ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀņØĆ Ēł¼ņ×Éņ×Éļź╝ ļŹöņÜ▒ Ļ│ĄĻ▓®ņĀüņØ┤Ļ▓ī ļ¦īļōĀļŗż. Adebambo and Yan(2016)ņØĆ ļ¬©ļ®śĒģĆ ĒÜ©Ļ│╝ļź╝ ņäżļ¬ģĒĢśļŖöļŹ░ ņ׳ņ¢┤ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ ĒÄĖĒ¢źļÉ£ ņ×ÉĻĖ░ĻĘĆņØĖņØś ņŚŁĒĢĀņØä Ļ▓ĆĒåĀĒĢ£ļŗż. Ļ│╝ņŗĀņØ┤ ļåÆņØĆ ĒÄĆļō£ ļ¦żļŗłņĀĆĻ░Ć ĻĘĖļĀćņ¦Ć ļ¬╗ĒĢ£ ĒÄĆļō£ļ¦żļŗłņĀĆļ│┤ļŗż ļŹö Ēü░ ļ¬©ļ®śĒģĆ ņØ┤ņØĄĻ│╝ ļŹö Ļ░ĢĒĢ£ ņłśņØĄļźĀ ļ░śņĀäĒśäņāüņØä Ļ░Ćņ¦ĆļŖö Ļ▓āņØä ĒÖĢņØĖĒĢśņŚ¼ Daniel et al.(1998)ņØä ņ¦Ćņ¦ĆĒĢ£ļŗż. Cooper et al.(2004)ņŚÉ ļö░ļź┤ļ®┤ ļ¬©ļ®śĒģĆ ņĀäļץņØś ņłśņØĄņä▒ņØĆ ņŗ£ņןņØś ņāüĒā£ņŚÉ ļö░ļØ╝ ļ│ĆĒÖöĒĢśĻ│Ā Daniel et al.(1998)ņØś Ļ▓░Ļ│╝ņÖĆ ļÅÖņØ╝ĒĢśĻ▓ī ņāüņŖ╣ņŗ£ņן(up market)ņŚÉņä£ ļ¬©ļ®śĒģĆ ņĀäļץņØś ņłśņØĄņä▒ņØ┤ ļåÆļŗż. Chui et al.(2010)ņØĆ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ ĒÄĖĒ¢źļÉ£ ņ×ÉĻĖ░ĻĘĆņØĖņŚÉ Ļ┤ĆļĀ©ļÉ£ Ļ░£ņØĖņŻ╝ņØś ņ¦Ćņłśļź╝ ņĖĪņĀĢĒĢśņŚ¼ ļ¼ĖĒÖöņĀü ņ░©ņØ┤Ļ░Ć ļ¬©ļ®śĒģĆ ņĀäļץņØś ņłśņØĄļźĀņŚÉ ļ»Ėņ╣śļŖö ņśüĒ¢źņØä ņĪ░ņé¼ĒĢ£ļŗż. Hou et al.(2009)ņŚÉ ļö░ļź┤ļ®┤ ņāüņŖ╣ņŗ£ņןņŚÉņä£ Ļ▒░ļלļ¤ēņØ┤ ļ¦ÄņØĆ ņŻ╝ņŗØņØĆ ļ¬©ļ®śĒģĆ ņØ┤ņØĄņØä ņĘ©ĒĢ£ļŗż. Byun et al.(2016)ņØĆ Daniel et al.(1998)ņØä ļ░öĒāĢņ£╝ļĪ£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ļéśĒāĆļé┤ļŖö ņĖĪņĀĢņ╣śļź╝ ņĀĢņØśĒĢ£ļŗż. ļŹö ļéśņĢäĻ░Ć, Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ│╝ ņŻ╝ņŗØņłśņØĄļźĀņØś ņ¢æņØś Ļ┤ĆĻ│äļź╝ ĒÖĢņØĖĒĢ£ļŗż.

Byun et al.(2016)ņØĆ ļ»ĖĻĄŁ ņŻ╝ņŗØņŗ£ņןņ£╝ļĪ£ Ēæ£ļ│Ėņ£╝ļĪ£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņŚÉ ļīĆĒĢ£ ņĖĪņĀĢņ╣śļź╝ ļÅäņČ£ĒĢśņŚ¼ Daniel et al.(1998)ņŚÉ ļīĆĒĢ£ ņŗżņ”ØņĀü ņ”ØĻ▒░ļź╝ ņĀ£Ļ│ĄĒĢ£ļŗż. Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ(continuing overreaction)ņØä ļéśĒāĆļé┤ļŖö COļ│ĆņłśļŖö ļÅÖņŗ£Ļ░äļīĆ ņŻ╝ņŗØņłśņØĄļźĀĻ│╝ ņøöļ│äĻ▒░ļלļīĆĻĖłņ£╝ļĪ£ ĻĄ¼ņä▒ļÉ£ļŗż. Ļ▒░ļלļīĆĻĖłņØĆ Ļ░Ćņżæņ╣śĻ░Ć ļČĆņŚ¼ļÉ£ ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ēņØä ņé¼ņÜ®ĒĢ£ļŗż. Byun et al.(2016)ņŚÉ ļö░ļź┤ļ®┤ COļŖö Ļ│╝Ļ▒░ņłśņØĄļźĀļ│┤ļŗż ļ»ĖļלņłśņØĄļźĀņŚÉ ļīĆĒĢ£ ņśłņĖĪļĀźņØ┤ ļåÆĻ│Ā, COņĀäļץņØś ņłśņØĄņä▒ņØĆ ļ¬©ļ®śĒģĆ ņĀäļץņØś ņłśņØĄļźĀņØä ņĪ░ņĀĢĒĢ£ ĒøäņŚÉļÅä ņ£Āņ¦ĆļÉ£ļŗż. COĻ░Ć Ļ░Ćņן ļåÆņØĆ ņŻ╝ņŗØņØä ļ¦żņ×ģĒĢśĻ│Ā COĻ░Ć Ļ░Ćņן ļé«ņØĆ ņŻ╝ņŗØņØä ļ¦żļÅäĒĢśļŖö COņĀäļץņØĆ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦Ćļ®░, COņĀäļץņØś ņłśņØĄļźĀņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ņØ┤Ēøä 12Ļ░£ņøöĻ╣īņ¦Ć ņ¦ĆņåŹļÉ£ļŗż.

3.ŌĆģņ×ÉļŻīŌĆģļ░ÅŌĆģļ░®ļ▓ĢļĪĀ

3.1 Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ

Daniel et al.(1998)ņŚÉ ļö░ļź┤ļ®┤ Ēł¼ņ×Éņ×ÉļŖö ņé¼ņĀüņØĖ ņĀĢļ│┤(private information)ņŚÉ ļīĆĒĢ┤ Ļ│╝ņŗĀ(overconfidence)ĒĢśļŖö Ļ▓ĮĒ¢źņØ┤ ņ׳ļŗż. ļśÉĒĢ£, Ēł¼ņ×Éņ×ÉņØś ĒÄĖĒ¢źļÉ£ ņ×ÉĻĖ░ĻĘĆņØĖ(biased self-attribution)ņØĆ ņŻ╝ņŗØ ņŗ£ņןņŚÉņä£ ļ░£ņāØĒĢśļŖö Ļ│╝ņåīļ░śņØæ(under-reaction)Ļ│╝ Ļ│╝ļīĆļ░śņØæ(over-reaction)ņØä ņäżļ¬ģĒĢ£ļŗż. Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØĆ Ēł¼ņ×Éņ×ÉĻ░Ć ĻĘĖļōżņØś ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢśņŚ¼ Ļ│╝ņŗĀĒĢĀ ļĢī ļ░£ņāØĒĢ£ļŗż. ļåÆņØĆ(ļé«ņØĆ) Ļ│╝Ļ▒░ņłśņØĄļźĀņØĆ ņ¢æ(ņØī)ņØś ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ Ēł¼ņ×Éņ×ÉņØś ņ¢æ(ņØī)ņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ņĢ╝ĻĖ░ĒĢ£ļŗż. Daniel et al.(1998)ņŚÉ ļö░ļź┤ļ®┤ Ļ│╝Ļ▒░ņłśņØĄļźĀņØĆ ļ»ĖļלņłśņØĄļźĀņŚÉ ļīĆĒĢ£ ņśłņĖĪļĀźņØä Ļ░Ćņ¦äļŗż. ļö░ļØ╝ņä£ Ļ│╝Ļ▒░ņłśņØĄļźĀņØä ĻĖ░ļ░śņ£╝ļĪ£ ņĀĢņØśĒĢ£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØĆ ļ»ĖļלņłśņØĄļźĀņØä ņśłņĖĪĒĢ£ļŗż. ņ”ē, Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØĆ ļ»ĖļלņłśņØĄļźĀņŚÉ ļīĆĒĢ£ ņ¦üņĀæņĀüņØĖ ņĖĪņĀĢņ╣śņØ┤ļ®░ Ēł¼ņ×Éņ×ÉņØś Ļ│äņåŹņĀüņØĖ Ļ│╝ņ×ēļ░śņØæņØ┤ ļ¬©ļ®śĒģĆ ĒśäņāüņØä ņĢ╝ĻĖ░ĒĢ£ļŗż. Byun et al.(2016)ņØĆ Daniel et al.(1998)ņŚÉ ļö░ļØ╝ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ļéśĒāĆļé┤ļŖö ņŗżņ”ØņĀüņØĖ ņĖĪņĀĢņ╣śļź╝ ņĀ£ņŗ£ĒĢ£ļŗż. ļŹö ļéśņĢäĻ░Ć, Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ ĒÄĖĒ¢źļÉ£ ņ×ÉĻĖ░ĻĘĆņØĖņ£╝ļĪ£ ņØĖĒĢ£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØ┤ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆĒĢ£ ņśłņĖĪņä▒ņØä Ļ░Ćņ¦ĆļŖöņ¦Ć ņŚ¼ļČĆļź╝ ĒÖĢņØĖĒĢ£ļŗż. Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś ņĖĪņĀĢņ╣śļŖö ļŗżņØīĻ│╝ Ļ░ÖņØ┤ ĻĄ¼ņä▒ļÉ£ļŗż.

ņ▓½ņ¦Ė, ņøöļ│äĻ▒░ļלļ¤ēņØä Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀ ļśÉļŖö Ļ│╝ņ×ēļ░śņØæņØś ļīĆņÜ®ņ╣śļĪ£ ņé¼ņÜ®ĒĢ£ļŗż. Benos(1998)ņŚÉ ļö░ļź┤ļ®┤ Ēł¼ņ×Éņ×ÉļŖö ĻĘĖļōżņØś ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢśņŚ¼ ļŹö ļ¦ÄņØĆ Ļ░Ćņżæņ╣śļź╝ ļČĆņŚ¼ĒĢ£ļŗż. ļö░ļØ╝ņä£ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀņØĆ ļŹöņÜ▒ Ļ│ĄĻ▓®ņĀüņØĖ Ļ▒░ļלļź╝ ņĢ╝ĻĖ░ĒĢ£ļŗż. Benos(1998)ņÖĆ Odean(1998)ņØś ņŚ░ĻĄ¼ļŖö Ļ│╝ņŗĀņØ┤ Ļ▒░ļלļ¤ēņØä ņ”ØĻ░Ćņŗ£Ēéżļ»ĆļĪ£ ļåÆņØĆ Ļ▒░ļלļ¤ēņØ┤ Ļ│╝ņŗĀņØś ņĀĢļÅäļØ╝Ļ│Ā ļéśĒāĆļéĖļŗż. Statman et al.(2006)ņØĆ ļ▓ĪĒä░ņ×ÉĻĖ░ ĒÜīĻĘĆļ¬©ĒśĢĻ│╝ ņČ®Ļ▓®ļ░śņØæĒĢ©ņłśļź╝ ņØ┤ņÜ®ĒĢśņŚ¼ ņŗ£ņןņØś ņĀäļ░śņĀüņØĖ Ļ▒░ļלļ¤ēņØ┤ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ ļööņŖżĒżņ¦Ćņģś ĒÜ©Ļ│╝ļź╝ ņäżļ¬ģĒĢĀ ņłś ņ׳ļŗżĻ│Ā ņĀ£ņŗ£ĒĢ£ļŗż. Grinblatt and Keloharju(2009)ļŖö ĒĢĆļ×Ćļō£ ņŻ╝ņŗØĻ▒░ļל ļŹ░ņØ┤Ēä░ļź╝ ņØ┤ņÜ®ĒĢśņŚ¼ Ļ░ÉĻ░ü ņČöĻĄ¼(sensation seeking)ņÖĆ Ļ│╝ņŗĀņØ┤ Ēł¼ņ×Éņ×ÉņØś ņŻ╝ņŗØĻ▒░ļלņŚÉ ļ»Ėņ╣śļŖö ņśüĒ¢źņØä ĒÖĢņØĖĒĢ£ļŗż. ĒŖ╣Ē׳, ņ×¼ņé░, ņåīļōØ, ļéśņØ┤, ņŻ╝ņŗØ ļ│┤ņ£Ā ņłś ļō▒ņØä ĒżĒĢ©ĒĢ£ ļŗżņłśņØś ļ│Ćņłśļź╝ ĒåĄņĀ£ĒĢśņŚ¼ Ļ▒░ļלļ╣łļÅäĻ░Ć ļåÆņØĆ Ēł¼ņ×Éņ×ÉņØ╝ņłśļĪØ Ļ│╝ņŗĀĒĢśļŖö Ļ▓ĮĒ¢źņØ┤ ļåÆņØīņØä ļ│┤ņØĖļŗż. ņ£äņØś ņŚ░ĻĄ¼ļōżņØĆ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ Ļ▒░ļלļ¤ēĻ░äņØś ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ┤ĆĻ│äļź╝ ņĀ£ņŗ£ĒĢśĻ│Ā, Ļ▒░ļלļ¤ēņØ┤ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀ ļśÉļŖö Ļ│╝ņ×ēļ░śņØæņØä ļéśĒāĆļé┤ļŖö ļīĆņÜ®ņ╣śļĪ£ ņé¼ņÜ®ļÉĀ ņłś ņ׳ņØīņØä ļÆĘļ░øņ╣©ĒĢ£ļŗż.

ļæśņ¦Ė, ļÅÖņŗ£Ļ░äļīĆ ņøöļ│äņłśņØĄļźĀĻ│╝ ņøöļ│äĻ▒░ļלļīĆĻĖłņØä ĒåĄĒĢ┤ ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ē(signed volume)ņØä ĻĄ¼ņä▒ĒĢśņŚ¼ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņ×ēļ░śņØæņØś ļ░®Ē¢źņØä ļéśĒāĆļéĖļŗż. Byun et al.(2016)ņŚÉ ļö░ļź┤ļ®┤ ņ¢æņØś ņłśņØĄļźĀņØä ļÅÖļ░śĒĢśļŖö ļåÆņØĆ ņłśņżĆņØś Ļ▒░ļלļ¤ēņØĆ ņ¢æņØś ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀņØä, ņØīņØś ņłśņØĄļźĀņØä ļÅÖļ░śĒĢśļŖö ļåÆņØĆ ņłśņżĆņØś Ļ▒░ļלļ¤ēņØ┤ ņØīņØś ņé¼ņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀņØä ņØśļ»ĖĒĢ£ļŗż.

tņøöņØśiļ▓łņ¦Ė ņŻ╝ņŗØņØś ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ēņØĆ ļŗżņØīĻ│╝ Ļ░Öļŗż.

ri,tļŖöiņøöņØśiļ▓łņ¦Ė ņŻ╝ņŗØņłśņØĄļźĀņØ┤ļŗż. VOLi,tļŖötņøöņØśiļ▓łņ¦Ė ņŻ╝ņŗØņØś ņøöļ│äĻ▒░ļלļīĆĻĖłņ£╝ļĪ£ Ļ░ü ļŗ¼ņØś ņØ╝ļ│äĻ▒░ļלļ¤ēņŚÉ ņóģĻ░Ćļź╝ Ļ│▒ĒĢ£ Ļ░ÆņØś ĒĢ®ņ£╝ļĪ£ ņĀĢņØśĒĢ£ļŗż. Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ(CO)ņØĆ ņŗØ (2)ņŚÉ ļö░ļØ╝ ļÅäņČ£ļÉ£ļŗż. ļ©╝ņĀĆ, ņĄ£ĻĘ╝ņØś ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ēņŚÉ ļŹö ļåÆņØĆ Ļ░Ćņżæņ╣śļź╝ ļČĆņŚ¼ĒĢśĻ│Ā ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ēņØś ĒĢ®ņØä ĻĄ¼ĒĢ£ļŗż. ļŗżņØīņ£╝ļĪ£, ļÅÖņØ╝ĒĢ£ ĻĖ░Ļ░äņØś ĒÅēĻĘĀ Ļ▒░ļלļ¤ēņ£╝ļĪ£ Ļ░Ćņżæņ╣śĻ░Ć ļČĆņŚ¼ļÉ£ ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ēņØä ņĀĢĻĘ£ĒÖöĒĢ£ļŗż. ņØ┤ļŖö ņŗ£Ļ░äņŚÉ ļö░ļØ╝ ņ”ØĻ░Ć ļśÉļŖö ĒĢśļØĮĒĢśļŖö Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀņØä ĒÖĢņØĖĒĢ£ļŗż.

SVi,tļŖö ņŗØ (1)ņŚÉ ņØśĒĢ┤ ļÅäņČ£ļÉ£tņøöņØśiļ▓łņ¦Ė ņŻ╝ņŗØņØś ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ēņØ┤Ļ│Ā, JļŖö ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äņØ┤ļŗż. ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äņØä 1ļģä(J=12)ņ£╝ļĪ£ ņäżņĀĢĒĢ£ļŗż. ļÅäņČ£ĻĖ░Ļ░äņØä ļ│ĆĻ▓ĮĒĢ£ Ļ▓░Ļ│╝ļŖö ņĀ£ŌĆģ5ņן ņĀ£ŌĆģ1ņĀłņŚÉ ļéśĒāĆļéĖļŗż. wiļŖöt-jņøöņŚÉ ļČĆņŚ¼ĒĢśļŖö Ļ░Ćņżæņ╣śļĪ£J-j+1ņØś Ļ░ÆņØ┤ļŗż (wJ =1, wJ-1 =2, ŌĆ”, w1 =J). ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖöCOi,tļź╝ Ēł¼ņ×Éņ×ÉņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ļéśĒāĆļé┤ļŖö ņĖĪņĀĢņ╣śļĪ£ ņé¼ņÜ®ĒĢ£ļŗż.

Daniel et al.(1998)ņØś ņŚ░ĻĄ¼ļŖö ĒÄĖĒ¢źļÉ£ ņ×ÉĻĖ░ĻĘĆņØĖņØ┤ ņżæĻĖ░(intermediate-term)ņłśņØĄļźĀņØä ņśłņĖĪĒĢśļŖö ĒĢĄņŗ¼ņÜöņåīļØ╝Ļ│Ā ļéśĒāĆļéĖļŗż. ļö░ļØ╝ņä£ ĒÄĖĒ¢źļÉ£ ņ×ÉĻĖ░ĻĘĆņØĖņØĆ Ļ│╝ņŗĀņØś ņ”ØĻ░ĆņČöņäĖļź╝ ļéśĒāĆļé┤ļŖö Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņ£╝ļĪ£ ņØ┤ņ¢┤ņ¦äļŗż. ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äļÅÖņĢł ĒÅēĻĘĀ Ļ▒░ļלļ¤ēņØä ņ£Āņ¦ĆĒĢ£ļŗżļ®┤, ņĄ£ĻĘ╝ ļŗ¼ņØś Ļ▒░ļלļ¤ēņŚÉ Ļ░Ćņżæņ╣śĻ░Ć ļåÆņØäņłśļĪØ Ļ▒░ļלļ¤ēņØś ĒĢ®ņØĆ ļŹöņÜ▒ ļåÆņĢäņ¦äļŗż. Lee and Swaminathan(2000)ņŚÉ ļö░ļź┤ļ®┤ Ļ│╝Ļ▒░Ļ▒░ļלļ¤ēņØĆ Ļ░ĆĻ▓®ļ¬©ļ®śĒģĆņØś ĻĘ£ļ¬©ņÖĆ ņ¦ĆņåŹņä▒ņØä ņśłņĖĪĒĢśļ®░ ņżæĻĖ░ņłśņØĄļźĀņØś Ļ│╝ņåīļ░śņØæĻ│╝ ņןĻĖ░ņłśņØĄļźĀņØś Ļ│╝ņ×ēļ░śņØæĒÜ©Ļ│╝ļź╝ ņĪ░ņĀĢĒĢśļŖöļŹ░ ļÅäņøĆņØä ņżĆļŗż. ļö░ļØ╝ņä£ ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ēņØä ĒĢ®ĒĢśĻ│Ā ļÅÖņØ╝ĻĖ░Ļ░äņØś ĒÅēĻĘĀĻ▒░ļלļ¤ēņ£╝ļĪ£ ņĀĢĻĘ£ĒÖöĒĢ£ Ļ░ÆņØĆ Ēł¼ņ×Éņ×É Ļ│╝ņŗĀņØś ņČöņäĖļź╝ ļéśĒāĆļéĖļŗż.

3.2 ņŻ╝ņÜö ļ│Ćņłś

ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö COņÖĆ ņŻ╝ņŗØņłśņØĄļźĀ Ļ░äņØś ĒÜĪļŗ©ļ®┤ņĀü Ļ┤ĆĻ│äļź╝ ņĪ░ņé¼ĒĢśĻĖ░ ņ£äĒĢ┤ ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØś ņśüĒ¢źņØä Ļ│ĀļĀżĒĢ£ļŗż. ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØś ņĀĢņØśļŖö ļŗżņØīĻ│╝ Ļ░Öļŗż.

ĻĖ░ņŚģĻĘ£ļ¬©(SIZE)ņÖĆ ņןļČĆĻ░Ćņ╣ś ļīĆ ņŗ£ņןĻ░Ćņ╣ś(BEME)ļŖö Fama and French(1992, 1993)ņŚÉ ļö░ļźĖ ņŗ£ņןĻ░Ćņ╣śņØś ņ×ÉņŚ░ļĪ£ĻĘĖļź╝ ņĘ©ĒĢ£ Ļ░ÆĻ│╝ ĒÜīĻ│äņŚ░ļÅä ņןļČĆĻ░Ćņ╣ś ļīĆ ņŗ£ņןĻ░Ćņ╣ś ļ╣äņ£©(book-to-market ratio)ņØ┤ļŗż. ņāüļīĆņĀüņ£╝ļĪ£ ļĀłļ▓äļ”¼ņ¦ĆĻ░Ć ļåÆņØĆ ĻĖ░ņŚģ(ĻĖłņ£ĄņŚģ, ņØĆĒ¢ēņŚģ, ļ│┤ĒŚśņŚģ ļō▒)ņØĆ Ēæ£ļ│ĖņŚÉņä£ ņĀ£ņÖĖĒĢ£ļŗż. ņŗ£ņןļ▓ĀĒāĆ(BETA)ļŖö ņŗØ (3)ņŚÉ ļö░ļØ╝tņøöņØś ņ┤łĻ│╝ņłśņØĄļźĀĻ│╝ ņŗ£ņן ņ┤łĻ│╝ņłśņØĄļźĀņØä ņé¼ņÜ®ĒĢśņŚ¼ Ļ│äņé░ĒĢ£ļŗż. ļ¦ż ņøö ņØ╝ļ│ä ņłśņØĄļźĀ Ļ┤ĆņĖĪņ╣śņØś Ļ░£ņłśĻ░Ć 12Ļ░£ ļ»Ėļ¦īņØĖ ņŻ╝ņŗØņØĆ ņĀ£ņÖĖĒĢ£ļŗż.

