1. 서론

2008년 금융위기 이후 주가의 하방위험(downside risk, 또는 왼쪽꼬리위험, left-tail risk)이 투자자의 기대수익률에 미치는 영향에 대해 여러 연구가 진행되어 왔다.1) Ang, Chen, and Xing(2006)은 하방베타(downside beta)가 큰 주식이 높은 위험프리미엄을 가짐을 보여주며, Bali et al.(2009), Chollette and Lu(2011), Huang et al.(2012), Kelly and Jiang(2014), Chabi-Yo et al.(2018) 등은 주가 급락위험(crash risk 또는 extreme downside risk)이 기대수익률과 유의한 양(+)의 관계를 가지며, 투자자가 급락위험에 민감한 주식에 대해 더 높은 위험프리미엄을 요구한다는 것을 잘 보여준다. 유사한 맥락에서 Bali et al.(2014)는 미국 주식시장에서 수익률 분포의 꼬리공분산위험에 대한 연간 위험프리미엄이 9% 수준으로 측정됨을 보여준다.2)

왼쪽꼬리위험에 대한 유의한 양(+)의 위험프리미엄을 보여주는 선행연구와는 달리 최근 Atilgan et al.(2020)은 미국과 G-10 국가의 주식시장을 대상으로 한 연구에서 VaR(value at risk)을 이용하여 측정한 왼쪽꼬리위험이 주식의 기대수익률과 유의한 음(-)의 관계를 갖는다는 결과를 보여주었다.3) 이러한 결과는 왼쪽꼬리위험과 기대수익률간의 관계에 대한 여러 기존 연구의 결과에 상반되는 것으로 많은 논쟁을 불러일으키고 이다. 이들은 이러한 결과가 투자자가 왼쪽꼬리위험의 지속성을 과소 평가하여 최근 큰 손실을 경험한 주식의 가격을 과대 평가하는 오류를 범하는 특성에서 기인한다고 주장한다. 즉, 최근에 큰 손실을 경험한 주식은 미래에도 그 손실을 지속하는 경향을 가져 주식수익률 분포에서 왼쪽꼬리 부분의 낮은 수익률은 미래에도 지속되는 특성(cross-sectional persistence)을 가지나, 투자자들이 이러한 위험을 과소평가하고 단기간에 평균회귀(mean reversion)할 것으로 예측하여 해당주식을 비싼 가격에 매입함으로써 손실을 보게 되는 현상이 지속된다는 것이다.4) 이들은 이러한 현상을 왼쪽꼬리모멘텀(left-tail momentum)이라 부르며, 이 현상은 개인투자자의 보유비중이 높고 투자자의 관심을 덜 받으며 차익거래에 제약이 더 많은 주식에서 더 강하게 발생한다는 결과를 보고한다.

해외 선진 주식시장뿐 아니라 한국 주식시장에서도 왼쪽꼬리위험과 주식수익률의 관계는 자산가격의 결정이나 자산배분 및 포트폴리오구성, 위험관리 등 재무금융의 핵심 영역을 구성하는 기본 요소이다. 또 VaR이나 ES(expected shortfall)로 측정되는 왼쪽꼬리위험은 학문적으로뿐만 아니라 실무적으로 활용도가 매우 높은 중요 요소이다. 본 연구는 Atilgan et al.(2020)의 연구를 토대로 하여 한국 주식시장에서의 왼쪽꼬리위험과 주식수익률간의 관계를 살펴보고, 왼쪽꼬리 모멘텀 현상이 존재하는지를 분석한다. 한국 주식시장은 미국 주식시장에 비해 개인투자자의 비중이 높고, 가격제한폭과 공매의 제약 등 차익거래제약이 더 큰 특성을 가진다. 이런 특성을 고려하면 미국 주식시장에서 보인 왼쪽꼬리모멘텀 현상이 우리 시장에서 더욱 강하게 나타날 것으로 예상할 수 있으며, 왼쪽꼬리모멘텀 현상은 우리 시장에서의 주식수익률 변동을 설명하는 한 특성이 될 수 있다. 그렇지만 저자가 알기에 우리 시장을 대상으로 왼쪽꼬리모멘텀 현상을 구체적으로 분석한 연구는 Cheon and Ban(2021)의 연구가 유일하다.5) 이들은 주가급락 위험프리미엄이 월평균 -2.29%에 달하며, 이러한 결과는 주가급락위험에 투자자들이 과소반응 하는 행태에 기인한다는 결과를 보여준다. 그러나 이들의 연구는 왼쪽꼬리모멘텀에 영향을 미칠 수 있는 변수들의 영향이 충분히 통제되지 않았다는 한계를 갖는다. 본 연구는 선행연구를 바탕으로 우리 시장에서 관련 영향변수들을 통제한 후에도 왼쪽꼬리모멘텀 현상이 유의하게 존재하는지를 엄밀하게 검증한다. 본 연구는 주로 서구시장을 대상으로 이루어진 왼쪽꼬리모멘텀 현상에 대한 연구(앞서 살펴본 것과 같이 선행연구는 일관된 결과를 보여주지 못하고 있다)에 더해 우리 시장에서의 결과를 제공하는 의미와 더불어, 국내시장을 대상으로 한 관련 연구가 매우 드문 현실에서 우리 시장에서의 왼쪽꼬리모멘텀의 존재 여부를 강건하게 검증한 결과를 제공한다는 점에서 후속연구에 의미있는 토대를 제공해줄 수 있을 것이다.

2000년 이후의 표본기간 동안 유가증권시장과 코스닥시장의 상장기업을 대상으로 한 본 연구의 결과는 왼쪽꼬리모멘텀 현상이 한국 주식시장에서도 강하게 나타남을 보여준다. 왼쪽꼬리 위험 측정치를 기준으로 10분위 포트폴리오를 구성하고 동일가중방법과 가치가중방법으로 구성한 (H-L) 무비용포트폴리오의 초과수익률을 Fama-French 3요인모형을 기준으로 측정한 경우 월평균 -0.67%~-0.73%(5분위 포트폴리오의 경우 -0.51%~-0.82%)의 값을 갖는다. 또 이러한 음(-)의 왼쪽꼬리모멘텀 현상은 왼쪽꼬리위험 척도인 VaR을 측정하는 백분위 수준의 변경이나 조건부 VaR(expected shortfall, ES)를 이용한 경우, 주식시장 상황의 변화를 고려한 경우, 그리고 왼쪽꼬리모멘텀 현상에 영향을 미칠 수 있는 주요 영향변수들을 통제한 후에도 전반적으로 유효하게 확인된다. 또 표본기간 동안에 관찰된 왼쪽꼬리모멘텀 현상은 우리 시장에서 기존의 Fama-French 3요인과는 독립적으로 주식수익률 변동을 설명하는 정보가치를 가짐을 보여준다.

본 연구의 구성은 다음과 같다. 제2장에서는 연구에 사용된 표본자료와 연구방법을 설명한다. 제3장에서는 왼쪽꼬리위험과 왼쪽꼬리모멘텀의 관계를 살펴보고, 제4장에서는 주식수익률에 영향을 미치는 기업특성변수들을 통제한 후의 왼쪽꼬리모멘텀에 대해 분석한다. 마지막으로 제5장에서는 연구의 요약과 시사점을 제시한다.

2. 표본자료와 연구방법

2.1 표본 자료와 기간

본 연구에 사용될 표본자료는 한국거래소가 개설하는 유가증권시장과 코스닥시장의 상장 및 상장 폐지된 모든 개별기업의 자료를 이용한다. 주식수익률은 FnGuide에서 제공하는 현금배당을 반영한 수정주가의 일별수익률 자료를 이용한다. 전체 표본기간(1999.07~2020.06)은 과거 포트폴리오 형성기간과 미래 보유기간으로 구성된 하위기간으로 구분된다. 하위기간은 수익률분포를 도출을 위한 12개월의 과거 형성기간과 포트폴리오 투자성과의 산출을 위한 1개월의 미래 보유기간으로 구성된다. 기간이동은 미래 보유기간이 겹치지 않는 방법(non- overlapping holding period method)을 따른다. 즉, 미래 보유기간 기준으로 하위기간은 2000년 7월부터 2020년 6월까지의 총 240가지이다.

분석에 포함될 개별주식은 다음의 조건을 충족하는 주식이다. 첫째, Fama and French(1992, 1993)에 따라 금융업에 속하는 개별주식은 제외하고, 기업규모와 장부-시장가치비율(비음(-)의 조건 포함) 산출이 가능한 주식들이다. 둘째, 각 하위기간에서 다음의 조건을 충족하는 개별주식을 선택한다: (1) 과거 형성기간과 미래 보유기간에서 모든 수익률 정보를 갖는 주식들, (2) 과거 형성기간에서 시장가치 산출을 위한 발행주식수와 가격 정보를 갖는 주식들, (3) 과거 형성기간의 주식수익률과 거래량 각각에서 50%이상 0이 아닌 의미 있는 자료를 갖는 주식들. 셋째, 위의 조건을 만족하는 주식들 중에서, 과거 형성기간 동안에 극단치에 의한 영향과 매우 작은 규모를 갖는 기업의 영향을 다음의 방법으로 줄인다: (1) Ang et al.(2006)과 같이, 과거 형성기간 동안의 일별 주식수익률의 변동성(표준편차)을 이용하여 구성된 20분위 포트폴리오에서 가장 높은 변동성을 갖는 상위 5%의 포트폴리오에 속한 개별주식들을 제외한다. (2) Hou et al.(2020)과 같이, 기업규모를 이용하여 구성한 20분위 포트폴리오에서 가장 작은 기업규모를 갖는 하위 5%의 포트폴리오에 속한 개별주식을 제외한다. 이상의 조건을 모두 충족하여 검증과정에 포함된 개별주식의 숫자는 첫 번째 하위기간(1999.07~2000.07)에서는 총 801개 주식 중에서 640개가, 마지막 하위기간(2019.06~2020.06)에서 총 1,962개 주식 중에서 1,717개 주식이 분석에 이용된다.