Ri,dņØĆdņØ╝ņØśiļ▓łņ¦Ė ņŻ╝ņŗØņłśņØĄļźĀņØ┤Ļ│Ā, Rm,dņØĆdņØ╝ņØś ņŗ£ņןņłśņØĄļźĀņØ┤ļŗż. rf,dņØĆdņØ╝ņØś ļ¼┤ņ£äĒŚś ņłśņØĄļźĀņØ┤ļŗż. ņÜ░ļ”¼ļŖö ļ¦żņøö ņØ╝ļ│ä ņłśņØĄļźĀļĪ£ ņŗØ (3)ņØä ņØ┤ņÜ®ĒĢśņŚ¼ Ļ░ü ņŻ╝ņŗØņØś ļ▓ĀĒāĆļź╝ ĻĄ¼ĒĢ£ļŗż. (╬▓╦å iļŖötņøöiļ▓łņ¦Ė ņŻ╝ņŗØņØś ņŗ£ņןļ▓ĀĒāĆņØ┤ļŗż.

Ļ│╝Ļ▒░ņłśņØĄļźĀ(PRET)ņØĆt-12ņøöļČĆĒä░t-2ņøöņØś ļłäņĀüņłśņØĄļźĀņØ┤ļŗż. ļŗ©ĻĖ░ņłśņØĄļźĀļ░śņĀä(REV)ņØĆ Jegadeesh(1990)Ļ│╝ Lehmann(1990)ņŚÉ ļö░ļźĖ ļŗ©ĻĖ░ņłśņØĄļźĀ ļ░śņĀä(reversal)ņØ┤ļŗż. Ļ░ü ņŻ╝ņŗØņŚÉ ļīĆĒĢśņŚ¼tņøöņØś REVļŖö Ļ│╝Ļ▒░ 1Ļ░£ņøö ņĀä ņłśņØĄļźĀļĪ£ ņĀĢņØśĒĢ£ļŗż. ņ£ĀļÅÖņä▒(ILLIQ)ņØĆ Amihud(2002)ņŚÉ ļö░ļźĖ ņ£ĀļÅÖņä▒ ņĖĪņĀĢņ╣śņØ┤ļ®░ ņŗØ (4)ņÖĆ Ļ░Öļŗż.

Ri,dņØĆdļ▓łņ¦Ė Ļ▒░ļלņØ╝ņØś ņŻ╝ņŗØņłśņØĄļźĀņØ┤Ļ│Ā, DiļŖötņŗ£ņĀÉņŚÉņä£iļ▓łņ¦Ė ņŻ╝ņŗØņØś Ļ▒░ļלļ¤ēņØ┤ 0ņØ┤ ņĢäļŗī Ļ▒░ļלņØ╝ ņłśļź╝, VOLDi,dļŖödļ▓łņ¦Ė Ļ▒░ļלņØ╝ņØś Ļ▒░ļלļīĆĻĖłņØä ņØśļ»ĖĒĢ£ļŗż.

Ļ│Āņ£Āļ│ĆļÅÖņä▒(IVOL)ņØĆ Bali et al.(2011)ņŚÉ ļö░ļźĖ Ļ│Āņ£Āļ│ĆļÅÖņä▒ņØ┤ļŗż. ╬Ąi,dļŖö ņŗØ (3)ņØä ĒåĄĒĢ┤ ļÅäņČ£ļÉśļ®░ ņøöļ│ä IVOLņØĆ╬Ąi,dņŚÉ Ēæ£ņżĆĒÄĖņ░©ļź╝ ņĘ©ĒĢ£ Ļ░Æņ£╝ļĪ£ ņŗØ (5)ņÖĆ Ļ░Öļŗż.

Ļ▒░ļלļ¤ēĒÜīņĀäņ£©(TURN)ņØĆt-12ņøöļČĆĒä░t-1ņøöņØś ĒÅēĻĘĀ ņøöļ│äĻ▒░ļלļ¤ēĒÜīņĀäņ£©ņØ┤ļŗż.

3.3 ņ×ÉļŻī

ļ│Ė ņŚ░ĻĄ¼ļŖö 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ĻĄŁļé┤ ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņןĻ│╝ ņĮöņŖżļŗź ņŗ£ņןņŚÉ ņāüņןļÉ£ ņŻ╝ņŗØņØä Ēæ£ļ│Ėņ£╝ļĪ£ ĒĢ£ļŗż. ņ×ÉļŻīņØś ņĀĢĒÖĢņä▒ņØ┤ ļ¢©ņ¢┤ņ¦ĆļŖö Ļ▓āņØä ļ░®ņ¦ĆĒĢśĻĖ░ ņ£äĒĢśņŚ¼ ņóģĻ░ĆĻ░Ć 500ņøÉ ņØ┤ĒĢśņØĖ ņŻ╝ņŗØņØĆ Ēæ£ļ│ĖņŚÉņä£ ņĀ£ņÖĖĒĢ£ļŗż. ņāüņן ĒÅÉņ¦ĆļÉ£ ņŻ╝ņŗØņØś Ļ▓ĮņÜ░ ņāüņן ĒÅÉņ¦Ć ņĀä 6Ļ░£ņøöņØś ņŻ╝Ļ░Ćņ×ÉļŻīņÖĆ ņŻ╝ņŗØļŹ░ņØ┤Ēä░Ļ░Ć 12Ļ░£ņøö ņØ┤ĒĢśņØĖ ĻĖ░ņŚģņØĆ Ēæ£ļ│ĖņŚÉņä£ ņĀ£ņÖĖĒĢ£ļŗż. ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö Fama and French(1993)ņØś 3ņÜöņØĖļ¬©ĒśĢņŚÉ ļö░ļźĖ ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØä ņé¼ņÜ®ĒĢ£ļŗż. ļö░ļØ╝ņä£ ņāüļīĆņĀüņ£╝ļĪ£ ļĀłļ▓äļ”¼ņ¦ĆĻ░Ć ļåÆņØĆ ĻĖ░ņŚģ(ĻĖłņ£ĄņŚģ, ņØĆĒ¢ēņŚģ, ļ│┤ĒŚśņŚģ ļō▒)ņØĆ Ēæ£ļ│ĖņŚÉņä£ ņĀ£ņÖĖĒĢ£ļŗż. ņØ╝ļ│äņłśņØĄļźĀņØĆ ĒĢ£ĻĄŁĻ▒░ļלņåīņŚÉņä£ ĻĘ£ņĀĢĒĢ£ Ļ░ĆĻ▓®ņĀ£ĒĢ£ĒÅŁņŚÉ ļö░ļØ╝ ņĪ░ņĀĢĒĢ£ļŗż. ļČäņäØĻĖ░Ļ░ä ņżæ ņāüņןĒÅÉņ¦Ć ĻĖ░ņŚģņØä ņĀ£ņÖĖĒĢĀ Ļ▓ĮņÜ░ ņāØņĪ┤ĒÄĖņØś(survival bias)Ļ░Ć ļ░£ņāØĒĢśļ»ĆļĪ£ ņāüņןĒÅÉņ¦Ć ĻĖ░ņŚģļÅä ļČäņäØ ļīĆņāüņŚÉ ĒżĒĢ©ĒĢ£ļŗż. ņŗ£Ļ│äņŚ┤ ļČäņäØņŚÉņä£ ņé¼ņÜ®ļÉ£ ĻĖ░Ļ░äņØĆ 246Ļ░£ņøöņØ┤ļ®░, ļČäņäØ ļīĆņāü ĻĖ░ņŚģ ņłśļŖö ņŗ£Ļ│äņŚ┤ ĒÅēĻĘĀ 1499Ļ░£ņØ┤ļŗż. Ēæ£ļ│ĖņŚÉ ņé¼ņÜ®ļÉ£ ņ×ÉļŻīļŖö FnGuideņŚÉņä£ ņĀ£Ļ│Ąļ░øņĢśļŗż. ļ¼┤ņ£äĒŚś ņłśņØĄļźĀņØĆ ĒåĄĒÖöņĢłņĀĢņ▒äĻČī 364ņØ╝ ļ¦īĻĖ░ņłśņØĄļźĀņØ┤Ļ│Ā, ņŗ£ņןņłśņØĄļźĀņØĆ ļ¦żņøö ļ¬©ļōĀ ĻĖ░ņŚģņŚÉ ļīĆĒĢ£ Ļ░Ćņ╣śĻ░ĆņżæņłśņØĄļźĀņØ┤ļŗż.

<Ēæ£ 1>ņØĆ ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ ņé¼ņÜ®ļÉ£ ņ×ÉļŻīņŚÉ ļīĆĒĢ£ ĻĖ░ņłĀĒåĄĻ│äļ¤ēņØ┤ļŗż. Ēī©ļäÉ AļŖö COņØś ņÜöņĢĮĒåĄĻ│äļ¤ēņØ┤ļŗż. Ēī©ļäÉ BļŖö ļ¦żņøö COļź╝ ĻĖ░ņżĆņ£╝ļĪ£ ĻĄ¼ņä▒ĒĢ£ 10ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØś ļ│Ćņłś Ļ░ÆņØś ņŗ£Ļ│äņŚ┤ ĒÅēĻĘĀņØ┤ļŗż. Ēī©ļäÉ CļŖö ļ│ĆņłśĻ░äņØś ĒÜĪļŗ©ļ®┤ņĀü ņāüĻ┤ĆĻ┤ĆĻ│äņØś ņŗ£Ļ│äņŚ┤ ĒÅēĻĘĀņØ┤ļŗż. COņØś ĒÅēĻĘĀĻ░ÆņØĆ 11.394ņØ┤ļ®░ Ēæ£ņżĆĒÄĖņ░©ļŖö 9.632ņØ┤ļŗż. <Ēæ£ 1>ņØś Ēī©ļäÉ BņŚÉ ļö░ļź┤ļ®┤ COĻ░Ć ļåÆņØĆ ņŻ╝ņŗØņØ╝ņłśļĪØ ĻĖ░ņŚģĻĘ£ļ¬©(SIZE), ņןļČĆĻ░Ćņ╣ś ļīĆ ņŗ£ņןĻ░Ćņ╣ś(BEME), ņŗ£ņןļ▓ĀĒāĆ(BETA), Ļ│╝Ļ▒░ņłśņØĄļźĀ(PRET), ļŗ©ĻĖ░ņłśņØĄļźĀļ░śņĀä(REV), Ļ│Āņ£Āļ│ĆļÅÖņä▒(IVOL)ņØ┤ ļåÆņØĆ Ļ▓ĮĒ¢źņØ┤ ņ׳ļŗż. ļ░śļ®┤, COĻ░Ć ņ”ØĻ░ĆĒĢ©ņŚÉ ļö░ļØ╝ ņ£ĀļÅÖņä▒(ILLIQ)ņØĆ ĒĢśļØĮĒĢśļŖö Ļ▓ĮĒ¢źņØ┤ ņ׳ņ£╝ļ®░, Ļ▒░ļלļ¤ēĒÜīņĀäņ£©(TURN)ņØś Ļ▓ĮņÜ░ COņÖĆ ļłłņŚÉ ļØäļŖö Ļ┤ĆĻ│äĻ░Ć ļéśĒāĆļéśņ¦Ć ņĢŖļŖöļŗż. <Ēæ£ 1>ņØś Ēī©ļäÉ CņŚÉ ņØśĒĢśļ®┤ Ēī©ļäÉ BņÖĆ ņ£Āņé¼ĒĢśĻ▓ī ĻĖ░ņŚģĻĘ£ļ¬©(SIZE), ņןļČĆĻ░Ćņ╣ś ļīĆ ņŗ£ņןĻ░Ćņ╣ś(BEME), ņŗ£ņןļ▓ĀĒāĆ(BETA), Ļ│╝Ļ▒░ņłśņØĄļźĀ(PRET), ļŗ©ĻĖ░ņłśņØĄļźĀļ░śņĀä(REV), Ļ│Āņ£Āļ│ĆļÅÖņä▒(IVOL)ņØĆ COņÖĆ ņ¢æņØś ņāüĻ┤ĆĻ┤ĆĻ│äņŚÉ ņ׳Ļ│Ā, ņ£ĀļÅÖņä▒(ILLIQ)ņØĆ COņÖĆ ņØīņØś ņāüĻ┤ĆĻ┤ĆĻ│äĻ░Ć ļéśĒāĆļé£ļŗż. Ļ▒░ļלļ¤ēĒÜīņĀäņ£© (TURN)ņØĆ COņÖĆ ņ¢æņØś ņāüĻ┤ĆĻ┤ĆĻ│äņŚÉ ņ׳ņ£╝ļéś ĻĘĖ Ēü¼ĻĖ░Ļ░Ć ņ×æņĢä Ēī©ļäÉ BņŚÉņä£ ļÜ£ļĀĘĒĢ£ Ēī©Ēä┤ņØ┤ ļéśĒāĆļéśņ¦Ć ņĢŖļŖöļŗż. ĒŖ╣Ē׳, COņÖĆ Ļ│╝Ļ▒░ņłśņØĄļźĀ(PRET), ļŗ©ĻĖ░ņłśņØĄļźĀļ░śņĀä(REV)ņØś ņāüĻ┤ĆĻ│äņłśļŖö 0.351, 0.356ņ£╝ļĪ£ ļŗżļźĖ ņÜöņØĖņŚÉ ļ╣äĒĢśņŚ¼ ļåÆņØĆ ņāüĻ┤ĆĻ┤ĆĻ│äļź╝ Ļ░Ćņ¦äļŗż. ņÜ░ļ”¼ļŖö ņĀ£ 4ņןņŚÉņä£ ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØś ņśüĒ¢źņØ┤ COņĀäļץņŚÉ Ļ┤ĆņŚ¼ĒĢśļŖöņ¦Ć ĒÖĢņØĖĒĢ£ļŗż.

<Ēæ£┬Ā1>

ĻĖ░ņłĀĒåĄĻ│äļ¤ē

ņØ┤ Ēæ£ļŖö 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņןĻ│╝ ņĮöņŖżļŗźņŗ£ņןņŚÉ ņāüņןļÉ£ ĻĖ░ņŚģļōżņØś ņøöļ│ä ņ×ÉļŻīņŚÉ ļīĆĒĢ£ ĻĖ░ņłĀĒåĄĻ│äļ¤ēņØ┤ļŗż. Ēī©ļäÉ AļŖö Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņŚÉ ļīĆĒĢ£ ņĖĪņĀĢņ╣śņØĖ COņØś ĒÅēĻĘĀ, ņżæņĢÖĻ░Æ, Ēæ£ņżĆĒÄĖņ░©, 1st, 25th, 50th, 75th, 99th ļČäņ£äņłśņØś ņŗ£Ļ│äņŚ┤ ĒÅēĻĘĀĻ░ÆņØä ļéśĒāĆļéĖļŗż. Ēī©ļäÉ BļŖö COļź╝ ĻĖ░ņżĆņ£╝ļĪ£ 10ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢ£ Ēøä, Ļ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢśļŖö ļ│ĆņłśļōżņØś ņŗ£Ļ│äņŚ┤ ĒÅēĻĘĀņØä ļéśĒāĆļéĖļŗż. Ēī©ļäÉ CļŖö ļ│ĆņłśļōżņØś ĒÜĪļŗ©ļ®┤ņĀü ņāüĻ┤ĆĻ│äņłśņØś ņŗ£Ļ│äņŚ┤ ĒÅēĻĘĀņØä ļéśĒāĆļéĖļŗż.

Ēī©ļäÉ A: CO ņÜöņĢĮĒåĄĻ│äļ¤ē

3.4 ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒

3.4.1 ļŗ©ļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśż

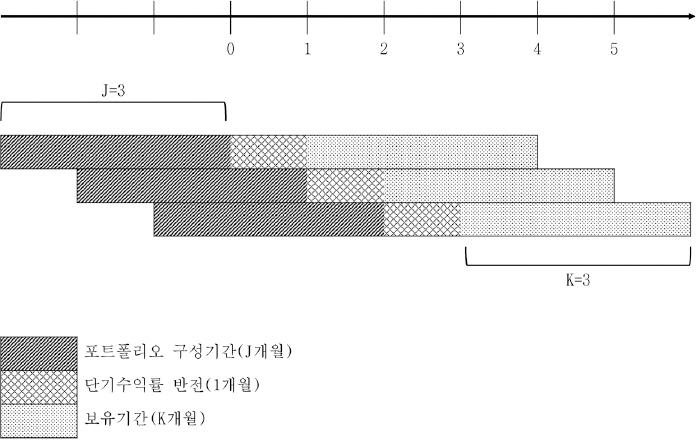

ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö Jegadeesh and Titman(1993)ņŚÉ ļö░ļØ╝ ņżæļ│Ą ĒżĒŖĖĒÅ┤ļ”¼ņśż(overlapping portfolio)ļź╝ ĻĄ¼ņä▒ĒĢ£ļŗż. 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņןĻ│╝ ņĮöņŖżļŗźņŗ£ņןņŚÉ ņāüņןļÉ£ ĻĖ░ņŚģņØä ļīĆņāüņ£╝ļĪ£ ļ¦żtņøöņØś ņŗ£ņ×æņŗ£ņĀÉņŚÉņä£ ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢ£ļŗż. Ļ│╝Ļ▒░JĻ░£ņøö(t-JņøöļČĆĒä░t-1ņøö)ņØś ņøöļ│äņŻ╝ņŗØņłśņØĄļźĀĻ│╝ ņøöļ│äĻ▒░ļלļīĆĻĖłņØä ņØ┤ņÜ®ĒĢśņŚ¼tņøöņØś COļź╝ Ļ│äņé░ĒĢ£ļŗż. ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö Ļ│╝Ļ▒░ 12Ļ░£ņøö ņŻ╝ņŗØļŹ░ņØ┤Ēä░(J=12)ļź╝ ņØ┤ņÜ®ĒĢśņŚ¼ COļź╝ ļÅäņČ£ĒĢśļ®░, ņĀ£ 5ņן ņĀ£1ņĀłņŚÉņä£JĻĖ░Ļ░äņØś ļ│ĆĒÖöņŚÉ ļö░ļźĖ Ļ▓░Ļ│╝ļź╝ ļéśĒāĆļéĖļŗż. COļź╝ ĻĖ░ņżĆņ£╝ļĪ£ 10ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢśņŚ¼ CO ņł£ņ£äĻ░Ć Ļ░Ćņן ļé«ņØĆ 10%ņŚÉ Low 1ņØä ļČĆņŚ¼ĒĢśĻ│Ā, Ļ░Ćņן ļåÆņØĆ 10%ņŚÉ High 10ņØä ļČĆņŚ¼ĒĢ£ļŗż. COņĀäļץņØś ņłśņØĄņä▒ņØä ĒÖĢņØĖĒĢśĻĖ░ ņ£äĒĢśņŚ¼ Ēł¼ņ×Éņ×ÉņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØ┤ ĻĘ╣ļŗ©ņĀüņ£╝ļĪ£ ļéśĒāĆļéśļŖö Low 1Ļ│╝ High 10ņŚÉ ņ┤łņĀÉņØä ļ¦×ņČśļŗż. Ļ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö ņ░©ĒøäKĻ░£ņøö(t+1ņøöļČĆĒä░t+Kņøö)ļÅÖņĢł ļ│┤ņ£ĀĒĢ£ļŗż. Jegadeesh(1990)ņŚÉ ļö░ļØ╝ ņøöļ│äņŻ╝ņŗØ ņłśņØĄļźĀņØś ņØīņØś ņ×ÉĻĖ░ņāüĻ┤Ć ĒÜ©Ļ│╝ļź╝ ņżäņØ┤ĻĖ░ ņ£äĒĢ┤ tņøöņØś ņøöļ│äņłśņØĄļźĀĻ│╝ Ļ▒░ļלļīĆĻĖłņØä ņĀ£ņÖĖĒĢśļ®░, ĒżĒŖĖ ĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░ä(formation period, J)ņÖĆ ļ│┤ņ£ĀĻĖ░Ļ░ä(holding period, K) ņé¼ņØ┤ņŚÉ 1Ļ░£ņøöņØś Ļ░äĻ▓®ņØä ļæöļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ KĻ░£ņøöņØĖ ņżæļ│Ą ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉņä£tņøöņØś ņøöļ│äņłśņØĄļźĀņØĆt-KņøöļČĆĒä░t-1ņøöņŚÉ ĻĄ¼ņä▒ļÉ£ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņøöļ│äņłśņØĄļźĀļĪ£ ĻĄ¼ņä▒ļÉ£ļŗż. ļŗżņŗ£ ļ¦ÉĒĢ┤, ļ¦żtņøöņŚÉņä£ļŖöt-KĻ░£ņøö ņØ┤ņĀäļ┐Éļ¦ī ņĢäļŗłļØ╝ ņĀäņøöņŚÉ ņäĀĒāØļÉ£ ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļ│┤ņ£ĀĒĢśĻ▓ī ļÉ£ļŗż. ņØ┤ļ¤¼ĒĢ£ ņżæļ│Ą ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ļ░®ļ▓ĢņØĆ <ĻĘĖļ”╝ 1>ņŚÉ ņ×ÉņäĖĒ׳ ļéśĒāĆļéĖļŗż.

<ĻĘĖļ”╝┬Ā1>

ņżæļ│Ą ĒżĒŖĖĒÅ┤ļ”¼ņśż(overlapping portfolio)ĻĄ¼ņä▒ ļ░®ļ▓Ģ

ņØ┤ ĻĘĖļ”╝ņØĆ Jegadeesh and Titman(1993)ņŚÉ ļö░ļźĖ ņżæļ│Ą ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ļ░®ļ▓ĢņØ┤ļŗż. ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äņØ┤ 3Ļ░£ņøö(J=3)ņØ┤Ļ│Ā, ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 3Ļ░£ņøö(K=3)ņØ╝ Ļ▓ĮņÜ░ ļŗżņØīĻ│╝ Ļ░ÖņØĆ ļ░®ļ▓Ģņ£╝ļĪ£ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØä ĻĄ¼ņä▒ĒĢ£ļŗż.

<ĻĘĖļ”╝ 1> ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äņØ┤ 3Ļ░£ņøö(J=3)ņØ┤Ļ│Ā, ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 3Ļ░£ņøö(K=3)ņØĖ ņżæļ│Ą ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĄ¼ņä▒ļ░®ļ▓ĢņØ┤ļŗż. ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØĆ ļ¦żņøö Ļ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņŚÉ1/KņØś Ļ░Ćņżæņ╣śļź╝ Ļ│▒ĒĢ£ Ļ░ÆņØś ĒĢ®ņØ┤ļŗż. ņśłļź╝ ļōżņ¢┤, <ĻĘĖļ”╝ 1>ņØśt=3ņØ╝ ļĢī ņłśņØĄļźĀņØĆ ņ▓½ ļ▓łņ¦Ė ĻĄ¼ņä▒ļÉ£ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņäĖ ļ▓łņ¦Ė ļŗ¼ņØś ņłśņØĄļźĀĻ│╝ ļæÉ ļ▓łņ¦Ė ĻĄ¼ņä▒ļÉ£ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ļæÉ ļ▓łņ¦Ė ļŗ¼ņØś ņłśņØĄļźĀ, ņäĖ ļ▓łņ¦Ė ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņ▓½ ļ▓łņ¦Ė ļŗ¼ņØś ņłśņØĄļźĀņØś ĒĢ®ņØäK=3ņ£╝ļĪ£ ļéśļłł Ļ░ÆņØ┤ ļÉ£ļŗż. ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äņØä 12Ļ░£ņøöļĪ£ ņäżņĀĢĒĢśĻ│Ā, ļ│┤ņ£ĀĻĖ░Ļ░äņØĆ 6Ļ░£ņøö, 9Ļ░£ņøö ĻĘĖļ”¼Ļ│Ā 12Ļ░£ņøöļĪ£ ļéśļłäņ¢┤ ņ¦äĒ¢ēĒĢ£ļŗż.