요인포트폴리오의 수익률인 시장위험프리미엄(RMRF), 규모프리미엄(SMB), 가치프리미엄 (HML)은 유가증권시장과 코스닥시장에 상장된 모든 주식들 중에서, 금융업과 기업규모와 장부가-시장가비율의 자료가 없는 주식들을 제외한 12월을 결산월로 갖는 기업의 주식들을 이용하여 생성한다. 무위험이자율은 통화안정증권(364일)의 이자율을 이용한다.

2.2 주요 변수의 측정과 기초통계량

2.2.1 왼쪽꼬리위험 지표: VaR

본 연구에서 분석하는 왼쪽꼬리모멘텀 현상은 과거 포트폴리오 형성기간의 수익률분포에서 극단적 손실 사건들에 기인해 왼쪽 꼬리부분에 위치한 수익률 정보가 미래 보유기간의 횡단면 주식수익률에 대해 예측력을 가짐을 의미한다. 이를 검증하기 위해 먼저 과거기간의 극단적 손실사건의 수익률정보는 과거 12개월 동안의 일별 주식수익률의 분포에서 신뢰수준 97.5%에 대한 VaR로 측정한다.

식 (1)에서 VaR은 확률변수 X의 누적분포함수(FX)가 주어진 (1- α)보다 큰 값들 중에서 가장 작은 값이다(식에서 inf는 가장 작은 값을 나타낸다). α는 유의수준으로 수익률분포의 꼬리부분 확률이다. 예를 들어 좌우대칭의 속성을 갖는 수익률분포에서 신뢰구간 95%를 가정하면, 유의수준은 왼쪽 꼬리부분과 오른쪽 꼬리부분이 각각 2.5%에 해당한다. 본 연구에서는 극단적 손실의 수익률이 위치하는 왼쪽 꼬리부분의 확률이 2.5%(α =2.5%)에 위치하는 VaR을 계산한다. 즉, VaR은 과거 12개월 일별 주식수익률의 백분위 2.5%에 위치하는 값이다. 여기서 과거 12개월은 검증월 직전월의 시장미시구조의 영향을 줄이기 위해 검증월(t)의 직전월(t-1)을 제외한 기간(-12, -2)으로 설정한다. 검증 편의를 위해 2.5% 백분위에 위치하는 VaR은 과거 형성기간 12개월의 거래일별 일별 주식수익률에 -1을 곱한 수익률을 이용하여 누적확률 97.5%에 해당하는 값을 구하는 방법을 이용한다. 한편, 검증결과의 강건성을 위해 유의수준 5%에 해당하는 신뢰수준 95% VaR과 유의수준 0.5%에 해당하는 신뢰수준 99.5% VaR, 그리고 신뢰수준 97.5%에 해당하는 조건부 VaR인 ES(expected shortfall)를 추가적으로 이용한다.

2.2.2 통제변수

본 연구에서는 왼쪽꼬리모멘텀 현상이 강건하게 존재하는지를 살펴보기 위해 주식수익률에 영향을 미치는 것으로 알려진 기업특성변수와 수익률분포의 속성을 나타내는 변수들을 통제한 후의 왼쪽꼬리모멘텀의 존재를 분석한다. 이변량 포트폴리오(bivariate portfolio)와 Fama and MacBeth(1973)의 횡단면회귀분석을 통해 왼쪽꼬리모멘텀 현상의 강건성 확인을 위해 선택한 통제변수는 4가지 유형의 총 12가지 변수이다.

첫째, 가격결정모형의 주요 요인들에 관련된 변수들인 시장베타, 기업규모, 장부-시장가치비율 이다. 시장베타(market beta, BETA)는 과거 12개월의 일별자료를 이용한 시장모형으로부터 산출된 회귀계수이다. 여기서 과거 12개월은 시장미시구조 효과를 통제하기 위하여 검증월(t)의 직전월(t-1)을 제외한 기간(-12, -2)이다. 기업규모(market capitalization, SIZE)는 직전월 (t-1)의 주식가격에 직전년도(y-1) 12월 말의 발행주식수를 곱하여 산출된 값의 로그변환값 (ln(SIZE))이다. 장부-시장가치 비율(book-to-market ratio, BM)은 직전년도(y-1)의 장부 가치를 시장가치로 나눈 값에 1을 더한 후의 로그변환값(ln(1+BM))이다. 장부가치는 직전년도 (y-1)의 총자본에서 우선주 자본금을 뺀 값이고, 시장가치는 직전년도(y-1)의 12월말 주식가격 에서 발행주식수를 곱한 값이다.

둘째, 과거기간 투자성과에 관련된 변수들인 모멘텀, 단기반전, 장기반전이다. 모멘텀(momentum; Jegadeesh and Titman, 1993)은 과거 형성기간 12개월에서 직전월(t-1)을 제외한 기간(-12, -2)의 기간성과(periodic returns)이다. 단기반전(short-term reversal; Jegadeesh, 1990)은 직전월(t-1)의 기간성과이다. 장기반전(long-term reversal; DeBondt and Thaler, 1985)은 과거 60개월에서 과거 13개월까지(-60, -13)의 기간성과이다.

셋째, 시장미시구조 관련변수인 비유동성, 고유변동성, MAX효과이다. 비유동성(il-liquidity, Amihud, 2002)은 직전월(t-1) 동안 거래일별 수익률 절대값을 거래금액으로 나눈 값들의 평균값이다. 분모와 분자의 크기 차이를 조정하기 위하여 거래일별로 산출된 값에 조정계수로 106을 곱한다. 고유변동성(idiosyncratic volatility; Ang et al., 2006)은 직전월(t-1)에서 Fama and French(1993)의 3요인모형으로부터 추정된 잔차수익률의 표준편차에 대한 월 전환 값이다. 직전월에서 0이 아닌 수익률 자료를 50% 이상 갖는 주식들을 이용한다. MAX효과(max effect; Bali et al., 2014)는 직전월(t-1) 기간에 가장 큰 값을 갖는 5가지 일별수익률의 평균값이다.

넷째, 수익률분포의 속성에 관련된 변수인 왜도, 고유왜도, 공왜도이다. 왜도(skewness)는 과거 형성기간(-12, -2)의 일별수익률 분포의 왜도이다. 고유왜도(idiosyncratic skewness; Boyer et al., 2010)는 직전월(t-1)에서 Fama and French(1993)의 3요인모형으로부터 추정된 잔차수익률을 이용하여 측정된 왜도이다. 공왜도(co-skewness; Harvey and Siddique, 2000)는 과거 형성기간(-12, -2)에서 개별주식 초과수익률을 시장 초과수익률의 제곱값에 대해 회귀 분석(OLS)하여 추정한 회귀계수이다.

2.2.3 주요 변수의 기초통계량과 상관관계

<표 1>에 신뢰수준 97.5% VaR(이하, LT-VaR)과 12가지 통제변수들에 대한 기초통계량을 나타내었다. 보고된 결과는 전체기간에서 240가지 하위기간별로 과거 형성기간에서 산출된 횡단면 변수들의 시계열 평균값을 나타낸다. 각 변수들의 평균, 표준편차, 왜도, 첨도, 최대값, 중위수, 최소값을 보고한다.

<표 1>

주요 변수들의 기초통계량

표는 전체기간에서 설정된 240가지 하위기간별로 과거 형성기간에서 산출된 주요 변수들의 기초통계량의 시계열 평균값을 나타낸다. Left-tail VaR(LT-VaR)은 과거 형성기간의 일별수익률에 -1을 곱해 구한 분포의 백분위 확률 97.5%에 해당하는 값이다. 보고된 주요 변수들은 첫째, 가격결정요인의 관련 변수인 시장베타(market beta), 기업규모(ln(SIZE)), 장부-시장가치비율(ln(1+BM)), 둘째, 과거기간 투자성과의 관련 변수들인 장기반전(long-reversal), 모멘텀(momentum), 단기반전(short-reversal), 셋째, 시장미시

구조 관련 변수들인 MAX효과(MAX effect), 비유동성(il-liquidity), 고유변동성(IVOL), 넷째, 수익률 분포의 관련 변수들인 왜도(skewness), 고유왜도(i-skewness), 공왜도(co-skewness)이다. 보고통계량은 각 변수별로 평균(ave.), 표준편차(stdev.), 왜도(skew.), 첨도(kurtosis), 최대값(max), 중위수(median), 최소값(min)이다.

<표 1>의 결과를 보면 대부분의 변수들이 안정적인 분포 특성을 갖는 것을 확인할 수 있다.6) 즉, 공왜도를 제외한 다른 변수들의 표준편차는 안정적인 수준이고, 왜도와 첨도는 비유동성을 제외한 경우 극단적인 치우침을 보이지 않으며 정규성에서 크게 벗어나지 않는 값을 보인다. 또한 평균과 중위수 간의 차이가 비유동성과 공왜도 변수를 제외하고 큰 차이가 없음을 보여 대부분 변수들이 갖는 분포의 대칭성과 중심화 경향이 극단치로부터 큰 영향을 받지 않음을 나타낸다. <표 1>에서 비유동성 변수가 갖는 기초통계량의 특이점은 변수의 산출과정에서 피할 수 없는 분모와 분자 간의 매우 큰 크기 차이에 기인한 것으로 볼 수 있다.

다음으로, <표 2>에 변수들간의 상관관계를 나타낸다. 상관계수는 240가지 하위기간별로 과거 형성기간에서 산출된 변수들 간의 상관관계에 대한 시계열 평균값이다.

<표 2>

주요 변수들 간의 상관관계

표는 전체기간에서 설정된 240가지 하위기간별 과거 형성기간에서 산출된 12가지 변수들 간의 상관관계에 대한 시계열 평균값을 나타낸다. 하위기간은 과거 형성기간 12개월(-12,-2)과 미래 보유기간 1개월로 구성되며, 기간이동은 미래 보유기간이 겹치지 않는 방법을 이용한다. 분석에 포함된 변수들은 다음과 같다: 백분위 확률 97.5%의 left-tail VaR (LT-VaR), 시장베타(market beta), 기업규모(ln(SIZE)), 장부-시장가치비율(ln(1+BM)), 모멘텀(momentum), 단기반전(short-reversal), 장기반전(long-reversal), 비유동성(il-liquidity), 고유변동성(IVOL), MAX효과(MAX effect), 왜도(skewness), 고유왜도(i-skewness), 공왜도(co-skewness).

<표 2>에서 LT-VaR와 12가지 통제변수들 간의 상관관계가 우려 할만큼 높은 수준이 아님을 확인할 수 있다. 즉, LT-VaR와의 관계에서 고유변동성(0.44), 왜도(0.4), 시장베타(0.34) 등이 상대적으로 높은 상관관계를 보이며, 기업규모(-0.24)와 장부-시장가치비율(-0.22)은 음(-)의 관계를 보인다. 통제변수들 간의 관계에서 왜도를 중심으로 과거 직전월(t-1)에서 측정된 변수들 간에 높은 상관관계를 보인다. 즉, 왜도와 높은 상관관계를 갖는 변수들은 고유변동성(0.91), MAX효과(0.47), 단기반전(0.56) 등이다. 이는 분포의 치우침 정도에 영향을 미치는 수익률 빈도가 직전월의 수익률 자료로부터 영향을 크게 받기 때문에 나타나는 결과로 해석된다. 이들 변수들이 LT-VaR와 갖는 상관관계를 고려할 때 이들 변수들 간의 높은 상관관계가 본 연구의 분석결과에 의미있는 영향을 미치지는 못할 것으로 판단한다.

3. 왼쪽꼬리위험과 왼쪽꼬리모멘텀

3.1 왼쪽꼬리위험과 포트폴리오 투자성과

왼쪽꼬리모멘텀 현상은 과거기간에 큰 폭의 손실을 경험한 주식들이 미래기간에 주식수익률의 평균회귀 경향에 의하여 정상적 수준의 수익률로 복귀할 것이라는 기대가 실현되지 않음에 따라 나타난 결과로 파악할 수 있다. 즉, 과거기간에 큰 손실을 경험한 주식들이 평균회귀 없이 미래 보유기간에도 나쁜 성과가 지속되는 현상이다. 높은 LT-VaR을 갖는 주식일수록 보다 극단적인 손실을 경험한 주식이므로, 왼쪽꼬리모멘텀은 과거기간에 높은 LT-VaR을 갖는 주식들이 낮은 LT-VaR을 갖는 주식들에 비해 미래 보유기간에도 계속하여 낮은 수익률을 갖는지를 확인함으로써 검증할 수 있다. 이를 살펴보기 위해 과거기간에 높은 LT-VaR을 갖는 주식들로 구성된 포트폴리오(H)를 매수하고, 과거기간에 낮은 LT-VaR을 갖는 주식들로 구성된 포트폴리오(L)를 매도하여 구성한 H-L 무비용 포트폴리오의 투자성과를 분석한다.

포트폴리오의 투자성과는 무위험수익률에 대한 초과수익률, CAPM에 대한 위험조정수익률, Fama and French(1993)의 3요인모형에 대한 위험조정수익률을 제시한다. 무위험수익률은 통화안정증권(364일)의 이자율을 이용하며, CAPM과 Fama-French 3요인모형에 사용되는 시장위험프리미엄, 규모프리미엄, 가치프리미엄의 수익률은 유가증권시장과 코스닥시장에서 거래되는 개별주식들을 이용하여 생성한다. 즉, 시장수익률은 개별주식에 대한 시장가치를 가중치로 한 가치가중 포트폴리오수익률을 산출하여 이용하고, 시장위험프리미엄은 산출된 시장수익률에서 무위험수익률을 뺀 값이다. 규모프리미엄과 가치프리미엄은 Fama and French(1993)의 기업규모와 장부-시장가치비율을 기준으로 구성한 2×3 포트폴리오에 따라 산출된 가치가중 포트폴리오 수익률을 이용한다.

<표 3>은 한국 주식시장에서 왼쪽꼬리모멘텀 현상이 존재하는지를 분석한 결과를 나타낸다. 표는 왼쪽꼬리위험의 크기에 따라 10분위 포트폴리오(decile)와 5분위 포트폴리오(quintile)를 가중치부여방법(동일가중, 가치가중)에 따라 구성한 포트폴리오의 검증결과를 함께 제시한다. LT-VaR은 과거 12개월의 형성기간에서 측정하고, 투자성과는 미래 1개월의 보유기간에서 측정한 값이다.

<표 3>

왼쪽꼬리위험과 포트폴리오의 투자성과

표는 전체기간에 있어서 하위기간별로 과거 LT-VaR을 기준으로 구성된 포트폴리오의 미래 보유기간의 투자성과를 나타낸다. 하위기간은 과거 형성기간 12개월(-12,-2)과 미래 보유기간 1개월로 구성되며, 기간이동은 미래 보유기간이 겹치지 않는 방법을 이용한다. 포트폴리오는 10분위(decile)와 5분위(quintile)의 2가지이다. 10분위 포트폴리오는 10가지 포트폴리오와 가장 높고(High) 가장 낮은(Low) 2가지 포트폴리오 간의 차이인 H-L 무비용 포트폴리오를 제시하고, 5분위 포트폴리오는 H-L 무비용 포트폴리오만을 구분 제시한다. 검증결과는 포트폴리오 수익률의 가중치부여방법에 따라 동일가중방법(Panel A)과 가치가중방법(Panle B)으로 구분 제시한다. 성과 측정치는 무위험수익률에 대한 초과수익률, CAPM과 Fama and French(1993)의 3요인모형에 대한 위험조정수익률의 3가지이다. 괄호안의 값은 Newey and West(1987, 1994)를 따라 자기상관과 이분산성을 조정한 t-통계량이다. ***, **, *는 각각 1%, 5%, 10% 수준에서 통계적으로 유의함을 의미한다.

<표 3>의 결과는 한국 주식시장에서 왼쪽꼬리모멘텀 현상이 유의하게 나타남을 보여준다. 과거기간에 극단적 손실로 인해 높은 LT-VaR을 갖는 주식들로 구성된 포트폴리오(H)는 미래 보유기간에 여전히 낮은 투자성과를 실현하는 반면에 과거기간에 상대적으로 낮은 LT-VaR을 갖는 주식들로 구성된 포트폴리오(L)는 미래 보유기간에 상대적으로 높은 투자성과를 실현한다. 따라서 높은 LT-VaR 포트폴리오를 매수하고 낮은 LT-VaR 포트폴리오를 매도하는 H-L 무비용 포트폴리오는 유의한 음(-)의 투자성과를 보인다. Fama-French 3요인모형을 기준으로 볼 때 10분위 기준 H-L 무비용 포트폴리오의 초과수익률은 동일가중방법의 경우 월평균 -0.67%, 가치가중방법의 경우 -0.73%이다(5분위 기준 H-L 무비용 포트폴리오의 경우 -0.51%와 -0.82%이다). 유의한 음(-)의 투자성과는 가중치부여방법(동일가중, 가치가중), 포트폴리오 구성방법(10분위, 5분위), 그리고 투자성과 측정치(무위험초과수익률, CAPM α, FF3 α)에 관계없이 동일하게 관찰된다.

또한 10분위 포트폴리오에서 미래 보유기간의 투자성과는 투자성과 측정치에 관계없이 전반적으로 높은 LT-VaR 포트폴리오(H)에서 낮은 LT-VaR 포트폴리오(L)로 단조증가하는 패턴을 보인다. 이는 <그림 1>에서 분명하게 확인된다. 그림에서 X축은 과거 형성기간의 LT-VaR을 나타내고 Y축은 미래 보유기간의 투자성과이다.

<그림 1>

과거기간의 왼쪽꼬리위험(LT-VaR)과 미래 투자성과 간의 관계

그림은 과거 형성기간의 LT-VaR과 미래 보유기간의 포트폴리오 투자성과를 산포도(scatter plot)를 이용하여 나타낸다. 그림에서 X축은 과거 형성기간의 LT-VaR이고, Y축은 미래 보유기간의 투자성과이다. 가중치 부여방법에 따라 동일가중방법(그림(a))과 가치가중방법(그림(b))으로 구분한다. 미래 보유기간 투자성과를 초과수익률(red ○), CAPM 위험조정수익률(green □), Fama and French(1993)의 3요인모형 위험조정수익률(blue △)로 구분·표시한다.