3.4.2 ļŗżļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśż

ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö ņŻ╝ņŗØņłśņØĄļźĀĻ│╝ COņØś Ļ┤ĆĻ│äņŚÉņä£ ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØś ņśüĒ¢źņØä ļ░░ņĀ£ĒĢśĻĖ░ ņ£äĒĢśņŚ¼ ļŗżļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśż ļČäņäØņØä ĒĢ£ļŗż. ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ļ░®ļ▓ĢņØĆ ļŗżņØīĻ│╝ Ļ░Öļŗż. ļ¦żtņøö ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØä ĻĖ░ņżĆņ£╝ļĪ£ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļĪ£ ļéśļłłļŗż. Ļ░ü ĻĖ░ņŚģĒŖ╣ņä▒ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØä ļīĆņāüņ£╝ļĪ£ ļŗżņŗ£ COņŚÉ ļö░ļØ╝ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļĪ£ ļéśļłäņ¢┤ 25Ļ░£(5├Ś5)ņØś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢ£ļŗż. Ļ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØĆ ņ░©Ēøä KĻ░£ņøö(t+1ņøöļČĆĒä░t+Kņøö)ļÅÖņĢł ļ│┤ņ£ĀĒĢ£ļŗż. ņżæļ│Ą ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĄ¼ņä▒ņØĆ <ĻĘĖļ”╝ 1>Ļ│╝ ļÅÖņØ╝ĒĢśļŗż. ņ£äņØś ļ░®ļ▓ĢņØä ĒåĄĒĢśņŚ¼ ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØä ĒåĄņĀ£ĒĢ£ Ēøä ņŻ╝ņŗØņłśņØĄļźĀĻ│╝ COņØś Ļ┤ĆĻ│äļź╝ ņĪ░ņé¼ĒĢ£ļŗż. ļŗżļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśż ļČäņäØĻ▓░Ļ│╝ļŖö ļ¬©ļōĀ ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØä ĒżĒĢ©ĒĢśĻĖ░ ņ£äĒĢ┤ Ļ░ü ĻĖ░ņŚģĒŖ╣ņä▒ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ Ļ▒Ėņ╣£ CO ĒżĒŖĖĒÅ┤ļ”¼ņśż ĒÅēĻĘĀņłśņØĄļźĀņØä ņĀ£ņŗ£ĒĢ£ļŗż.

4.ŌĆģņŗżņ”ØĻ▓░Ļ│╝

4.1 ļŗ©ļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśż ļČäņäØ

<Ēæ£ 2>ļŖö CO ĻĖ░ļ░ś ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØ┤ļŗż. ĒżĒŖĖĒÅ┤ļ”¼ņśż 1(Low 1)ņØĆ Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ņøöļ│ä ņłśņØĄļźĀĻ│╝ ņøöļ│äĻ▒░ļלļīĆĻĖłņ£╝ļĪ£ ļÅäņČ£ĒĢ£ COĻ░Ć Ļ░Ćņן ļé«ņØĆ ĻĘĖļŻ╣ņØ┤Ļ│Ā, ĒżĒŖĖĒÅ┤ļ”¼ņśż 10(High 10)ņØĆ COĻ░Ć Ļ░Ćņן ļåÆņØĆ ĻĘĖļŻ╣ņØ┤ļŗż. COĻ░Ć Ļ░Ćņן ļé«ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż 1ņØĆ ņØīņØś ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ Ēł¼ņ×Éņ×ÉņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ļéśĒāĆļé┤Ļ│Ā, ĒżĒŖĖĒÅ┤ļ”¼ņśż 10ņØĆ ņ¢æņØś ņĀĢļ│┤ņŚÉ ļīĆĒĢ£ Ēł¼ņ×Éņ×ÉņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ļéśĒāĆļéĖļŗż. COļŖö ņŗØ (2)ņŚÉ ņØśĒĢśņŚ¼ Ļ│╝Ļ▒░ 12Ļ░£ņøö(t-12ņøöļČĆĒä░t-1ņøö)ņØś ņøöļ│äņłśņØĄļźĀĻ│╝ ņøöļ│äĻ▒░ļלļīĆĻĖłņ£╝ļĪ£ ļÅäņČ£ĒĢ£ļŗż. Ļ░ü ņŚ┤ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ ņØ┤Ēøä ļ│┤ņ£ĀĻĖ░Ļ░ä(K)ņØ┤ 6Ļ░£ņøö, 9Ļ░£ņøö, ĻĘĖļ”¼Ļ│Ā 12Ļ░£ņøöņØĖ ņżæļ│Ą ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØ┤ļŗż. ņżæļ│Ą ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ļ░®ļ▓ĢņØĆ <ĻĘĖļ”╝ 1>Ļ│╝ Ļ░Öļŗż. High-LowļŖö COĻ░Ć Ļ░Ćņן ļåÆņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļ¦żņ×ģĒĢśĻ│Ā, COĻ░Ć Ļ░Ćņן ļé«ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļ¦żļÅäĒĢśļŖö ņĀäļץņØĖ ļ¼┤ļ╣äņÜ® ĒżĒŖĖĒÅ┤ļ”¼ņśż(zero-cost investment)ņØś ņłśņØĄļźĀņØ┤ļŗż. CAPM ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØĆ ņŗØ (3)ņØś╬▒ņØ┤Ļ│Ā, FF3 ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØĆ Fama and French(1993)ņØś 3ņÜöņØĖņ£╝ļĪ£ ņ£äĒŚśņØ┤ ņĪ░ņĀĢļÉ£ ņłśņØĄļźĀļĪ£ ņŗØ (6)ņØś╬▒ņØ┤ļŗż. Ļ┤äĒśĖ ņĢłņØĆ Newey and West(1987)ņØś t-ĒåĄĻ│äļ¤ēņØä ļéśĒāĆļéĖļŗż.

<Ēæ£┬Ā2>

CO ĻĖ░ļ░ś ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀ

ļ¦żņøö ļ¦É COļź╝ ĻĖ░ņżĆņ£╝ļĪ£ ĻĄ¼ņä▒ĒĢ£ 10Ļ░£ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØ┤ļŗż. ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äņØĆ 12Ļ░£ņøö(J=12)ņØ┤ļ®░, Ļ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ 6Ļ░£ņøö, 9Ļ░£ņøö, ĻĘĖļ”¼Ļ│Ā 12Ļ░£ņøö ļ│┤ņ£ĀĒĢ£ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØ┤ļŗż. CAPMņØĆ ņŗ£ņןņÜöņØĖņ£╝ļĪ£ ņ£äĒŚśņØä ņĪ░ņĀĢĒĢ£ ņłśņØĄļźĀņØ┤Ļ│Ā, FF3ņØĆ Fama and French(1993)ņØś 3ņÜöņØĖņ£╝ļĪ£ ņ£äĒŚśņØä ņĪ░ņĀĢĒĢ£ ņłśņØĄļźĀņØ┤ļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØĆ Ļ░üĻ░ü 6Ļ░£ņøö(K=6), 9Ļ░£ņøö(K=9), 12Ļ░£ņøö(K=12)ņØ┤ļŗż. ņłśņØĄļźĀņØĆ ĒŹ╝ņä╝ĒŖĖ ļŗ©ņ£äļŗż. Ēæ£ļ│ĖņØĆ 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņןĻ│╝ ņĮöņŖżļŗźņŗ£ņןņŚÉ ņāüņןļÉ£ ļ│┤ĒåĄņŻ╝ ņżæņŚÉņä£ ņŻ╝ļŗ╣ Ļ░ĆĻ▓®ņØ┤ 500ņøÉļ│┤ļŗż Ēü░ ņŻ╝ņŗØņØ┤ļŗż. ***, **, *ļŖö Ļ░üĻ░ü 1%, 5%, 10% ņ£ĀņØśņłśņżĆņŚÉņä£ ņ£ĀņØśĒĢ©ņØä Ēæ£ņŗ£ĒĢ£ļŗż. Ļ┤äĒśĖ ņĢłņØś ņł½ņ×ÉļŖö Newey and West(1987) t-ĒåĄĻ│äļ¤ēņØ┤ļŗż.

<Ēæ£ 2>ņØś Ļ▓░Ļ│╝ļŖö COņÖĆ ņŻ╝ņŗØņłśņØĄļźĀĻ░äņØś ņ¢æņØś Ļ┤ĆĻ│äļź╝ ļéśĒāĆļéĖļŗż. ņØīņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä Ļ░Ćņ¦ĆļŖö ĒżĒŖĖĒÅ┤ļ”¼ņśż(Low 1)ļŖö ļŗżļźĖ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ļ╣äĒĢśņŚ¼ ņāüļīĆņĀüņ£╝ļĪ£ ļé«ņØĆ ņłśņØĄļźĀņØä, ņ¢æņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä Ļ░Ćņ¦ĆļŖö ĒżĒŖĖĒÅ┤ļ”¼ņśż(High 10)ļŖö ņāüļīĆņĀüņ£╝ļĪ£ ļåÆņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 6Ļ░£ņøö, 9Ļ░£ņøö, ĻĘĖļ”¼Ļ│Ā 12Ļ░£ņøöņØ╝ ļĢī ļ¼┤ļ╣äņÜ® ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØĆ 0.837%, 0.806%, 0.603%ņØ┤ļ®░ ĒåĄĻ│äņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢśļŗż. COņĀäļץņØś ņŚ░Ļ░ä ņłśņØĄļźĀņØĆ 7%ņŚÉņä£ 10% ņé¼ņØ┤ņØ┤ļŗż. ļö░ļØ╝ņä£ Ļ│äņåŹņĀü Ļ│╝ņ×ē ļ░śņØæņØä ĒåĄĒĢśņŚ¼ ņłśņØĄņä▒ ņ׳ļŖö ļ¦żņ×ģ-ļ¦żņłś Ļ▒░ļלņĀäļץņØä ĻĄ¼ĒśäĒĢĀ ņłś ņ׳ņØīņØä ņĀ£ņŗ£ĒĢ£ļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 6Ļ░£ņøöņØĖ Ļ▓ĮņÜ░ņŚÉ ņłśņØĄļźĀņØ┤ Ļ░Ćņן ļåÆņ£╝ļ®░, ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 9Ļ░£ņøöņØ╝ ļĢī Ļ░Ćņן ļåÆņØĆ t-ĒåĄĻ│äļ¤ēņØä Ļ░Ćņ¦äļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 12Ļ░£ņøöņØĖ Ļ▓ĮņÜ░ņŚÉļÅä ņŚ¼ņĀäĒ׳ ĒåĄĻ│äņĀüņ£╝ļĪ£ļéś Ļ▓ĮņĀ£ņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż.

<Ēæ£ 2>ņØś CAPM ņ£äĒŚśņĪ░ņĀĢņłśņØĄļźĀņØĆ ņŗØ (3)ņŚÉ ļö░ļØ╝ ņ£äĒŚśņØä ņĪ░ņĀĢĒĢ£ ņłśņØĄļźĀņØ┤ļŗż. CAPM ļ¼┤ļ╣äņÜ® ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö Ļ░ü ļ│┤ņ£ĀĻĖ░Ļ░äņŚÉ ļö░ļØ╝ 0.804%, 0.789%, 0.601%ņØ┤ļ®░, ļ¬©ļōĀ ĻĖ░Ļ░äņŚÉņä£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļŗż. FF3 ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØĆ Fama and French(1993)ņØś 3ņÜöņØĖ ļ¬©ĒśĢņØĖ ņŗ£ņןņÜöņØĖ, ĻĘ£ļ¬©ņÜöņØĖ (SMB), Ļ░Ćņ╣śņÜöņØĖ(HML)ņ£╝ļĪ£ ņ£äĒŚśņØä ņĪ░ņĀĢĒĢ£ ņĢīĒīīņØ┤ļŗż. ņØ┤ļź╝ ĒåĄĒĢ┤ COņĀäļץņØ┤ ļŗ©ņ¦Ć ņ£äĒŚśļČĆļŗ┤ņŚÉ ļīĆĒĢ£ ļ│┤ņāüņØĖņ¦Ć ņŚ¼ļČĆļź╝ Ļ▓ĆĒåĀĒĢĀ ņłś ņ׳ļŗż. FF3 ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØĆ ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 6Ļ░£ņøö, 9Ļ░£ņøö, 12Ļ░£ņøöņØ╝ ļĢī Ļ░üĻ░ü 0.208%, 0.333%, 0.231%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļŗż. ļö░ļØ╝ņä£ Fama and French(1993)ņØś 3ņÜöņØĖ ļ¬©ĒśĢņ£╝ļĪ£ ņ£äĒŚśņØä ņĪ░ņĀĢĒĢśņŚ¼ļÅä CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ļ¦żņłś-ļ¦żņ×ģņĀäļץņŚÉ ņłśņØĄņä▒ņØ┤ ņ׳ņØīņØä ĒÖĢņØĖĒĢ£ļŗż.

ņÜöņĢĮĒĢśļ®┤, ļ¦żņøö ļ¦É COļź╝ ĻĖ░ņżĆņ£╝ļĪ£ 10ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢśĻ│Ā Ļ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØä KĻ░£ņøö ļ│┤ņ£ĀĒĢ£ Ļ▓░Ļ│╝, ļ¼┤ļ╣äņÜ® ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. CAPM, FF3 ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀļÅä ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ņ£äĒŚś ņÜöņØĖņØä ņČöĻ░ĆĒĢĀņłśļĪØ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØĆ Ļ░ÉņåīĒĢśļŖö Ļ▓ĮĒ¢źņØ┤ ņ׳ņ£╝ļéś, ļ¬©ļōĀ ņłśņØĄļźĀņØ┤ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØĖ Ļ▓āņØä ĒÖĢņØĖĒĢ£ļŗż. ļö░ļØ╝ņä£ ņÜ░ļ”¼ļŖö COņÖĆ ņŻ╝ņŗØņłśņØĄļźĀņØĆ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ┤ĆĻ│äņŚÉ ņ׳Ļ│Ā, COņĀäļץņØ┤ ņłśņØĄņä▒ņØä Ļ░Ćņ¦äļŗżļŖö ņé¼ņŗżņØä ĒÖĢņØĖĒĢ£ļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 6Ļ░£ņøö (K=6)ņØ╝ Ļ▓ĮņÜ░ņŚÉ ņłśņØĄļźĀņØ┤ Ļ░Ćņן ļåÆņ£╝ļ»ĆļĪ£ ņØ┤Ēøä ĒżĒŖĖĒÅ┤ļ”¼ņśż ņĀäļץņØś Ļ▓░Ļ│╝ļŖö ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 6Ļ░£ņøöņØĖ Ļ▓ĮņÜ░ļ¦ī ļéśĒāĆļéĖļŗż.

4.2 ļ¬©ļ®śĒģĆĻ│╝ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ

Jegadeesh and Titman(1993)ņØś ļ¬©ļ®śĒģĆ ņØ┤ņāüĒśäņāüņØĆ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ Ļ░Ćņן ņ£Āļ¬ģĒĢ£ ņØ┤ņāüņłśņØĄļźĀ Ēśäņāü ņżæ ĒĢśļéśļŗż. Rouwenhorst(1998)ņŚÉ ļö░ļź┤ļ®┤ 1980ļģäĻ│╝ 1995ļģä ņé¼ņØ┤ņŚÉ ļ¬©ļ®śĒģĆ ņĀäļץņØĆ ņłśņØĄņä▒ņØä Ļ░Ćņ¦Ćļ®░ 12Ļ░£ ĻĄŁĻ░ĆņŚÉņä£ ņØ╝Ļ┤ĆļÉśĻ│Ā ĒÅēĻĘĀ 1ļģäĻ░ä ņ¦ĆņåŹņĀüņØĖ ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. Griffin et al.(2003)ņØĆ Ļ▒░ņŗ£ Ļ▓ĮņĀ£ņĀü ņ£äĒŚśņØ┤ ļ¬©ļ®śĒģĆ ņĀäļץņØś ņØ┤ņØĄņØä ņäżļ¬ģĒĢĀ ņłś ņ׳ļŖöņ¦Ć ņŚ¼ļČĆļź╝ Ļ▓ĆĒåĀĒĢśĻ│Ā, ļ¬©ļ®śĒģĆ ņĀäļץņØ┤ ĻĄŁņĀ£ņŗ£ņןņŚÉņä£ ņāüļŗ╣ĒĢ£ ņ¢æņØś ņØ┤ņØĄņØä ņ░ĮņČ£ĒĢ©ņØä ļ│┤ņØĖļŗż. ļ░śļ®┤, ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ļŖö ļ¬©ļ®śĒģĆņŚÉ ļīĆĒĢ£ Ļ▓░Ļ│╝Ļ░Ć ņāüņØ┤ĒĢśĻ▓ī ļéśĒāĆļé£ļŗż. Kam and Shin(2011)ņŚÉ ļö░ļź┤ļ®┤ ņŻ╝Ļ░Ć ļ¬©ļ®śĒģĆņŚÉ ļö░ļØ╝ ĻĄ¼ņä▒ļÉ£ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉņä£ Ēī©ņ×ÉĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØ┤ ņŖ╣ņ×ÉĒżĒŖĖĒÅ┤ļ”¼ņśżļ│┤ļŗż ļåÆļŗż. ņØ┤ļŖö ņŚŁĒ¢ēĒł¼ņ×ÉņĀäļץ (constrain investment strategy)ņØś ņä▒Ļ│╝ņŚÉņä£ ņ£ĀņØśĒĢ£ ņ¢æ(+)ņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ÉņØä ņØśļ»ĖĒĢ£ļŗż. Jang(2017)ņØĆ Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ĻĖ░Ļ░äņØä Ļ│╝Ļ▒░ 6Ļ░£ņøöņØä ĻĖ░ņżĆņ£╝ļĪ£ ļéśļłäņ¢┤ ļ¬©ļ®śĒģĆ ĒÜ©Ļ│╝ļź╝ ļČäņäØĒĢ£ļŗż. ĻĘĖ Ļ▓░Ļ│╝ ņżæĻĖ░ Ļ│╝Ļ▒░ 6Ļ░£ņøöņØś ņŖ╣ņ×Éļź╝ ļ¦żņłśĒĢśĻ│Ā Ēī©ņ×Éļź╝ ļ¦żļÅäĒĢśļŖö ņĀäļץņŚÉņä£ 1.51% ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. Eom(2013)ņŚÉ ļö░ļź┤ļ®┤ ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ņĀäļ░śņĀüņ£╝ļĪ£ ļ¬©ļ®śĒģĆņØ┤ ņĪ┤ņ×¼ĒĢśņ¦Ć ņĢŖļŖöļŗż. ļČäņäØņóģļ¬®Ļ│╝ ĻĖ░Ļ░äņØä ņäĖļČĆņĀüņ£╝ļĪ£ ļéśļłäņ¢┤ ļČäņäØĒĢ£ Ļ▓░Ļ│╝, ņÖĖĒÖśņ£äĻĖ░ ņØ┤ņĀäņŚÉļŖö ņØīņØś ļ¬©ļ®śĒģĆņØ┤ ļéśĒāĆļéśĻ│Ā ņÖĖĒÖśņ£äĻĖ░ ņØ┤ĒøäņŚÉļŖö ņ¢æņØś ļ¬©ļ®śĒģĆņØ┤ ņĪ┤ņ×¼ĒĢ©ņØä ĒÖĢņØĖĒĢ£ļŗż.

Daniel et al.(1998)ņŚÉ ļö░ļź┤ļ®┤ Byun et al.(2016)ņŚÉņä£ ņĀ£ņŗ£ĒĢ£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ(CO)ņØĆ ļ¬©ļ®śĒģĆ ņĀäļץņŚÉ ļīĆĒĢ£ ļīĆĒæ£ņĀüņØĖ Ē¢ēļÅÖņäżļ¬ģ ņżæ ĒĢśļéśļŗż. Ļ│╝Ļ▒░ņłśņØĄļźĀņŚÉ ĻĖ░ņ┤łĒĢ£ ņłśņØĄļźĀ ņśłņĖĪņä▒ņØ┤ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņŚÉ ņØśĒĢ£ Ļ▓āņØ┤ļØ╝ļ®┤ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØĆ Ļ│╝Ļ▒░ņłśņØĄļźĀļ│┤ļŗż ļ»ĖļלņłśņØĄļźĀņØä ļŹö ņל ņśłņĖĪĒĢśĻ▓ī ļÉĀ Ļ▓āņØ┤ļŗż. ņØ┤ņŚÉ ļö░ļØ╝ ļ│Ė ņĀłņŚÉņä£ļŖö COņĀäļץĻ│╝ ļ¬©ļ®śĒģĆ ņĀäļץņØś ņłśņØĄņä▒ņØä ļ╣äĻĄÉĒĢ£ļŗż.

ņÜ░ļ”¼ļŖö COņĀäļץĻ│╝ ļ¬©ļ®śĒģĆ ņĀäļץņŚÉ ļö░ļźĖ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØä ļ╣äĻĄÉĒĢ£ļŗż. ņä£ļĪ£ ļŗżļźĖ ņĀäļץņØś ņłśņØĄļźĀņØä ĻĖ░ņżĆ(benchmark)ņ£╝ļĪ£ ņé¼ņÜ®ĒĢśņŚ¼ ĻĖ░ņżĆņŚÉ ņØśĒĢ┤ ņĪ░ņĀĢļÉ£ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØä ĻĖ░ņżĆ ņĪ░ņĀĢņłśņØĄļźĀ(benchmark-adjusted return)ļĪ£ ļéśĒāĆļéĖļŗż. <Ēæ£ 3>ņØś 1-3ņŚ┤ņØĆ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØä ļéśĒāĆļéĖļŗż. ņøöļ│äņłśņØĄļźĀņØĆ COĻ░Ć Ļ░Ćņן ļé«ņØĆ Low 1ļČĆĒä░ Ļ░Ćņן ļåÆņØĆ High 10ņØś ņłśņØĄļźĀņØä ņØśļ»ĖĒĢśĻ│Ā, ļ¬©ļ®śĒģĆ ņĪ░ņĀĢņłśņØĄļźĀņØĆ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØś ņłśņØĄļźĀņŚÉņä£ Ļ░ü ņŻ╝ņŗØņØ┤ ņåŹĒĢ£ ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ļÅÖņØ╝Ļ░Ćņżæ ņłśņØĄļźĀņØä ļ║Ć Ļ░ÆņØ┤ļŗż. <Ēæ£ 3>ņØś 4-6ņŚ┤ņØĆ ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØä ļéśĒāĆļéĖļŗż. ņøöļ│äņłśņØĄļźĀņØĆ ļ¬©ļ®śĒģĆņØ┤ Ļ░Ćņן ļé«ņØĆ Low 1ļČĆĒä░ Ļ░Ćņן ļåÆņØĆ High 10ņØś ņłśņØĄļźĀņØä ņØśļ»ĖĒĢśĻ│Ā, COņĪ░ņĀĢ ņłśņØĄļźĀņØĆ ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØś ņłśņØĄļźĀņŚÉņä£ Ļ░ü ņŻ╝ņŗØņØ┤ ņåŹĒĢ£ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ļÅÖņØ╝Ļ░Ćņżæ ņłśņØĄļźĀņØä Ļ░ÉĒĢ£ Ļ░ÆņØ┤ļŗż.