3.2 왼쪽꼬리위험 포트폴리오의 특성

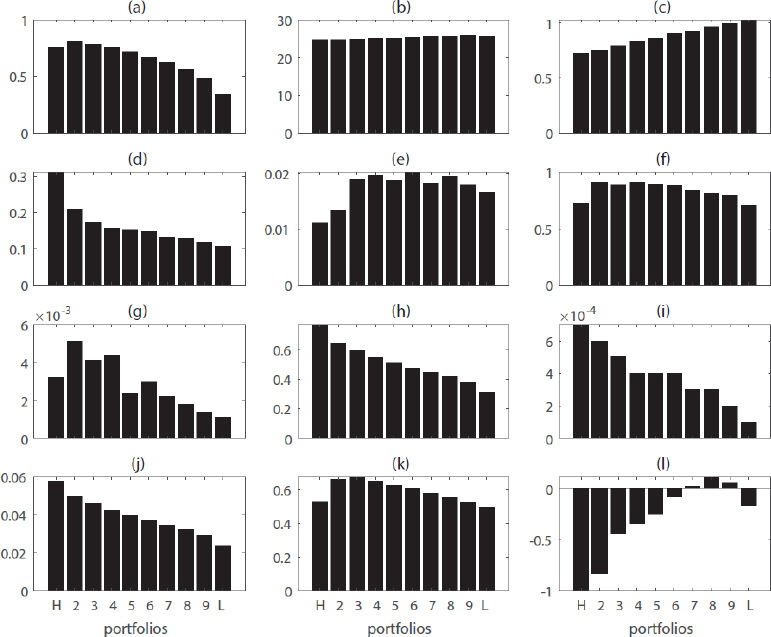

<표 4>는 왼쪽꼬리위험(LT-VaR)의 크기에 따라 주요 기업특성변수들의 크기에 어떤 변화가 있는지를 살펴본 결과이다. 표에 보고된 값은 각 하위기간별로 과거 형성기간에서 측정된 12가지 기업특성변수들에 대한 횡단면 측정치의 시계열 평균값이다. LT-VaR의 크기에 따라 구성된 10분위 포트폴리오는 모든 포트폴리오의 결과를 제시하고, 5분위 포트폴리오는 높은 포트폴리오 (H)와 낮은 포트폴리오(L)만을 제시한다.

<표 4>

LT-VaR와 주요 변수들의 특성

표는 전체기간에서 설정된 하위기간 각각에서 과거 LT-VaR을 기준으로 구성된 포트폴리오의 구성 주식들에 대한 12가지 변수들의 횡단면 측정치의 시계열 평균값을 나타낸다. 하위기간은 과거 형성기간 12개월(-12,-2)과 미래 보유기간 1개월로 구성되며, 기간이동은 미래 보유기간이 겹치지 않는 방법을 이용한다. 포트폴리오는 10분위와 5분위 2가지이다. 주요 변수들은 시장베타(market beta), 기업규모(ln(SIZE)), 장부-시장가치비율(ln(1+BM)), 모멘텀(momentum), 단기반전(short-reversal), 장기반전(long-reversal), 비유동성(il-liquidity), 고유변동성 (IVOL), MAX효과(MAX effect), 왜도(skewness), 고유왜도(i-skewness), 공왜도(co-skewness)이다.

3.3 왼쪽꼬리위험과 기업특성변수가 왼쪽꼬리모멘텀에 미치는 영향

이 절에서는 앞서 살펴본 왼쪽꼬리모멘텀 현상에 왼쪽꼬리위험과 기업특성변수가 미치는 영향을 회귀모형을 이용하여 분석한다. 이를 위해 각 개별주식의 미래보유기간(1개월)의 초과수익률을 종속변수로, 각 주식의 왼쪽꼬리위험 측정치인 LT-VaR와 기업특성변수들을 독립변수로 하는 회귀식을 구성한다. 회귀식은 Fama-Macbeth(1973)의 방법을 이용하여 추정한다.

식 (2)에서 VaRi,t는 과거기간(t)에서 주식 i의 왼쪽꼬리위험지표인 LT-VaR이며, FCi,t는 과거기간(t) 주식 i의 기업특성변수로 시장베타(market beta), 기업규모(ln(SIZE)), 장부-시장 가치비율(ln(1+BM)), 모멘텀(momentum), 단기반전(short-reversal), 장기반전(long-reversal), 비유동성(il-liquidity), 고유변동성(IVOL), MAX효과(MAX effect), 왜도(skewness), 고유 왜도(i-skewness), 공왜도(co-skewness)를 포함한다.

<표 5>는 식 (2)를 추정한 결과이다. 보고 수치는 하위기간별로 횡단면 회귀분석을 통해 추정된 회귀계수의 시계열 평균값이다. 횡단면 회귀분석은 5가지 모형으로 구분한다. 모형 1은 과거 형성기간의 LT-VaR을 이용한 단순회귀분석이다. 모형 2는 모형 1에 가격결정요인 관련 기업특성변수(시장베타, 기업규모, 장부-시장가치비율)를 포함한 회귀분석이고, 모형 3은 모형 2에 과거기간 투자성과 관련 기업특성변수(모멘텀, 단기반전, 장기반전)을 추가한 회귀분석이며, 모형 4는 모형 3에 시장미시구조 관련 기업특성변수(비유동성, 고유변동성, MAX효과)를 추가한 회귀분석이다. 그리고 모형 5는 모형 4에 수익률분포의 속성에 관련된 기업특성변수(왜도, 고유왜도, 공왜도)를 추가한 회귀분석이다.

<표 5>

왼쪽꼬리위험과 기업특성변수가 왼쪽꼬리모멘텀에 미치는 영향

표는 Fama and MacBeth(1973)의 횡단면 회귀분석으로부터 추정된 회귀계수의 시계열 평균을 나타낸다. 하위기간은 과거 형성기간 12개월(-12,-2)과 미래 보유기간 1개월로 구성되며, 기간이동은 미래 보유기간이 겹치지 않는 방법을 이용한다. 횡단면 회귀분석의 종속변수는 미래 보유기간 1개월의 개별주식수익률이고, 독립변수는 과거기간의 LT-VaR과 함께 과거기간에 측정된 통제변수들인 시장베타(market beta), 기업규모(ln(SIZE)), 장부-시장가치비율(ln(1+BM)), 모멘텀(momentum), 단기반전(short-reversal), 장기반전(long-reversal), 비유동성(il-liquidity), 고유변동성(IVOL), MAX효과(MAX effect), 왜도(skewness), 고유왜도(i-skewness), 공왜도(co-skewness)이다. 횡단면 회귀분석은 독립변수의 조합에 따라 5가지 모형으로 구분한다. 모형 1은 LT-VaR을 단일 독립변수로 포함하고, 모형 2는 가격결정요인에 관련된 3가지 변수(시장베타, 기업규모, 장부-시장가치비율)가 포함되고, 모형 3은 모형 2에 과거기간 투자성과에 관련된 3가지 변수(모멘텀, 단기반전 , 장기반전)이 추가되고, 모형 4는 모형에 시장미시구조 관련 3가지 변수(비유동성, 고유변동성, MAX효과)가 추가되고, 모형 5는 모형 4에 분포에 관련된 3가지 변수(왜도, 고유왜도, 공왜도)가 추가된 회귀분석이다. 괄호안의 값은 하위기간별로 추정된 회귀계수의 시계열 평균 값에 대해 Newey and West(1987, 1994)를 따라 자기상관과 이분산성을 조정한 t-통계량이다. ***, **, *는 각각 1%, 5%, 10% 수준에서 통계적으로 유의함을 의미한다.

<표 5>의 결과는 앞서 <표 3>에서 확인된 왼쪽꼬리모멘텀 현상이 주요 기업특성변수들을 통제한 경우에도 견고하게 존재함을 보여준다. 즉, 모형에 관계없이 과거 형성기간의 LT-VaR은 미래 보유기간(1개월)의 수익률에 대하여 유의한 음(-)의 관계를 갖는다. 이는 과거기간에 높은 (낮은) LT-VaR을 갖는 주식들은 미래 보유기간에서 낮은 (높은) 투자성과를 갖는다는 것을 의미한다. 기업특성변수들이 미래 보유기간의 수익률에 대해 갖는 관계는 선행연구에서 확인된 일반적인 결과와 일관성을 갖는다. 즉, 미래 기간의 수익률에 대해 가격결정요인 관련 변수들 중 기업규모는 유의한 음(-)의 관계를, 장부-시장가치 비율은 대부분 유의한 양(+)의 관계를 보이지만, 시장베타는 통계적 유의성을 보이지 않는다. 투자성과에 관련된 변수들 중 모멘텀은 유의한 양(+)의 관계를, 단기반전과 장기반전은 유의한 음(-)의 관계를 보여준다. 시장미시구조에 관련된 변수들 중 비유동성은 유의한 양(+)의 관계를, 고유변동성은 유의한 음(-)의 영향을 미친다. 다만, 수익률분포와 관련된 변수들인 고유왜도, 공왜도, 왜도와 MAX효과는 포트 폴리오의 초과수익률에 유의한 영향을 미치지 못한다.

3.4 왼쪽꼬리위험 포트폴리오의 미래 보유기간별 투자성과

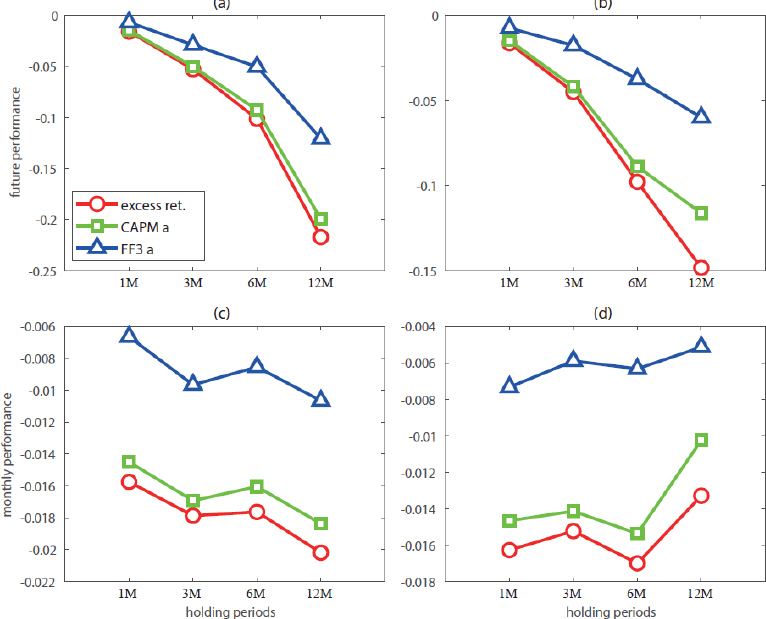

<표 6>은 미래 보유기간을 늘려갈 때 왼쪽꼬리모멘텀이 어떻게 변화하는지를 관찰한 결과이다. 미래 보유기간은 3개월(80가지 하위기간), 6개월(40가지 하위기간), 12개월(20가지 하위기간)의 3가지이고, 하위기간의 이동은 미래 보유기간이 겹치지 않는 방법을 따른다. 분석결과는 10분위 포트폴리오에 있어서 높은 LT-VaR을 갖는 주식들로 구성된 포트폴리오(H)와 낮은 LT-VaR을 갖는 주식들로 구성된 포트폴리오(L), 그리고 2가지 포트폴리오의 차이인 H-L 무비용 포트폴리오의 투자성과를 제시한다. 투자성과 측정치는 초과수익률, CAPM 위험조정수익률, FF3 위험조정수익률로 구분·제시한다.

<표 6>

미래 보유기간별 왼쪽꼬리위험 포트폴리오의 투자성과

표는 LT-VaR을 기준으로 구성된 포트폴리오의 미래 보유기간별 투자성과를 나타낸다. 하위기간은 과거 형성기간 12개월(-12, -2)과 미래 보유기간 3개월(Panel A), 6개월(Panel B), 12개월(Panel C)이다. 동일가중방법과 가치가중방법으로 LT-VaR를 기준으로 구성한 10분위 포트폴리오에서 가장 높은 LT-VaR을 갖는 포트폴리오(High)와 가장 낮은 LT-VaR을 갖는 포트폴리오(Low), 그리고 2가지 포트폴리오 간의 차이인 H-L 무비용 포트폴리오의 결과를 구분 제시한다. 투자성과 측정치는 무위험 수익률에 대한 초과수익률, CAPM과 Fama and French(1993)의 3요인모형에 대한 위험조정수익률의 3가지이다. 괄호안의 값은 Newey and West(1987, 1994)의 방법으로 자기상관과 이분산성을 조정한 t-통계량이다. ***, **, *는 각각 1%, 5%, 10% 수준에서 통계적으로 유의함을 의미한다.

<표 6>의 결과를 보면, 한국 주식시장에서 왼쪽꼬리모멘텀은 미래 보유기간 12개월까지 지속적으로 유의하게 나타난다. 동일가중방법의 경우, 투자성과 측정치에 관계없이 미래보유 기간이 길어질수록 H-L 무비용포트폴리오의 누적초과수익률은 커지며 유의한 값을 갖는다. Fama-French 3요인모형 초과수익률의 값을 기준으로 보면 3개월에서 12개월로 보유기간이 확대될 때 음(-)의 누적초과수익률은 -2.87%에서 -12.07%로 커진다. 가치가중방법의 경우도 미래보유기간 12개월의 FF3 위험조정수익률을 제외한 투자성과 측정치들은 미래보유기간 12개월까지 유의한 값을 보여주며, 음(-)의 누적초과수익률은 보유기간이 3개월에서 12개월로 늘어날 때 -1.76%에서 -5.99%로 확대된다. 미래 보유기간이 길어질수록 H-L 무비용포트 폴리오의 누적초과수익률이 지속적으로 더욱 큰 음(-)의 값을 갖는 결과는 <그림 3>에서 보다 분명하게 확인된다. 이러한 결과는 우리 시장에서 왼쪽꼬리모멘텀의 발생원인이 상당기간 해소되지 않고 지속됨을 의미한다.

<그림 3>

보유기간별 포트폴리오 투자성과 추이: 기간성과와 월별성과

그림은 LT_VaR에 따라 구성된 10분위 포트폴리오에 대한 H-L 무비용 포트폴리오의 보유기간별 기간성과와 월별성과의 추이를 나타낸다. 보유기간은 1개월, 3개월, 6개월, 12개월의 4가지이다. 그림 (a)와 (b)는 각 보유기간의 기간투자성과를 나타내고, 그림 (c)와 (d)는 각 보유기간의 기간투자성과를 월별투자성과로 일치시킨 전환 값을 나타낸다. 가중치부여방법에 있어서 동일가중방법은 그림 (a)와 (c)로 구분하고, 가치가중방법은 그림 (b)와 (d)로 구분·제시한다. 투자성과 측정치는 초과수익률(red ○), CAPM α (green □), FF3 α (blue △)로 구분한다.

3.5 강건성 검증

본 연구에서는 추가적으로 VaR 측정치에서 누적확률분포의 백분위 변경(95.0%, 99.5%)과 조건부 VaR(expected shortfall, LT-ES)를 이용한 분석을 실시하였고7), 또한 과거기간과 미래기간의 주식시장의 상황변화를 고려한 왼쪽꼬리위험모멘텀 현상을 분석하였다. 논문의 지면관계상 검증결과를 본문에 모두 제시하지는 못하고 부록에 제시한다. 주요 결과를 간략하게 요약하여 보고한다.

첫째, 과거 형성기간 주식수익률에 대한 누적확률분포의 백분위 95.0% LT-VaR과 백분위 99.5% LT-VaR을 이용하여 구성한 10분위, 5분위 포트폴리오에 대한 검증결과이다(<부표 1>). 95% LT-VaR를 이용한 경우 동일가중방법과 가치가중방법 모두에서 H-L 무비용 포트폴리오의 투자성과는 초과수익률과 CAPM 위험조정수익률에서 유의한 음(-)의 값을 보이고 FF3 위험조정수익률에서는 음(-)의 값에 대한 유의성이 떨어진다. 반면, 99.5% LT-VaR를 이용한 경우 가치가중방법의 H-L 무비용 포트폴리오 투자성과는 10분위와 5분위 포트폴리오 에서 유의한 결과를 확인할 수 없다. 이는 백분위 99.5%에 해당하는 극단 값이 지나치게 끝 부분에 위치함에 따라 왼쪽꼬리위험에 대한 의미있는 정보를 담지 못하고 표본자료의 안정성이 떨어짐에 따른 영향으로 보인다. 예를 들어, 백분위 97.5% LT-VaR에 비교하여 백분위 99.5% LT-VaR은 평균에서 1.42배 높은 값을, 표준편차에서 1.18배 높은 값을 보인다.

둘째, 백분위 97.5% LT-ES를 이용한 검증결과는 LT-VaR의 경우에 비해 유의성이 떨어지는 결과를 보인다(<부표 2>). 즉, 동일가중방법은 H-L 무비용 포트폴리오의 유의한 음(-)의 투자성과를 보이지만, 가치가중방법은 LT-VaR에서와 같이 FF3 위험조정수익률의 유의성이 떨어지며 CAPM 위험조정수익률도 유의성이 약하다. 개별주식수익률에 대한 횡단면분석의 검증결과는 LT-VaR에서 확인된 검증결과와 다르지 않다(<부표 3>). 즉, 모형에 관계없이, 과거 형성기간 백분위 97.5% LT-ES는 미래 보유기간 개별주식수익률의 1개월 기간성과에 통계적으로 유의한 음(-)의 관계를 갖는다. 다만, LT-VaR에 비교하여 LT-ES의 경우 다소 작은 회귀계수 값과 다소 낮은 유의성을 보여준다.

셋째, 과거기간과 미래기간의 주식시장 상황의 변화가 왼쪾꼬리모멘텀에 미치는 영향을 분석한다. 시장상황의 변화유형은 Asem and Tian(2010)에 따라 지속적인 경우(유형1: 과거 상승→미래 상승, 유형4: 하락→하락)와 전환적인 경우(유형2: 상승→하락, 유형3: 하락→상승)로 구분한다. 분석결과, 지속적인 시장상황에서 (H-L) 무비용포트폴리오는 대부분의 성과측정치 에서 유의한 음(-)의 값을 보인다(<부표 4>). 동일가중방법은 95.0% LT-VaR, 97.5% LT-VaR, 97.5% LT-ES에서 지속적 시장상황인 유형1과 유형4에서 모든 투자성과 측정치가 유의한 음(-)의 값을 보이고, 99.5% LT-VaR은 유형4에서 유의적이다. 전환적 시장상황에서는 (H-L) 포트폴리오의 투자성과 측정치는 모두 음(-)의 값을 가지나 그 유의성은 떨어진다. 가치가중 방법의 경우 역시 대체적인 모습은 동일가중의 경우와 유사하다. 즉, 우리 시장에서 왼쪽꼬리 모멘텀 현상은 시장상황에 관계없이 확인되나 전환적인 시장상황보다는 지속적인 경우에 보다 분명하게 나타난다. 또 시장상황이 상승→하락의 특성을 보이는 경우 성과측정치의 유의성이 크게 떨어지며, 동일가중에 비해 가치가중 방법의 유의성이 떨어지는 모습을 보인다.

강건성 검증의 결과는 왼쪽꼬리모멘텀을 검증에서 가중치부여방법, 왼쪽꼬리위험을 측정하는 방법, 시장상황의 변화 특성 등이 왼쪽꼬리모멘텀의 크기와 통계적 유의성에 영향을 미칠 수 있음을 보여준다. 그러나 전반적으로 볼 때 앞서 97.5% 수준의 LT-VaR를 이용하여 확인한 음(-)의 왼쪽꼬리모멘텀 현상에 대한 기본적인 결과는 여전히 유효하게 확인된다.8)

4. 기업특성변수의 통제와 왼쪽꼬리모멘텀 현상

4.1 기업특성변수를 통제한 이변량 포트폴리오의 분석결과

본 절에서는 이변량 포트폴리오 분석을 이용하여 주요 기업특성변수들을 통제한 이후에도 한국 주식시장에서 왼쪽꼬리모멘텀이 존재하는지를 검증한다. 즉, 왼쪽꼬리모멘텀 현상에 영향을 미칠 수 있는 주요 변수들을 통제한 조건부왼쪽꼬리모멘텀(conditional left-tail momentum)의 존재를 확인하기 위해 종속적 이중정렬방법(dependently double-sorting method)을 이용한 이변량 포트폴리오 분석을 수행한다.