<Ēæ£┬Ā3>

CO, ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀ

ņØ┤ Ēæ£ļŖö ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 6Ļ░£ņøö(K=6)ņØĖ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņÖĆ ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀ Ļ▓░Ļ│╝ļŗż. ļ¬©ļ®śĒģĆ(CO)ņĪ░ņĀĢ ņłśņØĄļźĀņØĆ ļ¦żņøö ļ¦É CO(ļ¬©ļ®śĒģĆ)ļź╝ ĻĖ░ņżĆņ£╝ļĪ£ ĻĄ¼ņä▒ļÉ£ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņŚÉņä£ ĻĘĖ ņŻ╝ņŗØņØ┤ ņåŹĒĢ£ ļ¬©ļ®śĒģĆ(CO) 10ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØä Ļ░ÉĒĢ£ Ļ░ÆņØ┤ļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØĆ 6Ļ░£ņøö(K=6)ņØ┤Ļ│Ā, ņłśņØĄļźĀņØĆ ĒŹ╝ņä╝ĒŖĖ ļŗ©ņ£äļŗż. Ēæ£ļ│ĖņØĆ 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņןĻ│╝ ņĮöņŖżļŗźņŗ£ņןņŚÉ ņāüņןļÉ£ ļ│┤ĒåĄņŻ╝ ņżæņŚÉņä£ ņŻ╝ļŗ╣ Ļ░ĆĻ▓®ņØ┤ 500ņøÉļ│┤ļŗż Ēü░ ņŻ╝ņŗØņØ┤ļŗż. ***, **, *ļŖö Ļ░üĻ░ü 1%, 5%, 10% ņ£ĀņØśņłśņżĆņŚÉņä£ ņ£ĀņØśĒĢ©ņØä Ēæ£ņŗ£ĒĢ£ļŗż. Ļ┤äĒśĖ ņĢłņØś ņł½ņ×ÉļŖö Newey and West(1987) t-ĒåĄĻ│äļ¤ēņØ┤ļŗż.

<Ēæ£ 3>ņŚÉ ļö░ļź┤ļ®┤, CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØĆ 0.837%, ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØĆ 1.027% ņØ┤ļŗż. t-ĒåĄĻ│äļ¤ēņØä ļ╣äĻĄÉĒĢśļ®┤ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņÖĆ ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö Ļ░üĻ░ü 4.374ņÖĆ 3.155ļĪ£ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżĻ░Ć ļŹö ļåÆļŗż. ņ”ē, COņĀäļץņØ┤ ļŹö ļåÆņØĆ ņāżĒöäļ╣äņ£©(sharpe ratio)ņØä Ļ░Ćņ¦äļŗż. CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś Ļ▓ĮņÜ░ COĻ░Ć ņ”ØĻ░ĆĒĢ©ņŚÉ ļö░ļØ╝ ņłśņØĄļźĀņØ┤ ļŗ©ņĪ░ļĪŁĻ▓ī ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦Ćņ¦Ćļ¦ī, ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś Ļ▓ĮņÜ░ ĒżĒŖĖĒÅ┤ļ”¼ņśż 7ļČĆĒä░ ĒżĒŖĖĒÅ┤ļ”¼ņśż 10ņŚÉ Ļ▒Ėņ│É ĒĢśļØĮĒĢśļŖö ņČöņäĖļź╝ Ļ░Ćņ¦äļŗż. <Ēæ£ 3>ņŚÉņä£ ņżæņÜöĒĢ£ Ļ▓āņØĆ ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØ┤ļŗż. CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØś ņ░©ņØ┤ļŖö 0.500%ņØ┤Ļ│Ā, ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØś ņ░©ņØ┤ļŖö 0.681%ņØ┤ļŗż. CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀĻ│╝ ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØĆ ļ¬©ļæÉ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ĒĢśņ¦Ćļ¦ī, ļæÉ ĒżĒŖĖ ĒÅ┤ļ”¼ņśżņØś Ēī©Ēä┤ņØĆ ļåĆļØ╝ņÜĖ ņĀĢļÅäļĪ£ ļŗżļź┤ļŗż. CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØĆ COĻ░Ć ļåÆņØīņŚÉ ļö░ļØ╝ ļŗ©ņĪ░ļĪŁĻ▓ī ņāüņŖ╣ĒĢśļŖö ņłśņØĄļźĀņØĆ Ļ░Ćņ¦ĆļŖö ļ░śļ®┤, ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØĆ ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦Ćņ¦Ć ņĢŖĻ│Ā ĒżĒŖĖĒÅ┤ļ”¼ņśż 7ņŚÉņä£ļČĆĒä░ ĒĢśļØĮĒĢśļŖö ņČöņäĖļź╝ Ļ░Ćņ¦äļŗż. ļśÉĒĢ£, CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØ┤ ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀļ│┤ļŗż ļåÆņØĆ t-ĒåĄĻ│äļ¤ēņØä Ļ░Ćņ¦äļŗż.

ņÜ░ļ”¼ļŖö ņ£äņØś Ļ▓░Ļ│╝ļź╝ Ēæ£ļ│ĖĻĖ░Ļ░äņØä ļéśļłäņ¢┤ ņ×¼ĒÖĢņØĖĒĢ£ļŗż. <ĻĘĖļ”╝ 2>ļŖö 2000ļģäļČĆĒä░ 2010ļģäĻ│╝ 2011ļģäļČĆĒä░ 2020ļģäņØś CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņÖĆ ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØä ļ╣äĻĄÉĒĢ£ļŗż. <ĻĘĖļ”╝ 2>ņØś ĻĘĖļŻ╣ AļŖö 2000ļģäļČĆĒä░ 2010ļģäĻ╣īņ¦ĆņØś ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀĻ│╝ 2011ļģäļČĆĒä░ 2020ļģäĻ╣īņ¦ĆņØś ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØä ļéśĒāĆļéĖļŗż. CO ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö COĻ░Ć ņ”ØĻ░ĆĒĢ©ņŚÉ ļö░ļØ╝ ņłśņØĄļźĀņØ┤ ļŗ©ņĪ░ļĪŁĻ▓ī ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦äļŗż. ĒĢśņ¦Ćļ¦ī, ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö ļÜ£ļĀĘĒĢ£ Ēī©Ēä┤ņØä ļéśĒāĆļé┤ņ¦Ć ņĢŖļŖöļŗż. ĻĘĖļŻ╣ BļŖö 2000ļģäļČĆĒä░ 2010ļģäĻ│╝ 2011ļģäļČĆĒä░ 2020ļģäņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØä ļéśĒāĆļéĖļŗż. ĻĘĖļŻ╣ AņÖĆ ņ£Āņé¼ĒĢśĻ▓ī, CO ĒżĒŖĖ ĒÅ┤ļ”¼ņśżļŖö COņŚÉ ļö░ļØ╝ ņ”ØĻ░ĆĒĢśļŖö ņłśņØĄļźĀ Ēī©Ēä┤ņØä ĒÖĢņØĖĒĢĀ ņłś ņ׳ņ¦Ćļ¦ī, ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦Ćņ¦Ć ņĢŖļŖöļŗż. 2011ļģäļČĆĒä░ 2020ļģäņØś Ļ▓░Ļ│╝ņŚÉņä£ ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż 10ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż 1Ļ│╝ ņ£Āņé¼ĒĢ£ ņłśņØĄļźĀņØä Ļ░Ćņ¦Ćļ»ĆļĪ£ ļ¬©ļ®śĒģĆ ņĀäļץņØĆ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦Ćņ¦Ć ļ¬╗ĒĢ£ļŗż.

<ĻĘĖļ”╝┬Ā2>

CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņÖĆ ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ļ╣äĻĄÉ

ņØ┤ ĻĘĖļ”╝ņØĆ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņÖĆ ļ¬©ļ®śĒģĆĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļ╣äĻĄÉĒĢ£ļŗż. ĻĘĖļŻ╣ AļŖö 2000’Į×2010ļģäĻ│╝ 2011’Į×2020ļģäņØś ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØ┤ļ®░, ĻĘĖļŻ╣ BļŖö 2000’Į×2010ļģäĻ│╝ 2011’Į×2020ļģäņØś CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņÖĆ ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØä ļéśĒāĆļéĖļŗż. ņłśņØĄļźĀņØĆ ĒŹ╝ņä╝ĒŖĖ ļŗ©ņ£äļŗż. Ēæ£ļ│ĖņØĆ 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ņ£ĀĻ░Ćņ”ØĻČī ņŗ£ņןĻ│╝ ņĮöņŖżļŗźņŗ£ņןņŚÉ ņāüņןļÉ£ ļ│┤ĒåĄņŻ╝ ņżæņŚÉņä£ ņŻ╝ļŗ╣ Ļ░ĆĻ▓®ņØ┤ 500ņøÉļ│┤ļŗż Ēü░ ņŻ╝ņŗØņØ┤ļŗż.

ņĀĢļ”¼ĒĢśļ®┤, Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äņØä Ļ░Ćņ¦ĆĻ│Ā ļÅÖņØ╝ĒĢ£ ļ│┤ņ£ĀĻĖ░Ļ░äņØä Ļ░Ćņ¦ĆļŖö ļ¬©ļ®śĒģĆ ņĀäļץĻ│╝ COņĀäļץņØĆ ļ¬©ļæÉ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. COļź╝ ņĪ░ņĀĢĒĢ£ ļ¬©ļ®śĒģĆņĀäļץņØĆ ļÜ£ļĀĘĒĢ£ Ēī©Ēä┤ņØä Ļ░Ćņ¦Ćņ¦Ć ņĢŖņ¦Ćļ¦ī, ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ļ¬©ļ®śĒģĆņ£╝ļĪ£ ņĪ░ņĀĢĒĢ£ COņĀäļץņØĆ ņŚ¼ņĀäĒ׳ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ļö░ļØ╝ņä£ COņĀäļץņØś ņłśņØĄļźĀņØĆ ļ¬©ļ®śĒģĆ ņĀäļץņŚÉ ņØśĒĢ£ ĻĖ░ņØĖĒĢ£ Ļ▓āņØ┤ ņĢäļŗłļ®░ ļ¬©ļ®śĒģĆņĀäļץņØĆ COņ£╝ļĪ£ ņØĖĒĢ┤ ņłśņØĄļźĀĻ│╝ ņ£ĀņØśļÅäĻ░Ć ļé«ņĢäņ¦ÉņØä ĒÖĢņØĖĒĢ£ļŗż.

4.3 ļŗżļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśż ļČäņäØ

ļ│Ė ņĀłņŚÉņä£ļŖö ņŗ£ņןļ▓ĀĒāĆ(BETA), ĻĖ░ņŚģĻĘ£ļ¬©(SIZE), ņןļČĆĻ░Ćņ╣ś ļīĆ ņŗ£ņןĻ░Ćņ╣ś(BEME), Ļ│╝Ļ▒░ņłśņØĄļźĀ (PRET), ļŗ©ĻĖ░ņłśņØĄļźĀļ░śņĀä(REV), ņ£ĀļÅÖņä▒(ILLIQ), Ļ│Āņ£Āļ│ĆļÅÖņä▒(IVOL), Ļ▒░ļלļ¤ēĒÜīņĀäņ£©(TURN)ņØä ĒåĄņĀ£ĒĢ£ Ēøä, Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ│╝ ņŻ╝ņŗØņłśņØĄļźĀņØś Ļ┤ĆĻ│äļź╝ Ļ▓ĆĒåĀĒĢ£ļŗż. ļ©╝ņĀĆ, ņŗ£ņןļ▓ĀĒāĆ(BETA)ļź╝ ĻĖ░ņżĆņ£╝ļĪ£ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢ£ļŗż. Ļ░ü ņŗ£ņןļ▓ĀĒāĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż ļé┤ņŚÉņä£ ļŗżņŗ£ COļź╝ ĻĖ░ņżĆņ£╝ļĪ£ Ļ░Ćņן ļé«ņØĆ Low 1ļČĆĒä░ Ļ░Ćņן ļåÆņØĆ High 5Ļ╣īņ¦Ć ņł£ņ£äļź╝ ļ¦żĻ▓© 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļĪ£ ļéśļłłļŗż. Ļ░äĻ▓░ņä▒ņØä ņ£äĒĢ┤ 25Ļ░£(5├Ś5)ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļ¬©ļæÉ ļ│┤Ļ│ĀĒĢśņ¦Ć ņĢŖĻ│Ā, Ļ░ü ņŗ£ņןļ▓ĀĒāĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ Low 1(CO) ļČĆĒä░ High 5(CO)Ļ╣īņ¦ĆņØś ĒÅēĻĘĀņłśņØĄļźĀņØä ņĀ£ņŗ£ĒĢ£ļŗż. ļŗżņŗ£ ļ¦ÉĒĢ┤, ņŗ£ņןļ▓ĀĒāĆ(BETA) ĒżĒŖĖĒÅ┤ļ”¼ņśż Low 1ņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØä ļīĆņāüņ£╝ļĪ£ ļŗżņŗ£ COļź╝ ĻĖ░ņżĆņ£╝ļĪ£ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļéśļłłļŗż. ņŗ£ņןļ▓ĀĒāĆ (BETA)Ļ░Ć Low 1ņØ┤ļ®┤ņä£ COĻ░Ć Low 1ņØĖ ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö B1-C1ņØ┤ ļÉśĻ│Ā, ņŗ£ņןļ▓ĀĒāĆ(BETA)Ļ░Ć Low 1ņØĖ ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö B1-C1ļČĆĒä░ B1-C5Ļ╣īņ¦Ć 5Ļ░£ ĒżĒŖĖĒÅ┤ļ”¼ņśżļĪ£ ļČäļźśļÉ£ļŗż. ņ£äņÖĆ Ļ░ÖņØĆ Ļ│╝ņĀĢņØä BETA 2, ŌĆ”, 5Ļ╣īņ¦Ć ļ░śļ│ĄĒĢśļ®┤ ņ┤Ø 25Ļ░£ņØś ĒżĒŖĖĒÅ┤ļ”¼ņśżĻ░Ć ĻĄ¼ņä▒ļÉ£ļŗż. <Ēæ£ 4>ņŚÉņä£ Low 1ņØĆ Ļ░ü ņŗ£ņןļ▓ĀĒāĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉņä£ COĻ░Ć Low 1ņØĖ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ĒÅēĻĘĀņłśņØĄļźĀņØ┤ļ®░ B1-C1, ŌĆ”, B5-C1ņØś ĒÅēĻĘĀ ņłśņØĄļźĀņØ┤ļŗż. ņØ┤ļ¤¼ĒĢ£ ļ░®ļ▓ĢņØĆ ņ£Āņé¼ĒĢ£ ņŗ£ņןļ▓ĀĒāĆļź╝ Ļ░Ćņ¦ä CO ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢśļ»ĆļĪ£ ņŗ£ņןļ▓ĀĒāĆļź╝ ĒåĄņĀ£ĒĢ£ Ēøä ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆĒĢ£ COņØś ņśüĒ¢źņØä ļéśĒāĆļéĖļŗż. ļŗżļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśż ļČäņäØņŚÉņä£ ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äņØ┤ Ļ│╝Ļ▒░ 12Ļ░£ņøö(J=12)ņØ┤Ļ│Ā ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 6Ļ░£ņøö(K=6)ņØĖ Ļ▓░Ļ│╝ļź╝ ņĀ£ņŗ£ĒĢ£ļŗż.

<Ēæ£┬Ā4>

ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØä ĒåĄņĀ£ŃģŗĒĢ£ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀ

ņØ┤ Ēæ£ļŖö ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØä ĒåĄņĀ£ĒĢ£ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØ┤ļŗż. ļ¦żņøö ļ¦É Ēæ£ļ│Ė ļé┤ ļ¬©ļōĀ ņŻ╝ņŗØņØä ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØä ĻĖ░ņżĆņ£╝ļĪ£ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļéśļłäĻ│Ā, Ļ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņŻ╝ņŗØņØä COļĪ£ ļŗżņŗ£ ņĀĢļĀ¼ĒĢśņŚ¼ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļ¦īļōĀļŗż. 25Ļ░£ņØś ĒżĒŖĖĒÅ┤ļ”¼ņśż ņżæņŚÉņä£ Ļ░ü ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØä ĒÅēĻĘĀĒĢśņŚ¼ ĻĄ¼ņä▒ĒĢ£ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś Ļ▓░Ļ│╝ļź╝ ļéśĒāĆļéĖļŗż. CAPMņØĆ ņŗ£ņןņÜöņØĖņ£╝ļĪ£ ņ£äĒŚśņØä ņĪ░ņĀĢĒĢ£ ņłśņØĄļźĀņØ┤Ļ│Ā, FF3ņØĆ Fama and French(1993)ņØś 3ņÜöņØĖņ£╝ļĪ£ ņ£äĒŚśņØä ņĪ░ņĀĢĒĢ£ ņłśņØĄļźĀņØ┤ļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØĆ 6Ļ░£ņøö(K=6)ņØ┤Ļ│Ā, ņłśņØĄļźĀņØĆ ĒŹ╝ņä╝ĒŖĖ ļŗ©ņ£äļŗż. Ēæ£ļ│ĖņØĆ 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņןĻ│╝ ņĮöņŖżļŗźņŗ£ņןņŚÉ ņāüņןļÉ£ ļ│┤ĒåĄņŻ╝ ņżæņŚÉņä£ ņŻ╝ļŗ╣ Ļ░ĆĻ▓®ņØ┤ 500ņøÉļ│┤ļŗż Ēü░ ņŻ╝ņŗØņØ┤ļŗż. ***, **, *ļŖö Ļ░üĻ░ü 1%, 5%, 10% ņ£ĀņØśņłśņżĆņŚÉņä£ ņ£ĀņØśĒĢ©ņØä Ēæ£ņŗ£ĒĢ£ļŗż. Ļ┤äĒśĖ ņĢłņØś ņł½ņ×ÉļŖö Newey and West(1987) t-ĒåĄĻ│äļ¤ēņØ┤ļŗż.

ņŗ£ņןļ▓ĀĒāĆ(BETA)ļĪ£ ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢ£ Ļ▓ĮņÜ░, COņĀäļץņØś ņłśņØĄļźĀņØĆ 0.721%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļŗż. CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØĆ COĻ░Ć ņ”ØĻ░ĆĒĢ©ņŚÉ ļö░ļØ╝ ļŗ©ņĪ░ļĪŁĻ▓ī ņ”ØĻ░ĆĒĢ£ļŗż. CAPMņÖĆ FF3 ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØĆ 0.711%, 0.224%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØ┤ļŗż. ļö░ļØ╝ņä£ ņŗ£ņןļ▓ĀĒāĆļŖö COņĀäļץņŚÉ ņ£ĀņØśĒĢ£ ņśüĒ¢źņØä ļ»Ėņ╣śņ¦Ć ļ¬╗ĒĢśļ®░, COņØĆ ņŗ£ņןļ▓ĀĒāĆņØś ņśüĒ¢źņŚÉņä£ ļÅģļ”ĮņĀüņØ┤ļØ╝ļŖö ņé¼ņŗżņØä ĒÖĢņØĖĒĢ£ļŗż.

ĻĖ░ņŚģĻĘ£ļ¬©(SIZE)ļź╝ ĒåĄņĀ£ĒĢ£ Ēøä, COĻ░Ć ļé«ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņÖĆ ļåÆņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņ░©ņØ┤ļŖö 0.695%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØ┤ļŗż. COĻ░Ć ņ”ØĻ░ĆĒĢ©ņŚÉ ļö░ļØ╝ ņłśņØĄļźĀņØ┤ ļŗ©ņĪ░ļĪŁĻ▓ī ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦äļŗż. CAPM, FF3ņŚÉ ļö░ļźĖ ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØĆ Ļ░üĻ░ü 0.700%, 0.273%ļĪ£ ļ¬©ļæÉ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØ┤ļ»ĆļĪ£ COņĀäļץņØ┤ ĻĖ░ņŚģĻĘ£ļ¬©ņŚÉ ĻĖ░ņØĖĒĢśņ¦Ć ņĢŖņØīņØä ĒÖĢņØĖĒĢ£ļŗż. ļŗżņŗ£ ļ¦ÉĒĢ┤, ĻĖ░ņŚģĻĘ£ļ¬©ļŖö COĻ░Ć ļåÆņØĆ(ļé«ņØĆ) ņŻ╝ņŗØņØ╝ņłśļĪØ ļåÆņØĆ(ļé«ņØĆ) ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ĒśäņāüņØä ņäżļ¬ģĒĢśņ¦Ć ņĢŖļŖöļŗż.

ņןļČĆĻ░Ćņ╣ś ļīĆ ņŗ£ņןĻ░Ćņ╣ś(BEME)ļź╝ ĒåĄņĀ£ĒĢ£ Ēøä Ļ▓░Ļ│╝ļÅä ņ£äņÖĆ ņ£Āņé¼ĒĢśļŗż. <Ēæ£ 4>ņŚÉ ļö░ļź┤ļ®┤ BEMEļź╝ ĒåĄņĀ£ĒĢ£ Ēøä CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØĆ ļŗ©ņĪ░ļĪŁĻ▓ī ņ”ØĻ░ĆĒĢ£ļŗż. ļ¼┤ļ╣äņÜ® ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØĆ 0.498%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļŗż. ļśÉĒĢ£, CAPM, FF3ņŚÉ ļö░ļØ╝ ņ£äĒŚśņØ┤ ņĪ░ņĀĢļÉ£ ņłśņØĄļźĀņØĆ Ļ░üĻ░ü 0.453%, 0.198%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØ┤ļŗż. ņןļČĆĻ░Ćņ╣ś ļīĆ ņŗ£ņןĻ░Ćņ╣śļź╝ ĒåĄņĀ£ĒĢ£ Ļ▓ĮņÜ░ ĻĖ░ņŚģĻĘ£ļ¬©ļź╝ ĒåĄņĀ£ĒĢĀ ļĢīļ│┤ļŗż COņĀäļץņØś ņłśņØĄļźĀņØ┤ ļé«ņ¦Ćļ¦ī, COņĀäļץņØĆ ņŚ¼ņĀäĒ׳ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż.