검증결과는 가격결정요인 관련 변수(시장베타, 기업규모, 장부-시장가치비율)을 통제한 결과(<표 7>), 과거기간의 투자성과 관련변수(모멘텀, 단기반전, 장기반전, MAX효과)을 통제한 결과(<표 8>)9), 수익률분포의 속성에 관련된 변수(왜도, 고유왜도, 공왜도)를 통제한 결과(<표 9>), 시장미시구조 관련변수(비유동성, 고유변동성)을 통제한 결과(<표 10>)로 구분하여 제시한다.

<표 7>

가격결정요인 관련변수를 통제한 경우의 왼쪽꼬리모멘텀

표는 가격결정요인 관련 기업특성변수를 통제변수로 하여 LT-VaR에 따라 구성한 포트폴리오의 미래 보유기간의 투자성과를 나타낸다. 하위기간은 과거 형성기간 12개월(-12, -2)과 미래 보유기간 1개월로 구성되며, 기간이동은 미래 보유기간이 겹치지 않는 방법을 이용한다. 통제변수는 시장베타(BETA, Panel A), 기업규모(SIZE, Panel B), 장부-시장가치비율(BM, Panel C)의 3가지이다. 포트폴리오는 먼저

통제변수 기준으로 상위 40%, 중위 20%, 하위40%의 3가지 주식집단으로 구분하고, 구분된 각 통제변수 주식집단 내에서 LT-VaR에 따라 5분위 포트폴리오를 구성한다. 검증결과는 가중치부여방법에 따라 상위 40% 주식집단(Top 40%)과 하위 40% 주식집단(Bottom 40%) 각각에서 LT-VaR에 따른 5분위 포트폴리오를 기준으로 구성한 (H-L) 무비용포트폴리오의 투자성과를 제시한다. 투자성과 측정치는

무위험수익률에 대한 초과수익률, CAPM과 Fama and French(1993)의 3요인모형에 대한 위험조정 수익률의 3가지이다. 괄호안의 값은 Newey and West(1987, 1994)의 방법에 따라 자기상관과 이분산성을 조정한 t-통계량이다. ***, **, *는 각각 1%, 5%, 10% 수준에서 통계적으로 유의함을 의미한다.

<표 8>

과거기간 투자성과 관련변수를 통제한 경우의 왼쪽꼬리모멘텀

표는 과거기간의 투자성과 관련변수를 통제변수로 하여 LT-VaR에 따라 구성한 포트폴리오의 미래 보유기간의 투자성과를 나타낸다. 하위기간은 과거 형성기간 12개월(-12, -2)과 미래 보유기간 1개월로 구성되며, 기간이동은 미래 보유기간이 겹치지 않는 방법을 이용한다. 통제변수는 장기반전(LREV, Panel A), 중기모멘텀(MOM, Panle B), 단기반전(SREV, Panel C), MAX효과(MAX, Panel D)의 4가지이다. 검증결과는 가중치부여방법에 따라 각 통제변수하의 상위 40% 주식집단(Top 40%)과 하위 40% 주식집단(Bottom 40%) 각각에서 LT-VaR에 따른 5분위 포트폴리오를 기준으로 구성한 (H-L) 무비용포트폴리오의 투자성과를 제시한다. 투자성과 측정치는 무위험수익률에 대한 초과수익률, CAPM과 Fama and French(1993)의 3요인모형에 대한 위험조정수익률의 3가지이다. 괄호안의 값은 Newey and West(1987, 1994)에 따라 자기상관과 이분산성을 조정한 t-통계량이다. ***, **, *는 각각 1%, 5%, 10% 수준에서 통계적으로 유의함을 의미한다.

<표 9>

수익률 분포속성 관련변수를 통제한 경우의 왼쪽꼬리모멘텀

표는 과거기간의 수익률분포 속성 관련변수를 통제변수로 하여 LT-VaR에 따라 구성한 포트폴리오의 미래 보유기간의 투자성과를 나타낸다. 왜도(SKEW, Panel A), 공왜도(coSKEW, Panle B), 고유왜도 (iSKEW, Panel C)의 3가지이다. 통제변수들은 왜도(SKEW, Panel A), 공왜도(coSKEW, Panle B), 고유왜도(iSKEW, Panel C)의 3가지이다. 검증결과는 가중치부여방법에 따라 각 통제변수하의 상위 40% 주식집단(Top 40%)과 하위 40% 주식집단(Bottom 40%) 각각에서 LT-VaR에 따른 5분위 포트폴리오를 기준으로 구성한 (H-L) 무비용포트폴리오의 투자성과를 제시한다. 투자성과 측정치는 무위험수익률에 대한 초과수익률, CAPM과 Fama and French(1993)의 3요인모형에 대한 위험조정수익률의 3가지이다. 괄호안의 값은 Newey and West(1987, 1994)에 따라 자기상관과 이분산성을 조정한 t-통계량이다. ***, **, *는 각각 1%, 5%, 10% 수준에서 통계적으로 유의함을 의미한다.

통제변수를 조건부로 하는 포트폴리오 구성과 평가 기준은 다음과 같다. 본 연구에서 채택한 포트폴리오 구조는 각 통제변수 기준 상위 40%와 하위 40%의 주식집단 내에서 과거 형성기간의 LT-VaR에 따라 5분위 포트폴리오를 구성하는 것이다. 즉, 종속적 이중정렬방법으로 3×5 포트폴리오를 구성한다. 검증결과는 가중치 부여방법(동일가중, 가치가중)별로 통제변수 상위 40%와 하위 40% 각각의 주식집단 내에서 LT-VaR에 따라 구성된 5분위 포트폴리오의 투자성과를 확인한다. 검증결과의 평가는 두가지 관점에서 해석한다. 첫 번째 관점은 상위집단의 결과와 하위집단의 결과를 평균한 H-L 무비용 포트폴리오 투자성과(Ave.)가 유의한 음(-)의 값을 갖는지 여부로 조건부왼쪽꼬리모멘텀의 존재를 평가한다. 즉, 높고 낮은 기업특성변수의 속성을 모두 반영한 경우의 왼쪽꼬리모멘텀 현상 존재여부를 해석한다. 두 번째 관점은 각 주식집단 내에서 H-L 무비용 포트폴리오가 유의한 음(-)의 투자성과를 갖는지의 여부에 따라 왼쪽꼬리모멘텀의 존재 여부를 평가한다. 즉, 높고 낮은 기업특성변수의 속성에 따라 왼쪽꼬리 모멘텀 현상의 존재가 상이한지 여부를 해석한다. H-L 무비용 포트폴리오의 투자성과는 무위험 초과수익률, CAPM 위험조정수익률, FF3 위험조정수익률로 구분·제시한다.

<표 7>에서 <표 10>에 제시한 분석결과는 전반적으로 관련변수들을 통제한 후에도 한국 주식시장에서 왼쪽꼬리모멘텀 현상이 유의하게 존재한다는 실증 증거를 보여준다. 통제변수의 유형별로 구분한 각각의 검증결과를 구체적으로 제시하면 다음과 같다.

<표 10>

차익거래 제약 관련 변수들을 통제한 경우의 왼쪽꼬리모멘텀

표는 과거기간의 차익거래 제약 관련 변수들을 통제변수로 하여 LT-VaR에 따라 구성된 포트폴리오의 미래 보유기간 투자성과를 나타낸다. 통제변수는 비유동성(ilLIQ, Panel A), 고유변동성(IVOL, Panle B)의 2가지이다. 검증결과는 가중치부여방법에 따라 각 통제변수하의 상위 40% 주식집단(Top 40%)과 하위 40% 주식집단(Bottom 40%) 각각에서 LT-VaR에 따른 5분위 포트폴리오를 기준으로 구성한 (H-L) 무비용포트폴리오의 투자성과를 제시한다. 투자성과 측정치는 무위험 초과수익률, CAPM과 3요인모형에 대한 위험조정수익률의 3가지이다. 괄호안의 값은 Newey and West(1987, 1994)에 따라 자기상관과 이분산성을 조정한 t-통계량이다. ***, **, *는 각각 1%, 5%, 10% 수준에서 통계적으로 유의함을 의미한다.

먼저, <표 7>은 가격결정요인 관련 기업특성변수(시장베타, 기업규모, 장부-시장가치비율)를 통제한 조건부 포트폴리오의 분석결과이다. 주요결과를 보면 첫째, 평균한 H-L 무비용 포트폴리오 투자성과(Ave.)에서 시장베타(Panel A)를 통제한 경우, 가중치 부여방법에 관계없이 H-L 무비용 포트폴리오에 대한 3가지 투자성과 측정치 모두는 유의한 음(-)의 값을 보인다. 기업규모(Panel B)와 장부-시장가치 비율(Panel C)을 통제한 경우, 동일가중방법 포트폴리오의 경우 모두 유의한 음(-)의 값을 보이고, 가치가중방법은 FF3 위험조정수익률을 제외한 다른 2가지 성과측정치에서 유의한 결과를 보인다. 둘째, 기업특성변수별로 상위 40%와 하위 40%로 구분된 주식집단에 대한 검증결과는, 시장베타(Panel A)의 경우, 동일가중방법은 상위 40% 주식집단에서 모든 투자성과 측정치가 유의한 음(-)의 값을 보이고, 가치가중방법은 하위 40% 주식집단에서 모두 유의한 음(-)의 투자성과를 보인다. 즉, 시장베타에 따라 구분된 주식집단에서 분명하게 어느 주식집단이 보다 강한 증거를 보인다고 보기 어렵다. 기업규모와 장부-시장가치 비율은 동일가중방법과 가치가중방법이 함께 유의한 증거를 보이는 것은 하위 40% 주식집단이다. 이러한 결과는 기업규모와 장부-시장가치비율이 낮은 주식집단에서 왼쪽꼬리모멘텀 현상이 보다 강하게 존재함을 의미한다.