ļŗżņØīņ£╝ļĪ£, Ļ│╝Ļ▒░ņłśņØĄļźĀ(PRET)ņØä ĒåĄņĀ£ĒĢ£ Ļ▓░Ļ│╝ļŗż. <Ēæ£ 1>ņØś Ēī©ļäÉ CņŚÉ ļö░ļź┤ļ®┤ COļŖö PRETņÖĆ ņ¢æņØś ņāüĻ┤ĆĻ┤ĆĻ│äļź╝ Ļ░Ćņ¦äļŗż. ĒĢśņ¦Ćļ¦ī, <Ēæ£ 3>ņØä ĒåĄĒĢ┤ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ļ¬©ļ®śĒģĆ ņĪ░ņĀĢņłśņØĄļźĀņØĆ ļŗ©ņĪ░ļĪŁĻ▓ī ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦ĆĻ│Ā ļ¼┤ļ╣äņÜ® ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░Æņ×äņØä ĒÖĢņØĖĒĢ£ļŗż. Daniel et al.(1998)ņŚÉ ļö░ļź┤ļ®┤ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØ┤ ļ¬©ļ®śĒģĆ ĒśäņāüņØä ņĢ╝ĻĖ░ĒĢ£ļŗż. ļŗżņŗ£ ļ¦ÉĒĢ┤, Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ│╝ ļ¬©ļ®śĒģĆņØĆ ņä£ļĪ£ ņśüĒ¢źņØä ļ»Ėņ╣śļŖö Ļ┤ĆĻ│äņØ┤ļŗż. ņÜ░ļ”¼ļŖö Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ│╝ ļ¬©ļ®śĒģĆņØ┤ ņä£ļĪ£ ņ£ĀņØśĒĢ£ ņśüĒ¢źņØä ļ»Ėņ╣śļŖö Ļ┤ĆĻ│äņØĖņ¦Ć ņŚ¼ļČĆļź╝ ĒÖĢņØĖĒĢśĻĖ░ ņ£äĒĢśņŚ¼ Fama and French(2015, 2017), Barillas and Shanken (2018)ņŚÉ ļö░ļØ╝ COņÖĆ ļ¬©ļ®śĒģĆņŚÉ ļīĆĒĢ£ ņŖżĒī©ļŗØ Ļ▓ĆņĀĢņØä ņ¦äĒ¢ēĒĢ£ļŗż. Fama and French(2015, 2017)ņØś ņŖżĒī©ļŗØ Ļ▓ĆņĀĢņØĆ ĒĢ£ Ļ▓ĆņĀĢņÜöņØĖ(factor)ņØä ņóģņåŹļ│ĆņłśļĪ£ ņĘ©ĒĢśĻ│Ā ļŗżļźĖ ņÜöņØĖļōżņØä ļÅģļ”Įļ│ĆņłśļĪ£ ņĘ©ĒĢśļŖö ļ░®ņŗØņØ┤ļŗż. ĒÜīĻĘĆļČäņäØņØś ņĀłĒÄĖņØ┤ ĒåĄĻ│äņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢśņ¦Ć ņĢŖļŗżļ®┤ ĻĘĖ Ļ▓ĆņĀĢņÜöņØĖņØĆ ļŗżļźĖ ņÜöņØĖļōżņŚÉ ņØśĒĢśņŚ¼ ņŖżĒī¼(spanned)ļÉśĻ│Ā, Ļ▓ĆņĀĢņÜöņØĖņØĆ ņŻ╝ņŗØņłśņØĄļźĀņØä ņäżļ¬ģĒĢśļŖöļŹ░ ņ׳ņ¢┤ ļČłĒĢäņÜöĒĢ£(redundant) ņÜöņØĖņØ┤ļØ╝ ĒĢ┤ņäØĒĢ£ļŗż. <Ēæ£ A1>ņØĆ COņÖĆ ļ¬©ļ®śĒģĆņØś ņŖżĒī©ļŗØ Ļ▓ĆņĀĢ Ļ▓░Ļ│╝ļŗż. <Ēæ£ A1>ņØś ļ¬©ĒśĢ 1ņŚÉņä£ ļ¬©ĒśĢ 3ņØĆ ļ¬©ļ®śĒģĆņØä ņóģņåŹļ│ĆņłśļĪ£, ļ¬©ĒśĢ 4ļČĆĒä░ ļ¬©ĒśĢ 6ņØĆ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ņóģņåŹļ│ĆņłśļĪ£ ņĘ©ĒĢ£ Ļ▓░Ļ│╝ļŗż. <Ēæ£ A1>ņŚÉ ļö░ļź┤ļ®┤ ļ¬©ļ®śĒģĆ(CO)ņØä ņóģņåŹļ│ĆņłśļĪ£ ĒĢśĻ│Ā CAPM, FF3, ĻĘĖļ”¼Ļ│Ā CO(ļ¬©ļ®śĒģĆ)ļź╝ ļÅģļ”Įļ│ĆņłśļĪ£ ņĘ©ĒĢ£ Ļ▓░Ļ│╝ņŚÉņä£ ļ¬©ļ®śĒģĆ(CO)ņØś ļ╣äņĀĢņāüņĀü ņłśņØĄļźĀ(alpha)ņØĆ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļŗż. ĒŖ╣Ē׳, ļ¬©ĒśĢ 3(6)ņŚÉņä£ CO(PRET)ņØś ĒÜīĻĘĆĻ│äņłśļŖö 0.963(0.500)ņ£╝ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļŗż. ļŹö ļéśņĢäĻ░Ć, ņä£ļĪ£ ļŗżļźĖ ļ│Ćņłśļź╝ ĒÜīĻĘĆļČäņäØņŚÉ ĒżĒĢ©ĒĢ£ ļ¬©ĒśĢ 3Ļ│╝ ļ¬©ĒśĢ 6ņŚÉņä£ Ļ▓░ņĀĢĻ│äņłśņØś Ļ░ÆņØ┤ ĻĖēĻ▓®ĒĢśĻ▓ī ņ”ØĻ░ĆĒĢ£ļŗż. ļö░ļØ╝ņä£ ļ¬©ļ®śĒģĆĻ│╝ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØĆ ņä£ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś ņśüĒ¢źņØä ļ»Ėņ╣śļŖö Ļ┤ĆĻ│äļŗż. ņ”ē, <Ēæ£ 4>ņØś ļ¬©ļ®śĒģĆņØä ĒåĄņĀ£ĒĢ£ Ļ▓░Ļ│╝ļŖö ņāüļīĆņĀüņ£╝ļĪ£ ļé«ņØĆ ņłśņØĄļźĀĻ│╝ t-ĒåĄĻ│äļ¤ēņØä Ļ░Ćņ¦ł Ļ▓āņØ┤ļØ╝ ņśłņāüĒĢĀ ņłś ņ׳ļŗż. ļ¬©ļ®śĒģĆņØä ĒåĄņĀ£ĒĢ£ COņĀäļץņØś ņłśņØĄļźĀņØĆ 0.461%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØä Ļ░Ćņ¦äļŗż. ļśÉĒĢ£, CAPM, FF3 ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØĆ Ļ░üĻ░ü 0.395%, 0.060%ļĪ£ ļŗżļźĖ ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØä ĒåĄņĀ£ĒĢ£ Ļ▓ĮņÜ░ņŚÉ ļ╣äĒĢśņŚ¼ ļé«ņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ĻĘĖ ņżæ, CAPM ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØĆ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļŗż. <Ēæ£ A1>ņŚÉ ļö░ļź┤ļ®┤ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ│╝ ļ¬©ļ®śĒģĆņØĆ ņä£ļĪ£ ĻĖ┤ļ░ĆĒĢ£ Ļ┤ĆĻ│äļź╝ Ļ░Ćņ¦äļŗż. ļö░ļØ╝ņä£ Ļ│╝Ļ▒░ņłśņØĄļźĀņØĆ Ēł¼ņ×Éņ×ÉņØś Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś FF3 ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņŚÉ ļīĆĒĢ┤ ņśüĒ¢źņØä ļ»Ėņ╣£ļŗż. ĒĢśņ¦Ćļ¦ī, Ļ│╝Ļ▒░ņłśņØĄļźĀņØä ĒåĄņĀ£ĒĢ£ ĒøäņŚÉļÅä CO ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö ļŗ©ņĪ░ļĪŁĻ▓ī ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦Ćļ»ĆļĪ£ COņÖĆ ņŻ╝ņŗØņłśņØĄļźĀĻ░äņØś Ļ┤ĆĻ│äļŖö Ļ│╝Ļ▒░ņłśņØĄļźĀņŚÉ ĻĖ░ņØĖĒĢ£ Ļ▓░Ļ│╝Ļ░Ć ņĢäļŗśņØä ĒÖĢņØĖĒĢ£ļŗż.

<Ēæ£ 4>ņØś 6ņŚ┤ņØĆ ļŗ©ĻĖ░ņłśņØĄļźĀļ░śņĀä(REV)ņØä ĒåĄņĀ£ĒĢ£ Ļ▓ĮņÜ░ļŗż. <Ēæ£ 1>ņØś Ēī©ļäÉ CņŚÉ ļö░ļź┤ļ®┤ COņÖĆ REVņØś ņāüĻ┤ĆĻ┤ĆĻ│äļŖö 0.356ņ£╝ļĪ£ ņāüļīĆņĀüņ£╝ļĪ£ Ēü░ ņ¢æņØś Ļ░ÆņØ┤ļŗż. ĻĘĖļ¤╝ņŚÉļÅä ļČłĻĄ¼ĒĢśĻ│Ā, ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØś ņ░©ņØ┤ļŖö 0.699%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļ®░, ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØĆ COņŚÉ ļö░ļØ╝ ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦äļŗż. CAPMĻ│╝ FF3 ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØĆ 0.682%, 0.270%ļĪ£ ĒåĄĻ│äņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢśļŗż. ļŗ©ĻĖ░ņłśņØĄļźĀļ░śņĀäņØĆ COņÖĆ ņ¢æņØś ņāüĻ┤ĆĻ┤ĆĻ│äļź╝ Ļ░Ćņ¦Ćņ¦Ćļ¦ī, COņĀäļץņØś ņłśņØĄņä▒ņŚÉ ņ£ĀņØśĒĢ£ ņśüĒ¢źņØä ļ»Ėņ╣śņ¦Ć ļ¬╗ĒĢ£ļŗż.

<Ēæ£ 4>ņØś 7ņŚ┤ņØĆ Amihud(2002)ņØś ņ£ĀļÅÖņä▒(ILLIQ)ņØä ĒåĄņĀ£ĒĢ£ Ļ▓░Ļ│╝ļŗż. <Ēæ£ 1>ņŚÉ ļö░ļź┤ļ®┤ ILLIQņÖĆ COļŖö ņØīņØś ņāüĻ┤ĆĻ┤ĆĻ│äļź╝ Ļ░Ćņ¦ĆĻ│Ā ņ׳ļŗż. COļŖö ņ£ĀļÅÖņä▒ņØś ļ│ĆĒÖöņŚÉ Ēü¼Ļ▓ī ņÜöļÅÖĒĢśņ¦Ć ņĢŖņ£╝ļ®░, COņĀäļץņØś ņłśņØĄļźĀņØĆ 0.823%ļĪ£ ņ£ĀņØśĒĢśļŗż. Ļ░ü ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØś ņ░©ņØ┤ļŖö 0.835%, 0.255%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļŗż. ļö░ļØ╝ņä£ ņ£ĀļÅÖņä▒ņØĆ COņÖĆ ļ»Ėļל ņŻ╝ņŗØņłśņØĄļźĀ ņé¼ņØ┤ņØś ņ¢æņØś Ļ┤ĆĻ│äļź╝ ņäżļ¬ģĒĢśņ¦Ć ņĢŖļŖöļŗż.

ļŗżņØīņØĆ ņŗØ (5)ļĪ£ ļÅäņČ£ļÉ£ Ļ│Āņ£Āļ│ĆļÅÖņä▒(IVOL)ņØä ĒåĄņĀ£ĒĢ£ Ļ▓░Ļ│╝ļŗż. ļ¼┤ļ╣äņÜ® ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö 0.741%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. CAPM, FF3 ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØĆ Ļ░üĻ░ü 0.722%, 0.280%ļĪ£ ņ£ĀņØśĒĢ£ Ļ░ÆņØ┤ļŗż. ļö░ļØ╝ņä£ IVOLņØĆ COņÖĆ ņŻ╝ņŗØņłśņØĄļźĀ Ļ░äņØś Ļ┤ĆĻ│äļź╝ ņČ®ļČäĒ׳ ņäżļ¬ģĒĢśņ¦Ć ļ¬╗ĒĢ£ļŗż.

<Ēæ£ 4>ņØś ļ¦łņ¦Ćļ¦ē ņŚ┤ņØĆ Ļ▒░ļלļ¤ēĒÜīņĀäņ£©(TURN)ņØä ĒåĄņĀ£ĒĢ£ Ļ▓░Ļ│╝ņØ┤ļŗż. <Ēæ£ 1>ņŚÉņä£ Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ĒÅēĻĘĀ ĒÜīņĀäņ£©Ļ│╝ COĻ░äņØś Ļ┤ĆĻ│äļź╝ ĒÖĢņØĖĒĢ£ Ļ▓░Ļ│╝, COļŖö TURNĻ│╝ ņ¢æņØś ņāüĻ┤ĆĻ┤ĆĻ│äņŚÉ ņ׳ņ¦Ćļ¦ī ĻĘĖ Ļ░ÆņØĆ 0.017ļĪ£ ĒśäņĀĆĒ׳ ļé«ļŗż. Ļ▒░ļלļ¤ē ĒÜīņĀäņ£©ņØä ņĀ£ņ¢┤ĒĢ£ Ēøä COņĀäļץņØś ņłśņØĄļźĀņØĆ 0.548%ņØ┤ļ®░ CAPM, FF3 ņ£äĒŚśņĪ░ņĀĢ ņłśņØĄļźĀņØĆ Ļ░üĻ░ü 0.516%, 0.197%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļŗż.

ļ│Ė ņĀłņŚÉņä£ļŖö ĻĖ░ņŚģĒŖ╣ņä▒ņØä ļéśĒāĆļé┤ļŖö ņÜöņØĖņØĖ ņŗ£ņןļ▓ĀĒāĆ(BETA), ĻĖ░ņŚģĻĘ£ļ¬©(SIZE), ņןļČĆĻ░Ćņ╣ś ļīĆ ņŗ£ņןĻ░Ćņ╣ś(BEME), Ļ│╝Ļ▒░ņłśņØĄļźĀ(PRET), ļŗ©ĻĖ░ņłśņØĄļźĀļ░śņĀä(REV), ņ£ĀļÅÖņä▒(ILLIQ), Ļ│Āņ£Āļ│ĆļÅÖņä▒ (IVOL), Ļ▒░ļלļ¤ēĒÜīņĀäņ£©(TURN)ņØä ĒåĄņĀ£ĒĢ£ Ēøä COņĀäļץņØś ņłśņØĄņä▒ņØä ĒÖĢņØĖĒĢ£ļŗż. ĻĘĖ Ļ▓░Ļ│╝, ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØä ĒåĄņĀ£ĒĢśņŚ¼ļÅä COņĀäļץņØĆ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä ņ£Āņ¦ĆĒĢ£ļŗż. Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØ┤ ļåÆņØĆ(ļé«ņØĆ) ņŻ╝ņŗØņØ╝ņłśļĪØ Ēł¼ņ×Éņ×ÉņŚÉĻ▓ī ņĀĆĒÅēĻ░Ć(Ļ│ĀĒÅēĻ░Ć)ļÉśņ¢┤ ļåÆņØĆ(ļé«ņØĆ) ņŻ╝ņŗØņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ĒśäņāüņØĆ ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØä ĒåĄņĀ£ĒĢśņŚ¼ļÅä ņ£Āņ¦ĆļÉ£ļŗż. ļŗżņŗ£ ļ¦ÉĒĢ┤, Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ│╝ ņŻ╝ņŗØņłśņØĄļźĀ Ļ░äņØś ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ┤ĆĻ│äļŖö ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņŚÉ ĻĖ░ņØĖĒĢśļŖö ĒśäņāüņØ┤ ņĢäļŗłļŗż. ļö░ļØ╝ņä£ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ļīĆĒĢśņŚ¼ ņŗ£ņןļ▓ĀĒāĆ, ņŗ£ņןĻĘ£ļ¬©, ņןļČĆĻ░Ćņ╣ś ļīĆ ņŗ£ņןĻ░Ćņ╣ś, Ļ│╝Ļ▒░ņłśņØĄļźĀ, ļŗ©ĻĖ░ņłśņØĄļźĀļ░śņĀä, ņ£ĀļÅÖņä▒, Ļ│Āņ£Āļ│ĆļÅÖņä▒, Ļ▒░ļלļ¤ēĒÜīņĀäņ£©ņØś ĒÜ©Ļ│╝ļĪ£ļŖö ļåÆņØĆ COņŻ╝ņŗØņŚÉ ļīĆĒĢ£ ļåÆņØĆ ņłśņØĄļźĀņØä ņäżļ¬ģĒĢĀ ņłś ņŚåļŗż.

4.4 Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ│╝ ņłśņØĄļźĀ ņ¦ĆņåŹņä▒, ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ņØś Ļ┤ĆĻ│ä

ĻĖ░ņĪ┤ņØś ņŚ░ĻĄ¼ļōżņØĆ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ņłśņØĄļźĀ ņ¦ĆņåŹņä▒(return consistency)ņØś ņŚŁĒĢĀĻ│╝ ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ (information discreteness)ņØä ņĪ░ņé¼Ē¢łļŗż. Grinblatt and Moskowitz(2004)ņŚÉ ļö░ļź┤ļ®┤ ņ¢æņØś Ļ│╝Ļ▒░ņłśņØĄļźĀņØś ņ¦ĆņåŹņä▒ņØĆ ĻĖ░ļīĆņłśņØĄļźĀņŚÉ ĒÜĪļŗ©ļ®┤ņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢ£ ņśüĒ¢źņØä ļ»Ėņ╣£ļŗż. Watkins(2006)ņŚÉ ļö░ļź┤ļ®┤ Ļ│╝Ļ▒░ 2ņŻ╝ ļÅÖņĢł ĻŠĖņżĆĒĢśĻ▓ī ņ¢æņØś(ņØīņØś) ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ņŻ╝ņŗØņØĆ ĻĘĖļĀćņ¦Ć ņĢŖņØĆ ņŻ╝ņŗØņŚÉ ļ╣äĒĢśņŚ¼ ļåÆņØĆ(ļé«ņØĆ) ļ»ĖļלņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ļŗ©ĻĖ░ ņłśņØĄļźĀņØś ņ¦ĆņåŹņä▒ņØä ņØ┤ņÜ®ĒĢ£ ņĀäļץņØĆ ņŗ£Ļ░äņØ┤ ņ¦Ćļé©ņŚÉ ļö░ļØ╝ ņ£ĀņØśĒĢśļŗż. Alwathainani(2009)ļŖö ĻĖ░ņŚģņØś Ļ│╝Ļ▒░ ņ×¼ļ¼┤ņä▒Ļ│╝ņØś ņä▒ņןņ¦ĆņåŹņä▒ņØä ĒåĄĒĢ┤ ļ»ĖļלņłśņØĄļźĀņØä ņśłņĖĪĒĢĀ ņłś ņ׳ļŗżĻ│Ā ņŻ╝ņןĒĢ£ļŗż. ņØ┤ļ¤¼ĒĢ£ Ļ┤ĆĻ│äļŖö Ļ│Āņä▒ņן ĻĖ░ņŚģņŚÉ ļ╣äĒĢśņŚ¼ ņĀĆņä▒ņן ĻĖ░ņŚģņŚÉņä£ ļŹöņÜ▒ Ļ░ĢĒĢśĻ▓ī ļéśĒāĆļé£ļŗż. Da et al.(2014)ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äļÅÖņĢł ļ░£ņāØĒĢ£ ņØ╝ļ│ä ņłśņØĄļźĀņØś ļČĆĒśĖļź╝ ņØ┤ņÜ®ĒĢśņŚ¼ ņĀĢļ│┤ņØś ĒØÉļ”äņØ┤ ņŚ░ņåŹņĀüņØĖņ¦Ć ņŚ¼ļČĆļź╝ ĒÖĢņØĖĒĢ£ļŗż. ņĀĢļ│┤ņØś ĒØÉļ”äņŚÉ ļīĆĒĢ£ ņĖĪņĀĢņ╣śļŖö ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ (information discreteness, ID)ņ£╝ļĪ£ ļéśĒāĆļéĖļŗż. Da et al.(2014)ņŚÉ ļö░ļź┤ļ®┤, ņŚ░ņåŹņĀüņØĖ ņĀĢļ│┤ļŖö Ļ░ĢĒĢ£ ņłśņØĄļźĀ ņ¦ĆņåŹņä▒ņØä ņĢ╝ĻĖ░ĒĢ£ļŗż. Lin et al.(2016)ņØĆ IDļĪ£ Ļ│╝Ļ▒░ņłśņØĄļźĀņŚÉ ļé┤ņ×¼ļÉ£ ņŚ░ņåŹņĀüņØĖ ņĀĢļ│┤ļź╝ ņŗØļ│äĒĢśņŚ¼ ļīĆļ¦īņŻ╝ņŗØņŗ£ņןņŚÉ ņĪ┤ņ×¼ĒĢśļŖö Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņåīļ░śņØæņØä ņäżļ¬ģĒĢ£ļŗż. ņóģĒĢ®ĒĢśļ®┤, ļÅÖņØ╝ĒĢ£ ļ░®Ē¢źņ£╝ļĪ£ ņŚ░ņåŹļÉśļŖö ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ņŻ╝ņŗØņØś Ļ▓ĮņÜ░ ĻĘ╣ļŗ©ņĀüņØĖ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢśļŖö Ļ▓ĮĒ¢źņØ┤ ņ׳Ļ│Ā, ļåÆņØĆ ņłśņżĆņØś ņłśņØĄļźĀ ņ¦ĆņåŹņä▒Ļ│╝ ļé«ņØĆ ņłśņżĆņØś ņĀĢļ│┤ ļČłņŚ░ņåŹņØä Ļ░Ćņ¦ł Ļ░ĆļŖźņä▒ņØ┤ ņ׳ļŗżĻ│Ā ņśłņāüĒĢĀ ņłś ņ׳ļŗż. ļ│Ė ņĀłņŚÉņä£ ņÜ░ļ”¼ļŖö COņØś ĒÜ©Ļ│╝Ļ░Ć ņłśņØĄļźĀ ņ¦ĆņåŹņä▒ ļśÉļŖö ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ņŚÉ ĻĖ░ņØĖĒĢśļŖöņ¦Ć ņŚ¼ļČĆļź╝ ĒÖĢņØĖĒĢ£ļŗż.

Grinblatt and Moskowitz(2004)ļŖö ņłśņØĄļźĀ ņ¦ĆņåŹņä▒ Ļ░Ćļ│ĆņłśļĪ£ POS_RCņÖĆ NEG_RCļź╝ ņĀ£ņŗ£ĒĢ£ļŗż. Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ņłśņØĄļźĀņØ┤ ņ¢æ(ņØī)ņØś Ļ░ÆņØĖ ņŻ╝ņŗØņØä ļīĆņāüņ£╝ļĪ£ Ļ│╝Ļ▒░ ņ¢æ(ņØī)ņØś ņłśņØĄļźĀņØä ņĀüņ¢┤ļÅä 8Ļ░£ņøö ņØ┤ņāü Ļ▓ĮĒŚśĒ¢łļŗżļ®┤ POS_RC(NEG_RC)ņŚÉ 1ņØä ļČĆņŚ¼ĒĢ£ļŗż. COļ│ĆņłśļŖö ņøöļ│ä ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ēņØä ņé¼ņÜ®ĒĢśĻĖ░ ļĢīļ¼ĖņŚÉ, ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö Ļ░£ņøöņØś ņłśņÖĆ ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö Ļ░£ņøöņØś ņłśļŖö ņłśņØĄļźĀ ņ¦ĆņåŹņä▒ņØś ĒÜ©Ļ│╝ļź╝ ņל ļéśĒāĆļé╝ Ļ▓āņØ┤ļŗż.

ļŹö ļéśņĢäĻ░Ć, Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ ņĀäļץņØś ņłśņØĄņä▒ņØ┤ ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░ä ļÅÖņĢł ņ¢æņØś(ņØīņØś) ņøöļ│ä ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļŗ¼ņØś Ļ░£ņłśņŚÉ ņØśĒĢ£ Ļ▓āņØĖņ¦Ć ņŚ¼ļČĆļź╝ ĒÖĢņØĖĒĢśĻĖ░ ņ£äĒĢ┤ ļŗżļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśż ļČäņäØņØä ņ¦äĒ¢ēĒĢ£ļŗż. ļŗżļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö COļ│ĆņłśņÖĆ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ļŗ¼ņØś Ļ░£ņłśņŚÉņä£ ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ļŗ¼ņØś Ļ░£ņłśļź╝ ļ║Ć NPOS_NEGļĪ£ ĻĄ¼ņä▒ļÉ£ļŗż. <Ēæ£ 5>ņØś Ēī©ļäÉ AļŖö COņÖĆ Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ņłśņØĄļźĀ ņżæ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļŗ¼ņØś Ļ░£ņłśņŚÉņä£ ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļŗ¼ņØś Ļ░£ņłśļź╝ ļ║Ć(NPOS_NEG) ļ│Ćņłśļź╝ ņØ┤ņÜ®ĒĢ£ ļŗżļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśż Ļ▓░Ļ│╝ļŗż. ļ¦żņøö NPOS_NEGļź╝ ĻĖ░ņżĆņ£╝ļĪ£ ĒĢśņ£ä 30%ņŚÉ ņåŹĒĢśļŖö ņŻ╝ņŗØņØä ĒżĒŖĖĒÅ┤ļ”¼ņśż 1, ņāüņ£ä 30%ņŚÉ ņåŹĒĢśļŖö ņŻ╝ņŗØņØä ĒżĒŖĖĒÅ┤ļ”¼ņśż 3ņŚÉ ļČĆņŚ¼ĒĢśĻ│Ā, ļæÉ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢśņ¦Ć ņĢŖļŖö ņżæĻ░ä 40%ņØś ņŻ╝ņŗØņŚÉ ĒżĒŖĖĒÅ┤ļ”¼ņśż 2ļź╝ ļČĆņŚ¼ĒĢ£ļŗż. Ļ░ü NPOS_NEG ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØä ļīĆņāüņ£╝ļĪ£ COņŚÉ ļö░ļźĖ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļĪ£ ļéśļłłļŗż. COĻ░Ć Ļ░Ćņן ļé«ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ Low 1ņØä, Ļ░Ćņן ļåÆņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ High 5ļź╝ ļČĆņŚ¼ĒĢ£ļŗż. ĻĘĖ Ļ▓░Ļ│╝, COĻ░Ć ļåÆņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļ¦żņ×ģĒĢśĻ│Ā COĻ░Ć ļé«ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļ¦żļÅäĒĢśļŖö ņĀäļץņØĆ Ļ░ü NPOS_NEG ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉņä£ 0.561%, 0.539%, 0.549%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ļö░ļØ╝ņä£ Ļ│╝Ļ▒░ĻĖ░Ļ░äļÅÖņĢł ņøöļ│ä ņ¢æņØś ņłśņØĄļźĀņØś ļŗ¼ņØś ņłśņÖĆ ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ļŗ¼ņØś ņłśļŖö COņĀäļץņŚÉ ņ£ĀņØśĒĢ£ ņśüĒ¢źņØä ļ»Ėņ╣śņ¦Ć ļ¬╗ĒĢ£ļŗż.

<Ēæ£┬Ā5>

ņČöĻ░ĆņĀüņØĖ ļ│Ćņłśļź╝ ĒåĄņĀ£ĒĢ£ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀ

ņØ┤ Ēæ£ļŖö ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░ä ļÅÖņĢł ņ¢æĻ│╝ ņØīņØś ņøöļ│äņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļŗ¼ņØś Ļ░£ņłśņÖĆ ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒(ID)ņØä ĒåĄņĀ£ĒĢ£ Ēøä COļĪ£ ĻĄ¼ņä▒ĒĢ£ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØ┤ļŗż. Ēī©ļäÉ AļŖö ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ļŗ¼ņØś ņłśņŚÉņä£ ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ļŗ¼ņØś ņłśļź╝ ļ║Ć(NPOS_NEG) ļ│Ćņłśļź╝ ĒåĄņĀ£ĒĢ£ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØ┤ļŗż. Ēī©ļäÉ BļŖö Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ņØ╝ļ│ä ļłäņĀüņłśņØĄļźĀ ļČĆĒśĖņŚÉ ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļéĀņØś ļ╣äņ£©Ļ│╝ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļéĀņØś ļ╣äņ£©ņØś ņ░©ņØ┤ļź╝ Ļ│▒ĒĢ£ IDļź╝ ĒåĄņĀ£ĒĢ£ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØ┤ļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØĆ 6Ļ░£ņøö(K=6)ņØ┤Ļ│Ā, ņłśņØĄļźĀņØĆ ĒŹ╝ņä╝ĒŖĖ ļŗ©ņ£äļŗż. Ēæ£ļ│ĖņØĆ 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņןĻ│╝ ņĮöņŖżļŗźņŗ£ņןņŚÉ ņāüņןļÉ£ ļ│┤ĒåĄņŻ╝ ņżæņŚÉņä£ ņŻ╝ļŗ╣ Ļ░ĆĻ▓®ņØ┤ 500ņøÉļ│┤ļŗż Ēü░ ņŻ╝ņŗØņØ┤ļŗż. ***, **, *ļŖö Ļ░üĻ░ü 1%, 5%, 10% ņ£ĀņØśņłśņżĆņŚÉņä£ ņ£ĀņØśĒĢ©ņØä Ēæ£ņŗ£ĒĢ£ļŗż. Ļ┤äĒśĖ ņĢłņØś ņł½ņ×ÉļŖö Newey and West(1987) t-ĒåĄĻ│äļ¤ēņØ┤ļŗż.

Ēī©ļäÉ A: NPOS_NEGņÖĆ CO

ļŗżņØīņ£╝ļĪ£, ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒Ļ│╝ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś Ļ┤ĆĻ│äļź╝ ņĪ░ņé¼ĒĢ£ļŗż. Da et al.(2014)ļŖö ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ņØś ļ│Ćņłś(ID)ļź╝ ņĀĢņØśĒĢśņŚ¼ ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ ĻĖ░Ļ░ä ņżæ ņĀĢļ│┤Ļ░Ć ņŚ░ņåŹņĀüņØĖņ¦Ć ļČłņŚ░ņåŹņĀüņØĖņ¦Ć ņŚ¼ļČĆļź╝ ļéśĒāĆļéĖļŗż. ņ£äņØś ņŚ░ĻĄ¼ņŚÉ ļö░ļź┤ļ®┤ Ēł¼ņ×Éņ×ÉļŖö ņŚ░ņåŹņĀüņØĖ ņĀĢļ│┤ņŚÉ ļīĆĒĢ┤ ļČłņŚ░ņåŹņĀüņØĖ ņĀĢļ│┤ļ│┤ļŗż ņŻ╝ņØśļź╝ ļŹ£ ĻĖ░ņÜĖņØĖļŗż. ļö░ļØ╝ņä£ ņŚ░ņåŹņĀüņØĖ ņĀĢļ│┤Ļ░Ć Ļ░ĢĒĢ£ ņłśņØĄļźĀ ņ¦ĆņåŹņØä ņ£ĀļÅäĒĢ£ļŗż. IDļŖö ņØ╝ļ│ä ņłśņØĄļźĀņØś ļČĆĒśĖņŚÉ ļö░ļØ╝ ņŗØ (7)Ļ│╝ Ļ░ÖņØ┤ ļÅäņČ£ļÉ£ļŗż.

IDi,tļŖötņøöņØśiļ▓łņ¦Ė ņŻ╝ņŗØņØś ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ ļ│ĆņłśņØ┤ļŗż. PRETļŖöt-12ņøöļČĆĒä░t-2ņøöņØś ņØ╝ļ│ä ļłäņĀüņłśņØĄļźĀņØ┤ļŗż. sng(PRET)ļŖö Ļ│╝Ļ▒░ņłśņØĄļźĀņØś ļČĆĒśĖļĪ£PRET>0ņØ┤ļ®┤ 1ņØä, PRET<0ņØ┤ļ®┤ -1ņØä ļČĆņŚ¼ĒĢ£ļŗż. %posļŖö Ļ│╝Ļ▒░ĻĖ░Ļ░äļÅÖņĢł ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ļéĀņØś ļ╣äņ£©ņØ┤Ļ│Ā, %ŌĆØnegŌĆØļŖö Ļ│╝Ļ▒░ĻĖ░Ļ░äļÅÖņĢł ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ļéĀņØś ļ╣äņ£©ņØ┤ļŗż. Ļ│╝Ļ▒░ĻĖ░Ļ░äņØś ņłśņØĄļźĀņØ┤ ņŚ¼ļ¤¼ ļéĀņŚÉ Ļ▒Ėņ│É ļłäņĀüļÉśļ®┤ ņĀĢļ│┤ņØś ņŚ░ņåŹņä▒ņØ┤ ņ¦ĆņåŹļÉśĻ│Ā, ņŚ░ņåŹņĀü ņĀĢļ│┤ļŖö ļŹö Ļ░ĢĒĢśĻ│Ā ņ¦ĆņåŹņä▒ņØĖ ņłśņØĄļźĀņØä ņ£ĀļÅäĒĢ£ļŗż. ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒(ID)ņØĆ ņĀĢļ│┤ņØś ņāüļīĆņĀü ļ╣łļÅäļź╝ ļéśĒāĆļéĖļŗż. ļåÆņØĆ IDļŖö ļČłņŚ░ņåŹņĀüņØĖ ņĀĢļ│┤ļź╝, ļé«ņØĆ IDļŖö ņŚ░ņåŹņĀüņØĖ ņĀĢļ│┤ļź╝ ļéśĒāĆļéĖļŗż. ņÜ░ļ”¼ļŖö COņÖĆ ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ ņĖĪņĀĢņ╣śļź╝ ĻĖ░ņżĆņ£╝ļĪ£ ļŗżļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢ£ļŗż.

<Ēæ£ 5>ņØś Ēī©ļäÉ BļŖö ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ņŚÉ ļö░ļźĖ COņĀäļץņØä ļéśĒāĆļéĖļŗż. Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ņØ╝ļ│ä ļłäņĀüņłśņØĄļźĀļĪ£ ļÅäņČ£ļÉ£ IDļź╝ ĻĖ░ņżĆņ£╝ļĪ£ 5Ļ░£ņØś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļéśļłäĻ│Ā, Ļ░ü IDĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØä COņŚÉ ļö░ļØ╝ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļĪ£ ļéśļłłļŗż. ĻĘĖ Ļ▓░Ļ│╝, ID ĻĘĖļŻ╣ņŚÉņä£ COņĀäļץņØś ņłśņØĄļźĀņØĆ 0.986%, 0.652%, 0.612%, 0.370%, 0.343%ļĪ£ ļ¬©ļæÉ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ĒŖ╣Ē׳, IDĻ░Ć ļåÆņĢäņ¦ÉņŚÉ ļö░ļØ╝ COņĀäļץņØś ņłśņØĄļźĀņØ┤ ļé«ņĢäņ¦ĆļŖö Ļ▓āņØä ĒÖĢņØĖĒĢ£ļŗż. <Ēæ£ 5>ņØś Ēī©ļäÉ BņŚÉ ļö░ļź┤ļ®┤ ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ņØ┤ COļź╝ ņÖäņĀäĒ׳ ņäżļ¬ģĒĢśņ¦Ć ļ¬╗ĒĢ£ļŗż.

ņÜ░ļ”¼ļŖö ĻĖ░ņŚģĒŖ╣ņä▒ ļ│Ćņłś ļ┐É ņĢäļŗłļØ╝ ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ņØä ĒåĄņĀ£ĒĢ£ Ļ▓ĮņÜ░ņŚÉļÅä COņĀäļץņØ┤ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ÉņØä ļ│┤ņśĆļŗż. ļŹö ļéśņĢäĻ░Ć, Fama-Macbeth ĒÜĪļŗ©ļ®┤ ļČäņäØņØä ĒåĄĒĢśņŚ¼ ĻĖ░ņŚģĒŖ╣ņä▒ļ│ĆņłśņÖĆ ņłśņØĄļźĀ ņ¦ĆņåŹņä▒, ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒, ĻĘĖļ”¼Ļ│Ā ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░ä ļÅÖņĢł ņ¢æĻ│╝ ņØīņØś ņøöļ│äņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļŗ¼ņØś Ļ░£ņłśņØś ņ░©ņØ┤ļź╝ ļÅÖņŗ£ņŚÉ ĒåĄņĀ£ĒĢ£ ĒøäņŚÉļÅä COĻ░Ć ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆĒĢśņŚ¼ ņ£ĀņØśĒĢ£ ņ¢æņØś ņśłņĖĪļĀźņØä Ļ░Ćņ¦ĆļŖöņ¦Ć ĒÖĢņØĖĒĢ£ļŗż. IDļŖö ņØ╝ļ│äņłśņØĄļźĀņØä ņØ┤ņÜ®ĒĢ£ ņŚ░ņåŹņĀüņØĖ ļ│ĆņłśņØ┤ņ¦Ćļ¦ī, Grinblatt and Moskowitz (2004)ņØś ņłśņØĄļźĀ ņ¦ĆņåŹņä▒ņØĆ ņøöļ│äņłśņØĄļźĀņØä ņØ┤ņÜ®ĒĢ£ ļČłņŚ░ņåŹņĀüņØĖ ļ│ĆņłśņØ┤ļŗż. Da et al.(2014)ņØĆ ņłśņØĄļźĀ ņ¦ĆņåŹņä▒Ļ│╝ IDņØś Ļ▓ĮņĀ£ņĀü ņØśļ»Ėļź╝ ĻĄ¼ļČäĒĢśĻĖ░ ņ£äĒĢśņŚ¼ Ļ│╝Ļ▒░ ņŖ╣ņ×ÉņÖĆ Ēī©ņ×ÉņØś Ļ┤ĆņĀÉņŚÉņä£ IDļź╝ ļČäļźśĒĢ£ļŗż. ļČĆĒśĖĒÖöļÉ£ IDļŖö POS_IDņÖĆ NEG_IDļĪ£ ņŗØ (8)Ļ│╝ Ļ░Öļŗż.

(8)

%posļŖö Ļ│╝Ļ▒░ĻĖ░Ļ░ä ļÅÖņĢł ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ļéĀņØś ļ╣äņ£©ņØ┤Ļ│Ā, %ŌĆØnegŌĆØļŖö Ļ│╝Ļ▒░ĻĖ░Ļ░ä ļÅÖņĢł ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ļéĀņØś ļ╣äņ£©ņØ┤ļŗż. rt-12,t-1ņØĆt-12ņøöļČĆĒä░t-1ņøöņØś ļłäņĀüņłśņØĄļźĀņØ┤ļŗż. POS_IDļŖö Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ņØ╝ļ│ä ļłäņĀüņłśņØĄļźĀņØ┤ ņ¢æņØś Ļ░ÆņØ╝ Ļ▓ĮņÜ░, ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļéĀņØś ļ╣äņ£©ņŚÉņä£ ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļéĀņØś ļ╣äņ£©ņØä ļ║Ć Ļ░ÆņØ┤ļŗż. NEG_IDļŖö Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ņØ╝ļ│ä ļłäņĀüņłśņØĄļźĀņØ┤ ņØīņØś Ļ░ÆņØ╝ Ļ▓ĮņÜ░, ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļéĀņØś ļ╣äņ£©ņŚÉņä£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļéĀņØś ļ╣äņ£©ņØä ļ║Ć Ļ░ÆņØ┤ļŗż. Ļ│╝Ļ▒░ĻĖ░Ļ░ä ļÅÖņĢł ņ¢æĻ│╝ ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļéĀņØś ļ╣äņ£©ņØś ņ░©ņØ┤ņØĖ POS_IDņÖĆ NEG_IDļŖö ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ņØä ļéśĒāĆļéĖļŗż.

ņÜ░ļ”¼ļŖö Fama and Macbeth(1973)ņØś ĒÜĪļŗ©ļ®┤ ĒÜīĻĘĆļČäņäØņØä ĒåĄĒĢśņŚ¼ COņØś ņśłņĖĪļĀźņØä ĒÖĢņØĖĒĢ£ļŗż. ņóģņåŹļ│ĆņłśļŖö 6Ļ░£ņøö ļ│┤ņ£ĀĻĖ░Ļ░ä ņłśņØĄļźĀ(buy and hold returns)ņØ┤ļ®░ ņŗØ (9)ņŚÉ ļö░ļØ╝ ĒÜĪļŗ©ļ®┤ ĒÜīĻĘĆļČäņäØņØä ņ¦äĒ¢ēĒĢ£ļŗż.

(9)

ri,t+1,t+6ļŖöiļ▓łņ¦Ė ņŻ╝ņŗØņØśt+1ņøöļČĆĒä░t+6ņøöņØś 6Ļ░£ņøö ņłśņØĄļźĀņØ┤Ļ│Ā, COi,tļŖö COļ│ĆņłśņØ┤ļŗż. PRETi,tļŖö ņ¦Ćļé£t-12ņøöļČĆĒä░t-2ņøöņØś ļłäņĀüņłśņØĄļźĀņØ┤ļ®░, POS_IDi,tņÖĆNEG_ID_i,tļŖö ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ ļ│ĆņłśņØ┤ļŗż. POS_RCi,tņÖĆNEG_RCi,tļŖö ņłśņØĄļźĀ ņ¦ĆņåŹņä▒ Ļ░Ćļ│ĆņłśņØ┤ļŗż. NPOS_NEGi,tļŖö ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ļŗ¼ņØś Ļ░£ņłśņŚÉņä£ ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆļŖö ļŗ¼ņØś Ļ░£ņłśļź╝ ļ║Ć Ļ░ÆņØ┤ļŗż. CGOi,tļŖö ļ»ĖņŗżĒśä ņ×Éļ│Ė ņØ┤ņØĄņØ┤ļŗżBETAi,t.ļŖötņøöņØś ņŗ£ņןļ▓ĀĒāĆņØ┤ļŗż. SIZEi,tļŖötņøöņØś ĻĖ░ņŚģĻĘ£ļ¬©ņØ┤Ļ│Ā, BEMEi,tļŖötņøöņØś ņןļČĆĻ░Ćņ╣ś ļīĆ ņŗ£ņןĻ░Ćņ╣śņØ┤ļ®░, REVi,tļŖö ļŗ©ĻĖ░ņłśņØĄļźĀļ░śņĀäņØ┤ļŗż. ILLIQi,tļŖö Amihud(2002)ņŚÉ ļö░ļźĖ ņ£ĀļÅÖņä▒ ļ│ĆņłśņØ┤ļ®░, IVOLi,tņØĆtņøöņØś Ļ│Āņ£Āļ│ĆļÅÖņä▒ņØ┤Ļ│Ā, TURNi,tļŖö Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ĒÅēĻĘĀ ņøöļ│äĻ▒░ļלļ¤ē ĒÜīņĀäļźĀņØ┤ļŗż.

<Ēæ£ 6>ņØĆ ĒÜīĻĘĆĻ│äņłśņØś ņŗ£Ļ│äņŚ┤ ĒÅēĻĘĀņØ┤ļ®░, Ļ┤äĒśĖņĢłņØś Ļ░ÆņØĆ Newey and West(1987)ņØś t-ĒåĄĻ│äļ¤ē ņØ┤ļŗż. ļ¬©ĒśĢ 1ņØĆ COĻ│╝ ĒÜĪļŗ©ļ®┤ņĀü ņŻ╝ņŗØņłśņØĄļźĀ Ļ░äņØś Ļ┤ĆĻ│äļź╝ ļéśĒāĆļéĖļŗż. ļ¬©ĒśĢ 1ņŚÉ ļö░ļź┤ļ®┤ COļŖö ĒÜĪļŗ©ļ®┤ņĀü ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ņ£ĀņØśĒĢ£ ņ¢æņØś ņśłņĖĪļĀźņØä Ļ░Ćņ¦äļŗż. CO ĒÜīĻĘĆĻ│äņłśņØś ĒÅēĻĘĀņØĆ 0.042ņØ┤Ļ│Ā, t-ĒåĄĻ│äļ¤ēņØĆ 3.739ņØ┤ļŗż. ļ¬©ĒśĢ 2ļŖö COņÖĆ Ļ│╝Ļ▒░ņłśņØĄļźĀ(PRET)ļź╝ ĒÜīĻĘĆļČäņäØņŚÉ ņČöĻ░ĆĒĢ£ Ļ▓░Ļ│╝ņØ┤ļŗż. PRETļŖö ņŻ╝ņŗØņłśņØĄļźĀĻ│╝ ņ£ĀņØśĒĢ£ ņØīņØś Ļ┤ĆĻ│äĻ░Ć ņ׳ļŖö ļ░śļ®┤, COņØś ĒÜīĻĘĆĻ│äņłśļŖö 0.052ņØ┤Ļ│Ā t-ĒåĄĻ│äļ¤ēņØĆ 4.975ļĪ£ ļ¬©ĒśĢ 1ņŚÉ ļ╣äĒĢśņŚ¼ ņāüņŖ╣Ē¢łļŗż. Ļ│╝Ļ▒░ņłśņØĄļźĀņØä Ļ│ĀļĀżĒĢ£ ĒøäņŚÉļÅä ĒÜĪļŗ©ļ®┤ņĀü ņłśņØĄļźĀņŚÉ ļīĆĒĢ£ COņØś ņśłņĖĪļĀźņØ┤ ņ£Āņ¦ĆļÉ£ļŗż. ļ¬©ĒśĢ 3Ļ│╝ ļ¬©ĒśĢ 4ļŖö ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒Ļ│╝ ņłśņØĄļźĀ ņ¦ĆņåŹņä▒ ļ│Ćņłśļź╝ Ļ│ĀļĀżĒĢ£ Ļ▓ĮņÜ░ņØ┤ļŗż. ļæÉ Ļ▓ĮņÜ░ņŚÉņä£ COļŖö ĒÜĪļŗ©ļ®┤ņĀü ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆĒĢśņŚ¼ ņŚ¼ņĀäĒ׳ ņ£ĀņØśĒĢ£ ņ¢æņØś ĒÜīĻĘĆĻ│äņłśļź╝ Ļ░Ćņ¦äļŗż. ļŹö ļéśņĢäĻ░Ć, ĻĖ░ņŚģĒŖ╣ņä▒ ļ│Ćņłśļź╝ ĒÜīĻĘĆļ¬©ĒśĢņŚÉ ņČöĻ░ĆĒĢ£ ļ¬©ĒśĢ 5ņÖĆ ļ¬©ĒśĢ 6ņŚÉņä£ļÅä COļŖö ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ņ£ĀņØśĒĢ£ ņ¢æņØś ņśłņĖĪļĀźņØä Ļ░Ćņ¦äļŗż. ņÜ░ļ”¼ļŖö ņŚ¼ļ¤¼ Ļ░Ćņ¦Ć ļ│Ćņłśļź╝ ĒåĄņĀ£ĒĢśņŚ¼ļÅä ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆĒĢ£ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś ņśłņĖĪļĀźņØ┤ ņ£Āņ¦ĆļÉ©ņØä ņ×¼ĒÖĢņØĖĒĢ£ļŗż.

<Ēæ£┬Ā6>

Fama-Macbeth ĒÜĪļŗ©ļ®┤ ļČäņäØ

ņØ┤ Ēæ£ļŖö ĻĖ░ņŚģņłśņżĆņŚÉņä£ Fama-Macbeth ĒÜĪļŗ©ļ®┤ ļČäņäØņØä ļéśĒāĆļéĖļŗż. 6Ļ░£ņøö ļ│┤ņ£ĀņłśņØĄļźĀņØä ņóģņåŹļ│ĆņłśļĪ£ ĒĢśĻ│Ā, Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ(CO), Ļ│╝Ļ▒░ņłśņØĄļźĀ(PRET), ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒(POS_ID/NEG_ID), ņłśņØĄļźĀ ņ¦ĆņåŹņä▒(POS_RC/NEG_RC), ņ¢æĻ│╝ ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ä Ļ░£ņøöņØś ņ░©ņØ┤(NPOS_NEG), ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄ(CGO), ĻĘĖļ”¼Ļ│Ā ĻĖ░ņŚģĒŖ╣ņä▒ ņÜöņØĖņØä ļÅģļ”Įļ│ĆņłśļĪ£ ĒĢ£ ĒÜĪļŗ©ļ®┤ ļČäņäØņØ┤ļŗż. Ļ░ü ņŚ┤ņØĆ ĒÜĪļŗ©ļ®┤ ĒÜīĻĘĆļČäņäØ ĒÜīĻĘĆĻ│äņłśņØś ņŗ£Ļ│äņŚ┤ ĒÅēĻĘĀĻ│╝ ņĪ░ņĀĢļÉ£ R2 ļź╝ ļéśĒāĆļéĖļŗż. Ēæ£ļ│ĖņØĆ 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņןĻ│╝ ņĮöņŖżļŗźņŗ£ņןņŚÉ ņāüņןļÉ£ ļ│┤ĒåĄņŻ╝ ņżæņŚÉņä£ ņŻ╝ļŗ╣ Ļ░ĆĻ▓®ņØ┤ 500ņøÉļ│┤ļŗż Ēü░ ņŻ╝ņŗØņØ┤ļŗż. ***, **, *ļŖö Ļ░üĻ░ü 1%, 5%, 10% ņ£ĀņØśņłśņżĆņŚÉņä£ ņ£ĀņØśĒĢ©ņØä Ēæ£ņŗ£ĒĢ£ļŗż. Ļ┤äĒśĖ ņĢłņØś ņł½ņ×ÉļŖö Newey and West(1987) t-ĒåĄĻ│äļ¤ēņØ┤ļŗż.