<표 8>은 과거기간의 투자성과 관련변수들(장기반전, 모멘텀, 단기반전, MAX효과)을 통제한 검증결과이다. 첫째, 변수별로 전체집단 평균 투자성과(Ave.)를 기준으로 조건부 왼쪽꼬리 모멘텀의 존재에 대한 분석결과를 보면, 장기반전(Panel A), 모멘텀(Panel B), 단기반전(Panel C)의 경우 모두에서 동일가중방법에 의한 H-L 무비용 포트폴리오의 투자성과 측정치는 모두 유의한 음(-)의 값을 보이고, 가치가중방법은 FF3 위험조정수익률을 제외한 다른 2가지 성과 측정치에서 유의적인 결과를 보인다. MAX효과(Panel D)의 경우, FF3 위험조정수익률을 제외하고 동일가중방법과 가치가중방법 모두에서 H-L 무비용 포트폴리오는 유의한 음(-)의 투자성과를 보인다. 둘째, 기업특성변수별로 상위 40%와 하위 40%로 구분한 주식집단 각각에 대한 검증결과는, 장기반전의 경우, 주식집단 구분에 관계없이 동일가중방법은 유의한 음(-)의 H-L 무비용 포트폴리오 투자성과를 보이며, 동일가중방법과 가치가중방법 모두에서 상위집단에 비해 하위 40% 집단에서 보다 강한 결과를 보인다. 모멘텀의 경우, 가중치 부여방법에 관계없이 하위 40% 주식집단에서 유의한 음(-)의 H-L 무비용 포트폴리오의 투자성과를 보인다. 단기 반전과 MAX효과의 경우는 가중치 부여방법에 관계없이 상위 40% 주식집단에서 보다 크고 유의한 음(-)의 결과를 보인다. 한편, MAX효과의 하위 40% 주식집단은 왼쪽꼬리모멘텀의 존재와 대조적인 증거를 보인다. 즉, 하위 40% 집단에서 H-L 무비용 포트폴리오는 통계적으로 유의한 양(+)의 투자성과를 보여 낮은 MAX효과를 갖는 주식들의 경우 왼쪽꼬리모멘텀이 사라지는 결과를 보여준다. 이러한 결과는 모멘텀과 단기반전은 낮은 주식집단에서 왼쪽꼬리 모멘텀 현상이 보다 강하게 존재하고, MAX효과는 높은 주식집단에서 왼쪽꼬리모멘텀 현상이 보다 강하게 존재함으로 의미한다.

<표 9>는 수익률 분포속성 관련변수들(왜도, 공왜도, 고유왜도)을 통제한 조건부 포트폴리오에 대한 검증결과이다. 주요 결과를 보면, 첫째, 상위집단과 하위집단의 평균을 보면, 왜도(Panel A)의 경우, 가치가중방법에서의 FF3 위험조정수익률을 제외하고 H-L 무비용 포트폴리오는 모든 경우에 유의한 음(-)의 투자성과를 보인다. 공왜도(Panel B)와 고유왜도(Panel C)의 경우, 가중치 부여방법에 관계없이 H-L 무비용 포트폴리오에 대한 3가지 투자성과 측정치 모두는 유의한 음(-)의 값을 보인다. 둘째, 상위 40%와 하위 40%로 구분된 집단에서의 검증결과는, 왜도의 경우, 동일가중방법은 하위 40% 주식집단에서 모든 투자성과 측정치가 유의적인 음(-)의 값을 보이고, 가치가중방법은 상위 04% 주식집단에서 모두 유의한 음(-)의 투자성과를 보인다. 공왜도의 경우, 동일가중방법은 주식집단 구분에 관계없이, 가치가중방법은 하위 40% 주식집단 에서 유의한 음(-)의 값을 갖는다. 고유왜도의 경우에는 상위 40% 주식집단에서 가중치 부여 방법에 관계없이 유의한 증거를 보인다. 이러한 결과는 왜도는 높은 주식집단에서, 반면에 공왜도는 낮은 주식집단에서 왼쪽꼬리모멘텀 현상이 보다 강하게 존재함을 의미한다.

<표 10>은 차익거래 제약에 관련된 변수들(비유동성, 고유변동성)을 통제한 검증결과이다. 첫째, 전체집단에 대한 분석결과는, 비유동성(Panel A)의 경우, 투자성과 측정치는 음(-)의 값을 보이기는 하나 유의한 결과를 보여주지 못한다. 하지만 고유변동성(Panel B)의 경우, 가중치 부여방법에 관계없이 H-L 무비용 포트폴리오에 대한 3가지 투자성과 측정치 모두는 유의한 음(-)의 값을 보인다. 둘째, 변수별로 상위 40%와 하위 40%로 구분된 집단에 대한 분석결과는, 비유동성의 경우, 동일가중방법의 하위 40% 주식집단에서 유의한 음(-)의 성과 측정치를 보여주며, 고유변동성의 경우에는 가중치 부여방법에 관계없이 상위 40% 주식집단에서 유의한 음(-) 결과를 보인다. 한편, 비유동성 상위 40% 주식집단과 고유변동성 하위 40% 주식집단은 왼쪽꼬리모멘텀 현상이 사라지는 약한 증거를 보인다.

<표 7>에서 <표 10>까지의 결과는 기업특성변수들을 통제한 후에도 한국 주식시장에서 왼쪽꼬리모멘텀이 유의하게 존재한다는 실증 결과를 보여준다. 특성변수별 조건부 이변량포트 폴리오를 기준으로 구성한 (H-L) 무비용포트폴리오의 투자성과를 분석한 결과는(Ave.) 12가지 특성변수 중 비유동성의 경우를 제외하고는 대부분 유의한 음(-)의 성과측정치를 보여주어 특성변수들을 통제한 후에도 우리 시장에서 왼쪽꼬리모멘텀이 존재함을 보여준다. 다만 앞의 3.1절에서 확인하였듯이 가치가중방법에 비교하여 동일가중방법의 경우에 보다 강한 결과를 보이고, FF-3요인모형의 위험조정수익률이 무위험이자율에 대한 초과수익률과 CAPM-위험 조정수익률에 비교하여 작은 음(-)의 값과 약한 통계적 유의성을 보인다. 이러한 결과는 우리 시장에서 확인되는 왼쪽꼬리모멘텀 현상이 포트폴리오의 가중치부여방법과 투자성과 측정치에 대한 가격결정모형 선택에 따라 부분적으로 영향을 받을 수 있음을 시사하는 것이다. 영향을 미치는 변수들을 살펴보면 고유왜도, 고유변동성, MAX효과, 단기반전 등은 높은 주식집단에서 왼쪽꼬리모멘텀이 보다 강하게 나타나고, 기업규모, 장부-시장가치비율, 모멘텀, 공왜도 등은 낮은 주식집단에서 보다 강한 왼쪽꼬리모멘텀이 발생한다. 이는 왼쪽꼬리모멘텀이 기존의 장부-시장가치비율, 모멘텀효과와는 차별적인 주식수익률 설명력을 가질 수 있음을 시사한다. 또 MAX효과와 고유변동성이 낮은 주식집단에서는 음(-)의 투자성과가 확인되지 않아 왼쪽꼬리모멘텀 현상이 이들 변수들에 영향을 받을 수 있음을 보여준다.

4.2 왼쪽꼬리모멘텀의 주식수익률 설명력

앞서 확인되었듯이 우리 시장에서 왼쪽꼬리모멘텀 현상은 유의하게 존재한다. 이는 투자전략 이나 위험관리전략의 수립과정에서 왼쪽꼬리모멘텀을 우리 시장에서 거래되는 주식의 수익률 변동을 설명하는 변수로 유용하게 이용할 수 있음을 의미한다. 한국 주식시장의 왼쪽꼬리모멘텀이 개별주식수익률의 횡단면적 변화를 설명하는 설명력을 갖는지를 확인하고 그 유용성을 간단하게 분석한다. 본 절에서의 분석은 왼쪽꼬리모멘텀이 위험-수익 차원에서 가격결정요인으로서 기능할 수 있는지를 검증하는 것이 아니라, 왼쪽꼬리모멘텀 퍼즐이 해소되지 않고 존재하는 상황에서 왼쪽꼬리모멘텀에 기초한 투자전략의 유용성과 주식수익률 변동에 대한 설명력을 갖는지를 확인하는 것이다. 분석방법은 Fama and French(1993)의 HML-요인 생성과정에 따라 왼쪽꼬리모멘텀 요인프리미엄을 생성하고 이 변수가 갖는 설명력을 분석한다. 즉, 독립적 이중정렬 포트폴리오(independently double-sorted portfolio) 구성방법에 따라 기업규모(= 주식가격×발행주식수)에 따라 2가지 주식집단(B, S)으로 분류하고, 동시에 과거 형성기간에서 측정한 신뢰수준 97.5% LT-VaR에 따라 상위 30%, 중간 40%, 하위 30%의 3가지 주식집단(H, M, L)으로 구분한 후에, 주식집단 간의 교집합을 갖는 주식들로 2×3 포트폴리오 매트릭스 구조를 구성한다. 그리고 앞의 검증결과에서 H-L 무비용 포트폴리오의 투자성과는 유의한 음(-)의 값을 보이기 때문에, 양(+)의 요인프리미엄을 생성하기 위해 낮은 LT-VaR을 갖는 주식집단의 가치가중수익률 산술평균[(BL+SL)/2)]에서 높은 LT-VaR을 갖는 주식집단의 가치가중수익률 산술평균[(BH+SH)/2]을 뺀 값으로 왼쪽꼬리모멘텀 요인프리미엄(LTMP)을 산출한다.