ņóģĒĢ®ĒĢśļ®┤, ļ│Ė ņĀłņŚÉņä£ļŖö ĻĖ░ņĪ┤ņØś ņŚ░ĻĄ¼ņŚÉ ļö░ļØ╝ ņłśņØĄļźĀ ņ¦ĆņåŹņä▒Ļ│╝ ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ņØ┤ ĻĖ░ļīĆņłśņØĄļźĀņŚÉ ļ»Ėņ╣śļŖö ņśüĒ¢źņØä ĒÖĢņØĖĒĢ£ļŗż. ĒżĒŖĖĒÅ┤ļ”¼ņśż ļČäņäØņØä ĒåĄĒĢ┤ ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒Ļ│╝ ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░ä ļÅÖņĢł ņ¢æĻ│╝ ņØīņØś ņøöļ│äņłśņØĄļźĀņØä Ļ░Ćņ¦ä ļŗ¼ņØś Ļ░£ņłśņØś ņ░©ņØ┤ļź╝ ĒåĄņĀ£ĒĢ£ Ēøä COņÖĆ ņŻ╝ņŗØņłśņØĄļźĀĻ░äņØś Ļ┤ĆĻ│äļź╝ ļéśĒāĆļéĖļŗż. ņČöĻ░ĆņĀüņØĖ ļ│Ćņłśļź╝ Ļ│ĀļĀżĒĢ£ ĒøäņŚÉļÅä COļŖö ņŻ╝ņŗØņłśņØĄļźĀĻ│╝ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ┤ĆĻ│äļź╝ Ļ░Ćņ¦äļŗż. ļŹö ļéśņĢäĻ░Ć, Fama-Macbeth ĒÜĪļŗ©ļ®┤ ļČäņäØņØä ĒåĄĒĢ┤ ņłśņØĄļźĀ ņ¦ĆņåŹņä▒Ļ│╝ ņČöĻ░ĆņĀü ņÜöņØĖņØä ļÅÖņŗ£ņŚÉ Ļ│ĀļĀżĒĢśņŚ¼ COĻ│╝ ĒÜĪļŗ©ļ®┤ņĀü ņŻ╝ņŗØņłśņØĄļźĀ Ļ░äņØś Ļ┤ĆĻ│äļź╝ ĒÖĢņØĖĒĢ£ļŗż. ņÜ░ļ”¼ļŖö Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØ┤ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļ»Ėņ╣śļŖö ņśüĒ¢źņØĆ ņłśņØĄļźĀ ņ¦ĆņåŹņä▒Ļ│╝ ņĀĢļ│┤ņØś ļČłņŚ░ņåŹņä▒ņŚÉ ņØśĒĢ£ ĒśäņāüņØ┤ ņĢäļŗśņØä ņ×¼ĒÖĢņØĖĒĢ£ļŗż. ļśÉĒĢ£, COļŖö ĒÜĪļŗ©ļ®┤ņĀü ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ņ£ĀņØśĒĢ£ ņ¢æņØś ņśłņĖĪļĀźņØä Ļ░Ćņ¦ÉņØä ņĀ£ņŗ£ĒĢ£ļŗż.

4.5 ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄĻ│╝ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ

Grinblatt and Han(2005)ņŚÉ ļö░ļź┤ļ®┤ ļööņŖżĒżņ¦Ćņģś ĒÜ©Ļ│╝ņŚÉ ņØśĒĢ£ Ļ▒░ļלļĪ£ ņØĖĒĢ┤ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄ (unrealized capital gains)ņØ┤ ņ”ØĻ░ĆĒĢĀņłśļĪØ ņŻ╝Ļ░ĆļŖö ņĀĆĒÅēĻ░ĆļÉ£ļŗż. ņŻ╝Ļ░ĆĻ░Ć ņĀĆĒÅēĻ░ĆļÉśļ®┤ ņŻ╝ņŗØņłśņØĄļźĀņØĆ ņ”ØĻ░ĆĒĢśļŖö ĒśäņāüņØ┤ ļ░£ņāØĒĢ£ļŗż. ņØ┤ņÖĆ ļ░śļīĆļĪ£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņåÉņŗżņØ┤ ņ”ØĻ░ĆĒĢĀņłśļĪØ ņŻ╝Ļ░ĆļŖö Ļ│ĀĒÅēĻ░ĆļÉśņ¢┤ ņŻ╝ņŗØņłśņØĄļźĀņØĆ ļé«ņĢäņ¦äļŗż. Grinblatt and Han(2005)ļŖö ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØś ļīĆņÜ®ļ│ĆņłśĻ░Ć ļ¬©ļ®śĒģĆ ņĀäļץņØś ņłśņØĄņä▒ņØä ņ░ĮņČ£ĒĢśļŖö ĒĢĄņŗ¼ļ│ĆņłśļØ╝Ļ│Ā ņŻ╝ņןĒĢśļ®░ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĒåĄņĀ£ĒĢ£ Ēøä Ļ│╝Ļ▒░ņłśņØĄļźĀņØ┤ ĒÜĪļŗ©ļ®┤ņĀüņ£╝ļĪ£ ņłśņØĄļźĀņØä ņśłņĖĪĒĢśņ¦Ć ļ¬╗ĒĢ©ņØä ļ│┤ņØĖļŗż. Oh and Hahn(2012)ņØĆ Grinblatt and Han(2005)ņŚÉ ļö░ļØ╝ ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņןņŚÉņä£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄĻ│╝ ņŻ╝ņŗØņłśņØĄļźĀņØĆ ņ¢æņØś Ļ┤ĆĻ│äļź╝ ĒÖĢņØĖĒĢ£ļŗż. ĻĘĖ Ļ▓░Ļ│╝, ĻĄŁļé┤ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØ┤ ļ¬©ļ®śĒģĆ ĒśäņāüņØä ņäżļ¬ģĒĢ©ņØä ļ│┤ņØĖļŗż. Oh and Hahn(2013)ņŚÉ ļö░ļź┤ļ®┤ ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņŚÉ ļö░ļźĖ ĒśäņāüņØĆ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØś ļČĆĒśĖņŚÉ ļö░ļØ╝ ļ╣äļīĆņ╣ŁņĀüņ£╝ļĪ£ ļ░£ņāØĒĢśļ®░ ļ»Ėņ▓śļČä ņØ┤ņØĄņØ┤ ņ¢æņłśņØĖ Ļ▓ĮņÜ░ņŚÉļ¦ī ļÜ£ļĀĘĒĢ£ ĒśäņāüņØ┤ ļéśĒāĆļé£ļŗż.

ņĀ£ 4ņן ņĀ£ŌĆģ2ņĀłņŚÉņä£ COņĀäļץņØĆ ļ¬©ļ®śĒģĆ ņĀäļץņØś ņłśņØĄļźĀļĪ£ ĻĖ░ņżĆņĪ░ņĀĢ ĒĢ£ ĒøäņŚÉļÅä ņŚ¼ņĀäĒ׳ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. Oh and Hahn(2012)ņŚÉ ļö░ļź┤ļ®┤ ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØ┤ ļ¬©ļ®śĒģĆ ĒśäņāüņØä ņäżļ¬ģĒĢśĻ│Ā, ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄĻ│╝ ņŻ╝ņŗØņłśņØĄļźĀĻ░äņØś ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ┤ĆĻ│äĻ░Ć ņĪ┤ņ×¼ĒĢ£ļŗż. ļö░ļØ╝ņä£ ļ│Ė ņĀłņŚÉņä£ļŖö ļ¬©ļ®śĒģĆ ĒśäņāüņØś ĒĢĄņŗ¼ļ│ĆņłśņØĖ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄĻ│╝ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæĻ░äņØś Ļ┤ĆĻ│äļź╝ ņé┤ĒÄ┤ļ│Ėļŗż. <Ēæ£ 7>ņØĆ ļŗżļ│Ćļ¤ē ĒżĒŖĖĒÅ┤ļ”¼ņśż ļČäņäØņØä ĒåĄĒĢśņŚ¼ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĒåĄņĀ£ĒĢ£ Ēøä Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØ┤ ņ£Āņ¦ĆļÉśļŖöņ¦Ć ņŚ¼ļČĆļź╝ ņĀ£ņŗ£ĒĢ£ļŗż.

(10)

<Ēæ£┬Ā7>

ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄĻ│╝ COņĀäļץ

ņØ┤ Ēæ£ļŖö ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ņĀ£ņ¢┤ĒĢ£ Ēøä COņĀäļץņØś ņłśņØĄņä▒ņØä ļéśĒāĆļéĖļŗż. Ēī©ļäÉ AļŖö ļ¦żņøö ļ¦É ņŗØ (10)ņ£╝ļĪ£ ļÅäņČ£ļÉ£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĻĖ░ņżĆņ£╝ļĪ£ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢśĻ│Ā, Ļ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØä COņŚÉ ļö░ļØ╝ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļĪ£ ļéśļłäņ¢┤ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĒåĄņĀ£ĒĢ£ COņĀäļץņØś ņłśņØĄņä▒ņØä ļéśĒāĆļéĖļŗż. Ēī©ļäÉ BļŖö ļ╣äļīĆņ╣ŁņĀü ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņŚÉ ļö░ļźĖ COņĀäļץņØä ĒÖĢņØĖĒĢ£ļŗż. ļ¦żņøö ļ¦É ņ¢æņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄ(POS_G)Ļ│╝ ņØīņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄ(NEG_G)ņØä Ļ░Ćņ¦ä ņŻ╝ņŗØņØä ļéśļłäĻ│Ā, Ļ░ü ĻĘĖļŻ╣ņŚÉņä£ ņżæņĢÖĻ░ÆņØä ĻĖ░ņżĆņ£╝ļĪ£ 2ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢśņŚ¼ Ļ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØä ļŗżņŗ£ COļź╝ ĻĖ░ņżĆņ£╝ļĪ£ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢ£ļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØĆ 6Ļ░£ņøö(K=6)ņØ┤Ļ│Ā, ņłśņØĄļźĀņØĆ ĒŹ╝ņä╝ĒŖĖ ļŗ©ņ£äļŗż. Ēæ£ļ│ĖņØĆ 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņןĻ│╝ ņĮöņŖżļŗźņŗ£ņןņŚÉ ņāüņןļÉ£ ļ│┤ĒåĄņŻ╝ ņżæņŚÉņä£ ņŻ╝ļŗ╣ Ļ░ĆĻ▓®ņØ┤ 500ņøÉļ│┤ļŗż Ēü░ ņŻ╝ņŗØņØ┤ļŗż. ***, **, *ļŖö Ļ░üĻ░ü 1%, 5%, 10% ņ£ĀņØśņłśņżĆņŚÉņä£ ņ£ĀņØśĒĢ©ņØä Ēæ£ņŗ£ĒĢ£ļŗż. Ļ┤äĒśĖ ņĢłņØś ņł½ņ×ÉļŖö Newey and West(1987) t-ĒåĄĻ│äļ¤ēņØ┤ļŗż.

Ēī©ļäÉ A: ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄĻ│╝ CO

ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØĆ ņŗØ (10)Ļ│╝ Ļ░Öļŗż. Grinblatt and Han(2005)ņØĆ ņŻ╝ļ│ä ņŻ╝ņŗØļŹ░ņØ┤Ēä░ļź╝ ņØ┤ņÜ®ĒĢśņŚ¼ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä Ļ│äņé░ĒĢ£ļŗż. ļ│Ė ņŚ░ĻĄ¼ņŚÉņä£ļŖö Ļ│╝Ļ▒░ 5ļģäņØś ņŻ╝ļ│ä ņŻ╝ņŗØļŹ░ņØ┤Ēä░ļź╝ ņØ┤ņÜ®ĒĢśņŚ¼ ļÅäņČ£ĒĢśļÉś An et al.(2019)ņŚÉņä£ ņĀ£ņŗ£ĒĢ£ ļ░öņÖĆ Ļ░ÖņØ┤ ļ¦ż ņøö ļ¦łņ¦Ćļ¦ē ņŻ╝ņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ļ¦ż ņøö ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņ£╝ļĪ£ ļéśĒāĆļéĖļŗż. gļŖö ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØ┤ļ®░, PļŖö ņŻ╝ņŗØĻ░ĆĻ▓®ņØ┤ļŗż. RņØĆ ĻĖ░ņżĆĻ░ĆĻ▓®ņØ┤ļ®░, VļŖö ņŻ╝ļ│ä ĒÜīņĀäņ£©(ņŻ╝ļ│ä Ļ▒░ļלļ¤ē/ņŻ╝ļ│ä ļ░£Ē¢ēņŻ╝ņŗØņłś)ņØś ĒÅēĻĘĀņØ┤ļŗż. kļŖö Ļ│╝Ļ▒░ ņŻ╝ņŗØĻ░ĆĻ▓®ņØś Ļ░Ćņżæņ╣śļĪ£ ĒĢ®ņØ┤ 1ņØ┤ ļÉśļŖö ņāüņłśņØ┤ļŗż.

<Ēæ£ 7>ņØś Ēī©ļäÉ AļŖö ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĒåĄņĀ£ĒĢ£ Ēøä COņĀäļץņØś ņłśņØĄņä▒ņØä ļéśĒāĆļéĖļŗż. ļ¦żņøö ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĻĖ░ņżĆņ£╝ļĪ£ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ļéśļłäĻ│Ā Ļ░ü ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØä COņŚÉ ļö░ļØ╝ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢ£ļŗż. ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄ ĒżĒŖĖĒÅ┤ļ”¼ņśż 1(5)ņØĆ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØ┤ Ļ░Ćņן ļé«ņØĆ(ļåÆņØĆ) ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ņåŹĒĢ£ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ņØśļ»ĖĒĢ£ļŗż. ĻĘĖ Ļ▓░Ļ│╝ CO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØĆ ļ¬©ļōĀ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉņä£ ļŗ©ņĪ░ļĪŁĻ▓ī ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦äļŗż. ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĻĖ░ņżĆņ£╝ļĪ£ ĒĢ£ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉņä£ COņĀäļץņØś ņłśņØĄļźĀ Ļ░üĻ░ü 0.870%, 0.840%, 0.587%, 0.346%, 0.683%ņØ┤ļ®░ ĒżĒŖĖĒÅ┤ļ”¼ņśż 4ļź╝ ņĀ£ņÖĖĒĢśļ®┤ ļ¬©ļæÉ ĒåĄĻ│äņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢśļŗż. ļ¦ż ņøö ĒżĒŖĖĒÅ┤ļ”¼ņśż 4ņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄ ĒÅēĻĘĀĒĢ£ Ļ▓░Ļ│╝ 0.115ļĪ£ 0ņŚÉ Ļ░ĆĻ╣īņÜ┤ ņ¢æņłśļØ╝ļŖö Ļ▓āņØä ĒÖĢņØĖĒĢ£ļŗż. ĒżĒŖĖĒÅ┤ļ”¼ņśż 3Ļ│╝ 5ņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØś ĒÅēĻĘĀĻ│╝ ļ╣äĻĄÉĒĢ£ Ļ▓░Ļ│╝ 0ņŚÉ Ļ░ĆĻ╣īņÜ┤ ņ¢æņłśņØ╝ Ļ▓ĮņÜ░ COņĀäļץņØś ņ£ĀņØśņä▒ņØ┤ ĒĢśļØĮĒĢ£ļŗż. ņÜ░ļ”¼ļŖö ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØś ļ╣äļīĆņ╣ŁņĀüņØĖ ĒÜ©Ļ│╝ļź╝ ļ®┤ļ░ĆĒ׳ ĒÖĢņØĖĒĢśĻĖ░ ņ£äĒĢśņŚ¼ ņ¢æņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄĻ│╝ ņØīņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņŚÉ ļö░ļźĖ COņĀäļץņØä ļČäņäØĒĢ£ļŗż.

Oh and Hahn(2013)ņŚÉ ļö░ļź┤ļ®┤ ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØś ļČĆĒśĖņŚÉ ļö░ļźĖ ņŻ╝ņŗØ ņłśņØĄļźĀņŚÉ ļīĆĒĢ┤ ļ╣äļīĆņ╣ŁņĀü ĒÜ©Ļ│╝Ļ░Ć ņĪ┤ņ×¼ĒĢ£ļŗż. ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØ┤ ņØīņłśņØ╝ Ļ▓ĮņÜ░ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆĒĢ£ ņśüĒ¢źņØ┤ ļ»Ėļ»ĖĒĢśļŗż. ĒĢśņ¦Ćļ¦ī, ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØ┤ ņ¢æņłśņØ╝ Ļ▓ĮņÜ░ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØ┤ ņ”ØĻ░ĆĒĢĀņłśļĪØ ņŻ╝Ļ░ĆĻ░Ć ņĀĆĒÅēĻ░ĆļÉśĻ│Ā ĻĖ░ļīĆņłśņØĄļźĀņØ┤ ņ”ØĻ░ĆĒĢśļŖö ĒśäņāüņØ┤ Ļ┤ĆņĖĪļÉ£ļŗż. ņØīņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØś ņśüĒ¢źņØ┤ ņĢĮĒĢśļŗżļ®┤, ņØīņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĒåĄņĀ£ĒĢ£ Ļ▓ĮņÜ░ņŚÉ ņ¢æņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĒåĄņĀ£ĒĢ£ Ļ▓ā ļ│┤ļŗż ļåÆņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦ł Ļ▓āņØ┤ļØ╝Ļ│Ā ņśłņāüĒĢĀ ņłś ņ׳ļŗż. ņÜ░ļ”¼ļŖö ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØś ļ╣äļīĆņ╣ŁņĀü ĒÜ©Ļ│╝ļź╝ ĒåĄņĀ£ĒĢśĻĖ░ ņ£äĒĢ┤ ļŗżņØīĻ│╝ Ļ░ÖņØ┤ ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢ£ļŗż. ļ©╝ņĀĆ, ņ¢æņØś(ņØīņØś) ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä Ļ░Ćņ¦ĆļŖö ņŻ╝ņŗØņØä POS_G(NEG_G)ļĪ£ ļČäļźśĒĢ£ļŗż. POS_G(NEG_G)ļź╝ ņżæņĢÖĻ░Æ ĻĖ░ņżĆņ£╝ļĪ£ ĒĢśņ£äĒżĒŖĖĒÅ┤ļ”¼ņśżņÖĆ ņāüņ£ä ĒżĒŖĖĒÅ┤ļ”¼ņśżļĪ£ ļéśļłäĻ│Ā Ļ░üĻ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśż 1Ļ│╝ 2ļź╝ ļČĆņŚ¼ĒĢśņŚ¼ ņ┤Ø 4Ļ░£ņØś ĻĘĖļŻ╣ņØä ĻĄ¼ņä▒ĒĢ£ļŗż. 4Ļ░£ņØś ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉņä£ ļŗżņŗ£ COļź╝ ĻĖ░ņżĆņ£╝ļĪ£ 5ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢ£ Ļ▓░Ļ│╝ļź╝ ļéśĒāĆļéĖļŗż. <Ēæ£ 7>ņØś Ēī©ļäÉ BņŚÉ ļö░ļź┤ļ®┤, Ļ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉņä£ļŖö COņĀäļץņØś ņłśņØĄļźĀņØ┤ 0.868%, 0.991%, 0.269%, 0.778%ņØ┤ļŗż. POS_GņØś ĒżĒŖĖĒÅ┤ļ”¼ņśż 1ņØä ņĀ£ņÖĖĒĢśļ®┤ ļ¬©ļæÉ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØ┤ļŗż. ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØ┤ ņØīņłśņØ╝ Ļ▓ĮņÜ░ ļ¬©ļæÉ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØĆ ļŗ©ņĪ░ļĪŁĻ▓ī ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦Ćņ¦Ćļ¦ī POS_GņØś ĒżĒŖĖĒÅ┤ļ”¼ņśż 1ņŚÉņä£ļŖö COĻ░Ć ņ”ØĻ░ĆĒĢ©ņŚÉ ļö░ļØ╝ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØ┤ ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦Ćņ¦Ć ņĢŖļŖöļŗż. Ēī©ļäÉ AņÖĆ ņ£Āņé¼ĒĢśĻ▓ī POS_GņØś ĒżĒŖĖĒÅ┤ļ”¼ņśż 1ņŚÉ ņåŹĒĢ£ ņŻ╝ņŗØņØś ĒÅēĻĘĀ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØĆ 0.097ļĪ£ 0ņŚÉ Ļ░ĆĻ╣īņÜ┤ ņ¢æņłśņØ┤ļŗż. ņ”ē, Oh and Hahn(2013)ņŚÉņä£ ņ¢ĖĻĖēĒĢ£ ļ░öņÖĆ Ļ░ÖņØ┤ ņØīņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä Ļ░Ćņ¦ł Ļ▓ĮņÜ░ ņ¢æņØś ļ»ĖņŗżĒśä ņØ┤ņØĄņØä Ļ░Ćņ¦ł ļĢīļ│┤ļŗż ļ¼┤ļ╣äņÜ® ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØ┤ ļåÆļŗż. ņÜ░ļ”¼ļŖö ļ¬©ļ®śĒģĆ ņĀäļץņØś ņłśņØĄļźĀņŚÉ ĒĢĄņŗ¼ņÜöņåīņØĖ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØ┤ COļź╝ ņČ®ļČäĒ׳ ņäżļ¬ģĒĢśņ¦Ć ļ¬╗ĒĢśņ¦Ćļ¦ī, ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØ┤ 0ņŚÉ Ļ░ĆĻ╣īņÜ┤ ņ¢æņłśņØ╝ Ļ▓ĮņÜ░ļŖö ņśłņÖĖĻ░Ć ļÉ£ļŗżļŖö ņé¼ņŗżņØä ĒÖĢņØĖĒĢ£ļŗż. ļö░ļØ╝ņä£ Oh and Hahn(2013)Ļ│╝ ņ£Āņé¼ĒĢśĻ▓ī ĒĢ£ĻĄŁ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØ┤ 0ņŚÉ Ļ░ĆĻ╣īņÜ┤ ņ¢æņØś Ļ░ÆņØ╝ ļĢī ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØś ļ╣äļīĆņ╣ŁņĀü ĒÜ©Ļ│╝Ļ░Ć ļéśĒāĆļé£ļŗż. ĒĢśņ¦Ćļ¦ī, <Ēæ£ 6>ņØś Fama-Macbeth ĒÜĪļŗ©ļ®┤ļČäņäØņŚÉņä£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĒåĄņĀ£ĒĢ£ ļ¬©ĒśĢ 7ņØś Ļ▓ĮņÜ░, COļŖö ĒÜĪļŗ©ļ®┤ņĀü ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆĒĢśņŚ¼ ņ£ĀņØśĒĢ£ ņ¢æņØś ņśłņĖĪļĀźņØä Ļ░Ćņ¦Ćņ¦Ćļ¦ī ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØĆ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ņ£ĀņØśĒĢ£ ņśüĒ¢źņØä ļ»Ėņ╣śņ¦Ć ļ¬╗ĒĢ£ļŗż.

ņóģĒĢ®ĒĢśļ®┤, Grinblatt and Han(2005)ņŚÉ ņØśĒĢ┤ ļ¬©ļ®śĒģĆ ĒśäņāüņØś ņłśņØĄņä▒ņØä ņ░ĮņČ£ĒĢśļŖö ĒĢĄņŗ¼ņÜöņØĖņØĖ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØĆ COņĀäļץņØä ņČ®ļČäĒ׳ ņäżļ¬ģĒĢśņ¦Ć ļ¬╗ĒĢ£ļŗż. ļ╣äļīĆņ╣ŁņĀü ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØś ĒÜ©Ļ│╝ļź╝ ĒÖĢņØĖĒĢ£ Ļ▓░Ļ│╝, ņØīņØś ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņŚÉņä£ COņĀäļץņØĆ ņāüļīĆņĀüņ£╝ļĪ£ ļŹö ļåÆņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ļö░ļØ╝ņä£ ļ»ĖņŗżĒśä ņ×Éļ│ĖņØ┤ņØĄņØä ĒåĄņĀ£ĒĢ£ Ēøä Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØĆ ņŻ╝ņŗØņłśņØĄļźĀņŚÉ ļīĆņ▓┤ņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś ņśüĒ¢źņØä ņżĆļŗż.

4.6 ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ(residual continuing overreaction)Ļ│╝ ņŻ╝ņŗØņłśņØĄļźĀ

Blitz et al.(2011)ņØĆ ņ×öņŚ¼ļ¬©ļ®śĒģĆ(residual momentum) ņĀäļץĻ│╝ ļ¬©ļ®śĒģĆ ņĀäļץņØä ļ╣äĻĄÉ ļČäņäØĒĢ£ļŗż. ņ×öņŚ¼ļ¬©ļ®śĒģĆņØĆ ĻĖ░ņĪ┤ņØś ļ¬©ļ®śĒģĆļ│┤ļŗż Ēü¼Ļ│Ā ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦Ćļ®░ ĻĖłņ£Ąņ£äĻĖ░ ĻĖ░Ļ░ä ļÅÖņĢł ņØ╝Ļ┤ĆļÉ£ ņä▒Ļ│╝ļź╝ Ļ░Ćņ¦äļŗż. ļśÉĒĢ£, ņ×öņŚ¼ļ¬©ļ®śĒģĆņØĆ 1ņøö ĒÜ©Ļ│╝(January effect) Ļ░ÖņØĆ Ļ│äņĀłņĀü Ēī©Ēä┤ņŚÉ Ļ┤ĆņŚ¼ ļ░øņ¦Ć ņĢŖļŖöļŗż. Blizt et al.(2020)ņØĆ Blitz et al.(2011)Ļ│╝ Gutierrez and Prinsky(2007)ņŚÉ ļö░ļØ╝ Ļ│Āņ£Ā ļ¬©ļ®śĒģĆ(idiosyncratic momentum)ņØä ļÅäņČ£ĒĢ£ļŗż. Ļ│Āņ£Āļ¬©ļ®śĒģĆņØĆ ņĀäĒåĄņĀü ļ¬©ļ®śĒģĆ ņĀäļץņŚÉ ņØśĒĢ┤ ņäżļ¬ģļÉśņ¦Ć ņĢŖļŖö ĒśäņāüņØ┤ļ®░, ļ¬©ļ®śĒģĆņØś ņØ┤ņāüņłśņØĄļźĀ ĒśäņāüņØä ņäżļ¬ģĒĢśļŖö ņÜöņØĖņ£╝ļĪ£ ĒåĄņĀ£ĒĢ£ ĒøäņŚÉļÅä ņŻ╝ņŗØņłśņØĄļźĀņØä ĒÜĪļŗ©ļ®┤ņĀüņ£╝ļĪ£ ņäżļ¬ģĒĢ£ļŗż. ļśÉĒĢ£, ņŗ£ņןņāüĒā£ņÖĆ ņŗ£ņןļÅÖĒā£(market dynamics)ņÖĆ Ļ┤ĆļĀ©ļÉ£ Ēł¼ņ×Éņ×ÉņØś Ļ│╝ņŗĀĻ│╝ Ļ│╝ņ×ēļ░śņØæņØĆ Ļ│Āņ£Āļ¬©ļ®śĒģĆņØś ņłśņØĄļźĀņØä ņäżļ¬ģĒĢĀ ņłś ņŚåļŗżĻ│Ā ņŻ╝ņןĒĢ£ļŗż.

ļ│Ė ņĀłņŚÉņä£ ņ×öņŚ¼ņłśņØĄļźĀņØä ņØ┤ņÜ®ĒĢśņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ņČöņĀĢĒĢśĻ│Ā, ņŻ╝ņŗØņłśņØĄļźĀĻ│╝ ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ(residual continuing overreaction, RCO)ņØś Ļ┤ĆĻ│äļź╝ ĒÖĢņØĖĒĢ£ļŗż. ņ×öņŚ¼ņłśņØĄļźĀ(residual return)ņØĆ Blitz et al.(2011)Ļ│╝ Gutierrez and Prinsky(2007)ņŚÉ ĻĖ░ļ░śņØä ļæö Blizt et al.(2020)ņŚÉ ļö░ļØ╝ ļÅäņČ£ļÉ£ļŗż. Ļ│╝Ļ▒░ 36Ļ░£ņøö ņŻ╝ņŗØļŹ░ņØ┤Ēä░ņÖĆ ņŗØ (3)ņØä ņØ┤ņÜ®ĒĢśņŚ¼ Ļ░ü ĒÜīĻĘĆĻ│äņłśļź╝ ĻĄ¼ĒĢśĻ│Ā, ņŗØ (11)ņŚÉ ļö░ļØ╝ ņ×öņŚ¼ņłśņØĄļźĀ(╬Ąi,t)ņØä ļÅäņČ£ĒĢ£ļŗż.

ņÜ░ļ”¼ļŖö ņŗØ (1)ņŚÉņä£ ņé¼ņÜ®ļÉ£ ņłśņØĄļźĀņØä ņ×öņŚ¼ņłśņØĄļźĀļĪ£ ļ│ĆĻ▓ĮĒĢśņŚ¼ ņŗØ (12)ņŚÉ ļö░ļØ╝ ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ē (RSV)ņØä ļÅäņČ£ĒĢ£ļŗż. ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ(RCO)ņØĆ ņŗØ (12)ņŚÉņä£ ļÅäņČ£ļÉ£RSVņØä ņŗØ (13)ņŚÉ ļīĆņ×ģĒĢśņŚ¼ Ļ│äņé░ĒĢ£ļŗż.

VOLi,tļŖötņøöņØśiļ▓łņ¦Ė ņŻ╝ņŗØņØś ņøöļ│äĻ▒░ļלļīĆĻĖłņØ┤Ļ│Ā, Ļ░ü ļŗ¼ņØś ņØ╝ļ│ä ņŻ╝ņŗØĻ▒░ļלļ¤ēņŚÉ ņóģĻ░Ćļź╝ Ļ│▒ĒĢ£ Ļ░ÆņØś ĒĢ®ņ£╝ļĪ£ ņĀĢņØśĒĢ£ļŗż. ╬Ąi,tļŖötņøöņØśiļ▓łņ¦Ė ņ×öņŚ¼ņłśņØĄļźĀņØ┤ļŗż. ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ(RCO)ņØĆ ņŗØ (13)ņŚÉ ļö░ļØ╝ ļÅäņČ£ĒĢ£ļŗż.

RSVi,tļŖötņøöņØśiļ▓łņ¦Ė ņŻ╝ņŗØņØś ļČĆĒśĖĒÖöļÉ£ Ļ▒░ļלļ¤ēņØ┤ļŗż. RCOi,tļŖö ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØä ļéśĒāĆļé┤ļŖö ņĖĪņĀĢņ╣śļĪ£ ņé¼ņÜ®ĒĢ£ļŗż.

<Ēæ£ 8>ņØĆ RCOņÖĆ ņŻ╝ņŗØņłśņØĄļźĀĻ░äņØś Ļ┤ĆĻ│äļź╝ ļéśĒāĆļéĖļŗż. <Ēæ£ 8>ņŚÉ ļö░ļź┤ļ®┤ RCOļŖö ņŻ╝ņŗØņłśņØĄļźĀĻ│╝ ņ¢æņØś Ļ┤ĆĻ│äņŚÉ ņ׳ļŗż. ņØīņØś RCOļź╝ Ļ░Ćņ¦ĆļŖö ĒżĒŖĖĒÅ┤ļ”¼ņśż(Low 1)ļŖö ļŗżļźĖ ĒżĒŖĖĒÅ┤ļ”¼ņśżņŚÉ ļ╣äĒĢśņŚ¼ ņāüļīĆņĀüņ£╝ļĪ£ ļé«ņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦ĆĻ│Ā, ņ¢æņØś RCOļź╝ Ļ░Ćņ¦ĆļŖö ĒżĒŖĖĒÅ┤ļ”¼ņśż(High 10)ļŖö ņāüļīĆņĀüņ£╝ļĪ£ ļåÆņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØ┤ 6Ļ░£ņøö, 9Ļ░£ņøö, 12ņøöņØ╝ Ļ▓ĮņÜ░ ļ¼┤ļ╣äņÜ® ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØĆ 0.562%, 0.598%, 0.459%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļ®░, RCOĻ░Ć ņ”ØĻ░ĆĒĢ©ņŚÉ ļö░ļØ╝ ņŻ╝ņŗØņłśņØĄļźĀņØ┤ ļŗ©ņĪ░ļĪŁĻ▓ī ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦äļŗż. ņ”ē, ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØĆ ņŻ╝ņŗØņłśņØĄļźĀĻ│╝ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ┤ĆĻ│äņŚÉ ņ׳ņ£╝ļ®░ ņŚ░Ļ░ä 5%ņŚÉņä£ 7%ņé¼ņØ┤ņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ņØ┤ļŖö ņŚ¼ņĀäĒ׳ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀ ņØ┤ņ¦Ćļ¦ī, <Ēæ£ 2>ņØś COņĀäļץņŚÉ ļ╣äĒĢśņŚ¼ ļé«ņØĆ ĒÅēĻĘĀņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż.

<Ēæ£┬Ā8>

RCO ĻĖ░ļ░ś ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀ

ļ¦żņøö ļ¦É ņ×öņŚ¼ņłśņØĄļźĀļĪ£ ļÅäņČ£ļÉ£ RCOļź╝ ĻĖ░ņżĆņ£╝ļĪ£ ĻĄ¼ņä▒ĒĢ£ 10Ļ░£ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ļ│┤ņ£ĀņłśņØĄļźĀņØ┤ļŗż. ĒżĒŖĖĒÅ┤ļ”¼ņśż ĻĄ¼ņä▒ĻĖ░Ļ░äņØĆ 12Ļ░£ņøö(J=12)ņØ┤ļ®░, Ļ░ü ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ 6Ļ░£ņøö, 9Ļ░£ņøö, ĻĘĖļ”¼Ļ│Ā 12Ļ░£ņøö ļ│┤ņ£ĀĒĢ£ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØ┤ļŗż. CAPMņØĆ ņŗ£ņןņÜöņØĖņ£╝ļĪ£ ņ£äĒŚśņØä ņĪ░ņĀĢĒĢ£ ņłśņØĄļźĀņØ┤ļŗż. ļ│┤ņ£ĀĻĖ░Ļ░äņØĆ Ļ░üĻ░ü 6Ļ░£ņøö(K=6), 9Ļ░£ņøö (K=9), 12Ļ░£ņøö(K=12)ņØ┤ļŗż. ņłśņØĄļźĀņØĆ ĒŹ╝ņä╝ĒŖĖ ļŗ©ņ£äļŗż. Ēæ£ļ│ĖņØĆ 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ņ£ĀĻ░Ćņ”ØĻČī ņŗ£ņןĻ│╝ ņĮöņŖżļŗźņŗ£ņןņŚÉ ņāüņןļÉ£ ļ│┤ĒåĄņŻ╝ ņżæņŚÉņä£ ņŻ╝ļŗ╣ Ļ░ĆĻ▓®ņØ┤ 500ņøÉļ│┤ļŗż Ēü░ ņŻ╝ņŗØņØ┤ļŗż. ***, **, *ļŖö Ļ░üĻ░ü 1%, 5%, 10% ņ£ĀņØśņłśņżĆņŚÉņä£ ņ£ĀņØśĒĢ©ņØä Ēæ£ņŗ£ĒĢ£ļŗż. Ļ┤äĒśĖ ņĢłņØś ņł½ņ×ÉļŖö Newey and West(1987) t-ĒåĄĻ│äļ¤ēņØ┤ļŗż.

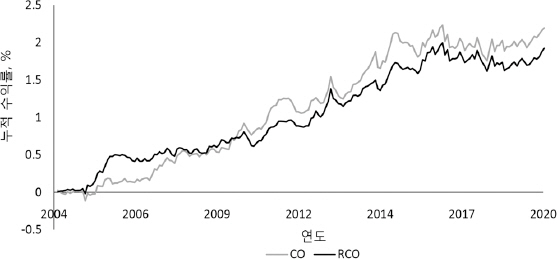

<ĻĘĖļ”╝ 3> COņĀäļץĻ│╝ RCOņĀäļץņØś ļłäņĀüņłśņØĄļźĀņØä ļéśĒāĆļéĖļŗż. 2004ļģäņŚÉļŖö ļæÉ ņĀäļץņØ┤ ļ╣äņŖĘĒĢ£ ņłśņżĆņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ļ░śļ®┤, 2005ļģäņŚÉ COņĀäļץņØ┤ ņØīņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦Ćļ®┤ņä£ ļæÉ ņĀäļץņØś ņłśņØĄļźĀņŚÉ ņ░©ņØ┤Ļ░Ć ļ░£ņāØĒĢśĻ│Ā RCOņĀäļץņØ┤ ļŹö ļåÆņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. 2010ļģäļīĆņŚÉ ļōżņ¢┤Ļ░Ćļ®┤ņä£ COņĀäļץņØś ņłśņØĄļźĀņØ┤ ļŹö ļåÆņĢäņ¦ĆĻ│Ā 2020ļģäĻ╣īņ¦Ć ņØ┤ņ¢┤ņ¦ĆļŖö Ļ▓āņØä ĒÖĢņØĖĒĢ£ļŗż. Ļ▓░Ļ│╝ņĀüņ£╝ļĪ£ COņĀäļץņØś ņłśņØĄļźĀņØĆ 2.1% ņłśņżĆņØä ņ£Āņ¦ĆĒĢśĻ│Ā, RCOņĀäļץņØĆ 1.9% ņĀĢļÅäņØś ņłśņØĄļźĀņØä ņ£Āņ¦ĆĒĢ£ļŗż. ņØ┤ļź╝ ĒåĄĒĢśņŚ¼, ĻĖ░ņĪ┤ņØś Ļ▓░Ļ│╝ņÖĆ ņ£Āņé¼ĒĢśĻ▓ī ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ COņĀäļץĻ│╝ RCOņĀäļץ ļ¬©ļæÉ ņ£ĀņØśĒĢ£ ņ¢æņØś ņłśņØĄļźĀņØä Ļ░Ćņ¦ÉņØä ĒÖĢņØĖĒĢ£ļŗż.

<ĻĘĖļ”╝┬Ā3>

COņÖĆ RCOņĀäļץņØś ļłäņĀüņłśņØĄļźĀ

ņØ┤ ĻĘĖļ”╝ņØĆ COņÖĆ RCOĻ░Ć Ļ░Ćņן ļåÆņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņŚÉņä£ Ļ░Ćņן ļé«ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņØä ļ║Ć ļ¼┤ļ╣äņÜ® ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ļłäņĀüņłśņØĄļźĀņØä ļéśĒāĆļéĖļŗż. COļŖö Ļ│╝Ļ▒░ 12Ļ░£ņøöņØś ņłśņØĄļźĀņØä ĻĖ░ņżĆņ£╝ļĪ£ ļÅäņČ£ļÉśļ®░, RCOļŖö CAPMļ¬©ĒśĢņØä ņé¼ņÜ®ĒĢśņŚ¼ ņČöņĀĢļÉ£ ņ×öņŚ¼ņłśņØĄļźĀņØä ĻĖ░ņżĆņ£╝ļĪ£ ņĀĢņØśļÉ£ļŗż. ņłśņØĄļźĀņØĆ ĒŹ╝ņä╝ĒŖĖ ļŗ©ņ£äļŗż. Ēæ£ļ│ĖņØĆ 2000ļģä 1ņøöļČĆĒä░ 2020ļģä 6ņøöĻ╣īņ¦Ć ņ£ĀĻ░Ćņ”ØĻČīņŗ£ņןĻ│╝ ņĮöņŖżļŗźņŗ£ņןņŚÉ ņāüņןļÉ£ ļ│┤ĒåĄņŻ╝ ņżæņŚÉņä£ ņŻ╝ļŗ╣ Ļ░ĆĻ▓®ņØ┤ 500ņøÉļ│┤ļŗż Ēü░ ņŻ╝ņŗØņØ┤ļŗż.

ņÜ░ļ”¼ļŖö ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæ(RCO)Ļ│╝ ņ×öņŚ¼ļ¬©ļ®śĒģĆ ņĀäļץņØś ņłśņØĄņä▒ņØä ļ╣äĻĄÉĒĢśĻĖ░ ņ£äĒĢśņŚ¼ ņĀ£ 4ņן ņĀ£2ņĀłĻ│╝ Ļ░ÖņØ┤ ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØä ĒÖĢņØĖĒĢ£ļŗż. ĻĖ░ņĪ┤ņØś ņŚ░ĻĄ¼ņŚÉ ņØśĒĢśļ®┤, ļ»ĖĻĄŁ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ņ×öņŚ¼ļ¬©ļ®śĒģĆņØ┤ ņłśņØĄļźĀ ļ¬©ļ®śĒģĆņĀäļץņŚÉ ļ╣äĒĢśņŚ¼ 2ļ░░Ļ░Ćļ¤ē ļåÆņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ņÜ░ļ”¼ļŖö ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ņ×öņŚ¼ļ¬©ļ®śĒģĆņØś ņśüĒ¢źņØä ĒÖĢņØĖĒĢśĻ│Ā, ņ×öņŚ¼ Ļ│äņåŹņĀü Ļ│╝ņ×ēļ░śņØæņØś ņśüĒ¢źņŚÉ Ļ┤ĆņŚ¼ĒĢśļŖöņ¦Ć ņŚ¼ļČĆļź╝ ĒÖĢņØĖĒĢ£ļŗż. ņ×öņŚ¼ļ¬©ļ®śĒģĆņØĆ Blitz et al.(2011)ņŚÉ ļö░ļØ╝t-12ņøöļČĆĒä░t-2ņøöņØś ņ×öņŚ¼ņłśņØĄļźĀņØä Ēæ£ņżĆĒÖöĒĢ£ Ļ░ÆņØ┤ļŗż.

<Ēæ£ 9>ļŖö RCOņÖĆ ņ×öņŚ¼ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀĻ│╝ ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØ┤ļŗż. RCO ĒżĒŖĖĒÅ┤ļ”¼ņśżļŖö ņŗØ (13)ņŚÉ ļö░ļØ╝ ļÅäņČ£ļÉ£ RCOļź╝ ĻĖ░ņżĆņ£╝ļĪ£ 10ļČäņ£äņłś ĒżĒŖĖĒÅ┤ļ”¼ņśżļź╝ ĻĄ¼ņä▒ĒĢ£ļŗż. RCO ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņ×öņŚ¼ļ¬©ļ®śĒģĆ ņĪ░ņĀĢņłśņØĄļźĀņØĆ ļ¦żņøö ļ¦É RCOļź╝ ĻĖ░ņżĆņ£╝ļĪ£ ĻĄ¼ņä▒ļÉ£ 10Ļ░£ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņłśņØĄļźĀņŚÉņä£ ĻĘĖ ņŻ╝ņŗØņØ┤ ņåŹĒĢ£ ņ×öņŚ¼ļ¬©ļ®śĒģĆ ĒżĒŖĖĒÅ┤ļ”¼ņśż ņłśņØĄļźĀņØä ļ║Ć Ļ░ÆņØ┤ļŗż. ņ×öņŚ¼ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņøöļ│äņłśņØĄļźĀņØĆ 0.918%ņŚÉņä£ 1.479%ļĪ£ ļŗ©ņĪ░ļĪŁĻ▓ī ņ”ØĻ░ĆĒĢśļŖö Ēī©Ēä┤ņØä Ļ░Ćņ¦Ćļ®░, RCOĻ░Ć Ļ░Ćņן ļåÆņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņÖĆ Ļ░Ćņן ļé«ņØĆ ĒżĒŖĖĒÅ┤ļ”¼ņśżņØś ņ░©ņØ┤ļŖö 0.562%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļŗż. ņ×öņŚ¼ļ¬©ļ®śĒģĆ ņĪ░ņĀĢņłśņØĄļźĀņØĆ -0.172%ņŚÉņä£ 0.090%ņØ┤ļ®░, ņ░©ņØ┤Ļ░ÆņØĆ 0.262%ļĪ£ ĒåĄĻ│äņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢśļŗż. RCOņĀäļץņØĆ <Ēæ£ 8>Ļ│╝ <ĻĘĖļ”╝ 3>ņŚÉņä£ ļéśĒāĆļāłļō»ņØ┤ COņĀäļץņŚÉ ļ╣äĒĢśņŚ¼ ļé«ņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦Ćņ¦Ćļ¦ī ĻĘĖ Ļ░ÆņØĆ Ļ▓ĮņĀ£ņĀüņ£╝ļĪ£ļéś ĒåĄĻ│äņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ļŗż. ņ×öņŚ¼ļ¬©ļ®śĒģĆ ņĀäļץņØś ņłśņØĄļźĀņØĆ 0.399%ļĪ£ ņ£ĀņØśĒĢ£ ņ¢æņØś Ļ░ÆņØ┤ņ¦Ćļ¦ī ļ¬©ļ®śĒģĆ ņĀäļץņŚÉ ļ╣äĒĢśņŚ¼ ļé«ņØĆ ņłśņØĄļźĀņØä Ļ░Ćņ¦äļŗż. ĒĢśņ¦Ćļ¦ī, RCOņĪ░ņĀĢ ņłśņØĄļźĀņŚÉ Ļ▓ĮņÜ░ ļÜ£ļĀĘĒĢ£ Ēī©Ēä┤ņØ┤ ņé¼ļØ╝ņ¦Ćļ®░ ĒåĄĻ│äņĀüņ£╝ļĪ£ ņ£ĀņØśĒĢśņ¦Ć ņĢŖļŗż. ņ×öņŚ¼ļ¬©ļ®śĒģĆ ņĀäļץņØĆ ĻĄŁļé┤ ņŻ╝ņŗØņŗ£ņןņŚÉņä£ ņłśņØĄļźĀ ļ¬©ļ®śĒģĆ ņĀäļץņŚÉ ļ╣äĒĢśņŚ¼ ņÜ░ņøöĒĢ£ Ļ▓░Ļ│╝ļź╝ Ļ░Ćņ¦Ćņ¦Ć ļ¬╗ĒĢ£ļŗż. ļŹö ļéśņĢäĻ░Ć, ņ×öņŚ¼ļ¬©ļ®śĒģĆ ņĀäļץņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀņØĆ RCOņŚÉ ņØśĒĢśņŚ¼ ĒåĄņĀ£ļÉśņ¢┤ ĻĘĖ ņśüĒ¢źņØ┤ ņé¼ļØ╝ņ¦äļŗż.

<Ēæ£┬Ā9>

RCO, ņ×öņŚ¼ļ¬©ļ®śĒģĆņØś ĻĖ░ņżĆņĪ░ņĀĢ ņłśņØĄļźĀ