검증결과는 <표 11>에 제시한다. 검증결과는 4가지로 구분한다. 첫째, 미래 보유기간 1개월, 3개월, 6개월, 12개월 각각에 대한 LTMP의 평균값, 둘째, LTMP를 생성하는데 이용된 포트폴리오 주식집단(BH, BL, SH, SL)의 수익률과 LTMP의 관계를 회귀분석을 이용하여 분석한 결과, 셋째, Fama and French(1993)의 3요인 프리미엄(Mkt, SMB, HML)과의 상관관계, 넷째, LTMP(종속변수)에 대한 FF3 요인프리미엄(독립변수)의 회귀분석 결과이다.

<표 11>

왼쪽꼬리모멘텀의 주식수익률 설명력

표는 기업규모를 통제한 왼쪽꼬리모멘텀 요인프리미엄의 분석결과를 나타낸다. 독립적 이중정렬 포트폴리오 구성방법에 따라 기업규모(=주식가격×발행주식수)에 따라 2가지 주식집단(B, S)으로 분류하고, 동시에 과거기간의 신뢰수준 97.5% LT-VaR에 따라 상위 30%, 중간 40%, 하위 30%의 3가지 주식집단(H, M, L)으로 구분한 후에, 주식집단 간의 교집합을 갖는 주식들로 2×3 포트폴리오 매트릭스 구조를 구성한다. 이후 낮은 LT-VaR을 갖는 주식집단의 가치가중수익률 산술평균[(BL+SL)/2)]에서 높은 LT-VaR을 갖는 주식집단의 가치가중수익률 산술평균[(BH+SH)/2]을 뺀 값으로 LTMP를 산출한다. 보고 결과는 첫째, 미래보유기간에 따른 LTMP (Panel A), 둘째, LTMP 생성에 이용된 기업규모와 LT-VaR 기준 2×3 포트폴리오의 수익률(종속변수)을 LTMP에 회귀분석한 결과(Panel B), 셋째, LTMP와 Fama-French 3요인프리미엄 과의 상관관계(Panel C), 넷째, LTMP를 FF3 요인프리미엄에 회귀분석한 결과(Panel D)이다. 괄호안의 값은 Newey and West(1987, 1994)에 따라 자기상관과 이분산성을 조정한 t-값이다. ***, **, *는 각각 1%, 5%, 10% 수준에서 통계적으로 유의함을 의미한다.

<표 11>의 결과를 보면, 각 검증에서 공통적으로 왼쪽꼬리모멘텀 요인프리미엄의 유용성을 지지하는 증거를 보여준다. 구체적으로 살펴보면, 첫째, 왼쪽꼬리모멘텀 요인프리미엄의 평균값이다. 미래 보유기간 1개월에서 12개월로 기간을 확장함에 따라 LTMP는 통계적으로 유의한 양(+)의 값을 가지나, 그 크기는 보유기간 1개월의 경우 0.05%, 3개월의 경우 0.04%로 작아지는 모습을 보인다. 둘째, 포트폴리오(BH, BL, SH, SL)의 수익률(종속변수)을 LTMP에 회귀분석 한 결과를 보면(Panel B), 주식집단이나 보유기간에 관계없이 LTMP는 포트폴리오의 수익률과 매우 유의한 음(-)의 관계를 가지며, 회귀계수의 크기 역시 매우 큰 값을 갖는다. 주식집단별로 보면 과거 형성기간에 높은 LT-VaR을 이용하여 구성된 주식집단(BH, SH)의 회귀계수가 낮은 LT-VaR의 주식집단(BL, SL)에 비교하여 보다 크고 유의적인 값을 갖는다. 이러한 결과는 왼쪽꼬리모멘텀 요인프리미엄이 과거 형성기간에 높은 LT-VaR을 갖는 주식들과 높은 관련성을 갖는다는 것을 나타낸다. 셋째, LTMP와 FF3 요인프리미엄(Mkt, SMB, HML) 과의 상관관계를 보면, LTMP는 시장위험프리미엄(Mkt)과 규모프리미엄(SMB)에 대해 음(-)의 상관관계를 갖고, 가치프리미엄(HML)과는 양(+)의 상관관계를 보인다. 그러나 상관계수의 크기는 절댓값 기준으로 0.26에서 0.38 사이의 값으로 왼쪽꼬리모멘텀 요인프리미엄이 주식 수익률의 변동을 설명하는 독립적인 정보효과를 갖고 있음을 잘 보여준다. 넷째, LTMP를 FF3 요인프리미엄(독립변수)에 대해 회귀분석한 결과이다. 분석결과에서 절편값은 미래 보유기간 1개월과 3개월에서 통계적으로 유의한 양(+)의 값을 보인다. 이는 LTMP가 Fama and French (1993)의 3요인 프리미엄과는 차별적인 고유한 설명력을 갖는다는 것을 의미한다.

요약하면, <표 11>의 결과는 한국 주식시장에서 관찰된 왼쪽꼬리모멘텀 현상이 주식수익률의 변동을 설명하는 설명요인으로서 기능할 수 있으며, 현재 우리 시장의 수익률변동 특성을 이해하고 이를 반영한 투자전략의 구성에 왼쪽꼬리모멘텀 요인프리미엄(LTMP)이 유용하게 활용될 수 있음을 보여주는 것이다.

Ⅴ. 결론

전통적인 재무이론에 따르면, 투자자들은 위험이 높은 주식에 투자할 때 더 높은 수익률을 요구한다. 본 연구에서는 2000년 7월부터 2020년 6월까지의 국내 유가증권시장과 코스닥시장에 상장된 주식과 상장폐지주식을 대상으로 Atilgan et al.(2020)이 보인 전통적인 위험-수익의 상충관계로 설명되지 못하는 현상인 왼쪽꼬리모멘텀이 존재하는지를 분석하였다. Atilgan et al.(2020)은 왼쪽꼬리모멘텀 현상이 개인투자자의 보유비중이 높고 투자자의 관심을 덜 받으며 차익거래에 제약이 더 많은 주식에서 더 강하게 발생한다고 주장한다. 한국 주식시장은 미국 주식시장에 비해 개인투자자의 비중이 높고, 가격제한폭과 공매의 제약 등 차익거래제약이 더 큰 특성을 가진다. 이런 특성을 고려하면 미국 주식시장에서 보인 왼쪽꼬리모멘텀 현상이 우리 시장에서 더욱 강하게 나타날 것으로 기대할 수 있다.

본 논문의 분석결과를 요약하면 다음과 같다. 전통적인 재무이론의 시각과는 다르게, 과거기간의 일별수익률에 기초한 VaR로 측정한 왼쪽꼬리위험 측정치가 주식의 기대수익률과 유의한 음(-)의 관계를 가지며, 왼쪽꼬리위험이 높은 포트폴리오(H)를 매수하고 낮은 포트폴리오(L)를 매도하는 투자전략의 성과는 매우 유의한 음(-)의 값을 가져 한국 주식시장에서 왼쪽꼬리모멘텀 현상이 유의하게 존재함을 보여준다. 측정된 왼쪽꼬리위험 측정치를 기준으로 10분위 포트폴리오를 구성하고 동일가중방법과 가치가중방법으로 구성한(H-L) 무비용포트폴리오의 초과수익률을 Fama-French 3요인모형을 기준으로 측정한 경우 월평균 -0.67%~-0.73%의 크기를 갖는다. 이러한 결과는 왼쪽꼬리위험 척도인 VaR을 측정하는 백분위 수준의 변경이나 조건부 VaR(ES)를 이용한 경우, 주식시장의 상황 변화를 고려한 경우에도 전반적으로 확인된다.

왼쪽꼬리모멘텀 현상에 영향을 미칠 수 있는 주요 변수들(가격결정요인 관련 변수인 시장베타, 기업규모, 장부-시장가치비율, 과거기간의 투자성과 관련변수인 모멘텀, 단기반전, 장기반전, MAX효과, 수익률분포의 속성에 관련된 변수인 왜도, 고유왜도, 공왜도, 시장미시구조 관련 변수인 비유동성, 고유변동성)을 통제한 조건부왼쪽꼬리모멘텀의 존재를 확인하기 위해 종속적 이중정렬방법을 이용한 이변량 포트폴리오 분석을 수행하였다. 분석결과는 우리 시장에서 확인되는 왼쪽꼬리모멘텀 현상이 포트폴리오 가중치부여방법과 투자성과 측정치에 대한 가격결정모형 선택에 따라 부분적으로 영향을 받으나. 이들 변수를 통제한 후에도 앞서 확인한 음(-)의 왼쪽꼬리모멘텀 현상이 유효하게 존재하는 현상임을 확인시켜준다.

추가적으로 한국 주식시장에서 관찰된 왼쪽꼬리모멘텀 현상이 주식수익률의 변동을 설명하는 설명요인으로서 기능할 수 있는지를 왼쪽꼬리모멘텀에 기반한 요인프리미엄을 생성하여 검증하였다. 검증결과는 왼쪽꼬리모멘텀요인이 기존의 Fama-French 3요인과는 독립적으로 주식수익률 변동을 설명하는 정보가치를 가짐을 보여주어 왼쪽꼬리모멘텀 요인프리미엄이 유용하게 활용될 수 있음을 보여준다.

본 연구는 한국의 유가증권시장과 코스닥시장을 대상으로 왼쪽꼬리위험과 주식수익률의 관계, 그리고 왼쪽꼬리모멘텀 현상의 존재여부를 강건하게 분석하였다는 점에서 중요한 의의를 가진다. 또한 본 연구의 결과는 왼쪽꼬리모멘텀 현상에 대한 국내 연구가 많지 않은 상황에서 외국 연구와 국내 연구 간의 차이를 좁히는데 기여할 것으로 기대하며, 향후 왼쪽꼬리모멘텀 현상의 발생원인에 대한 심층적인 연구를 통하여 다양한 후속담론을 생산할 것으로 기대한다.