1. ěëĄ

íęľęą°ëěě ę°ě 죟돸죟ëíěěĽ(order-driven market)ěě 죟ě ëë íěěíě 죟돸í ë ěŹěŠ ę°ëĽí 쥰깴ëśěŁźëŹ¸ěźëĄě IOC(immediate-or-cancel) ëźë ěŁźëŹ¸ě´ ěë¤. IOC 죟돸ě â죟돸ě§íí ěë ěŚě 졨ě죟돸âě´ëźë ę˛ěźëĄě 죟돸ě§ęłěĽ(limit order book)ě ę°ę˛ŠěĄ°ęą´ě 윊쥹íë ěęł ěëě´ ěë ë˛ěěě ě˛´ę˛°ě´ ěąěŹëęł , 미윊쥹ëë ëë¨¸ě§ ěŁźëŹ¸ěëě ěëě ěźëĄ ěŚě 졨ěëë 죟돸 ě íě´ë¤.

IOC죟돸ě ęłě˘ëĽź ę°ęł ěë ęą°ëěëźëŠ´ 죟돸í ë íšëłí ě íěě´ ë꾏ë ěŹěŠ ę°ëĽíë¤. íě§ë§ IOC죟돸ě ęľë´ ííŠě ě˛ěěźëĄ ëł´ęł í Choi(2022)ě ě°ęľŹě ěí늴, 2019ë

5ěëśí° 2020ë

9ěęšě§ KOSPI200 ěľě

ěěĽě ě 체 ęą°ëë ě¤ IOC죟돸ěźëĄ 체결ë ęą°ëëě ëšě¤ě´ 56%뼟 ě°¨ě§í ě ëëĄ ë§ě´ íěŠëęł ěěě§ë§, IOC죟돸ě 99%뼟 ě¸ęľě¸íŹěěę° ěŹěŠíęł ę¸°ę´ęłź ę°ě¸íŹěěë ęą°ě ěŹěŠíě§ ěë ëą, ęľë´ě¸ íŹěěę° íěŠě í¸ě°¨ę° ë§¤ě° í° ę˛ěźëĄ ëíëŹë¤. IOC죟돸ě ꡸ íšěąě 죟돸ě§ęłěĽě ę°ę˛Šęłź ěë ě 보뼟 ě¤ěę°ěźëĄ 모ëí°ë§íęł ěëě ěźëĄ ëš ëĽ¸ 죟돸ëĽë Ľě´ ě¤ěí기 ë돸ě ęł ëšëęą°ë(high-frequency trading)ëĄ ěŹěŠëë ě ě ęł ë ¤íë¤ëŠ´, ě ěí ě ëł´ě˛ëŚŹ ë° ěŁźëŹ¸ěě¤í

ě ëł´ě í ě¸ęľě¸íŹěěěę˛ íěŠëę° ë ëë¤ęł ě§ěí ě ěë¤. ëí IOC죟돸ě ëł´íľě ě§ě ę°ěŁźëŹ¸ęłź ëŹëŚŹ 죟돸ě§ęłěĽě ë기íě§ ěęł ěŚě 졨ěë기 ë돸ě, ě ëł´ě˛ëŚŹ ë° ěŁźëŹ¸ěëę° ë ëš ëĽ¸(low latency) í¸ë ě´ëě ě§ě°ě°¨ěľęą°ë(latency arbitrage)ě ëěě´ ëęą°ë ëë picking-off 댏ě¤íŹě ë

¸ěśëě§ ěëë¤ë ěĽě ě´ ěë¤.

ěľęˇź 10ë

ę° ě ëł´íľě ęłź ěť´í¨í°ę¸°ě ě ëšě˝ě ě¸ ë°ě ě íě

ě´ íęľęą°ëě뼟 íŹí¨íěŹ ě ě¸ęł ęą°ëěěë ęł ëšëęą°ëěě ěë경ěěźëĄ ě¸í´ ë§ě ě§ě ě¸ ëłí뼟 ę˛Şęł ěë¤. Musciotto et al.(2021)ě 기ě íě ěźëĄ ě¸í´ ě ě¸ęł ëëśëśě ęą°ëěěě ęł ëšëęą°ëě ëšě¤ě´ 50% ě ë ě°¨ě§íęł ě ě죟돸ě§ęłěĽě ě ěĽë ęą°ëě 보뼟 ě˝ë ěëę° ě ë§ě´íŹëĄě¸ěť¨(ë°ąë§ëśě 1ě´)ě ëśęłźíë¤ęł ëł´ęł ěěźëŠ°, Aquilina et al.(2022)ë FTSE 100ě 죟ěěěĽěě ęą°ëěë¤ę°ě 경ěě ë°ąë§ëśě 5ě´ěě 10ě´ě ě°¨ě´ëĄ 결ě ëë¤ęł 죟ěĽíë¤. ęľë´ëŹ¸íěě Choi(2022)ě ě§ěěľě

ěěĽěě ęł ëšëęą°ëěë¤ ěŹě´ě 경ěě´ ë°ëŚŹě¸ěť¨(ě˛ëśě 1ě´) ě´ë´ě 경ěěźëĄ ë¤ě´ě°ë¤ęł 죟ěĽíęł ěë¤. ëí Seoul Central District Court(2011)ě ELW ě¤ěşíź ę´ë ¨ í결돸ě ěí늴, 2010ë

ëšě ELWě ëí ě ëěąęłľę¸ě (liquidity provider)ě 죟돸ě˛ëŚŹěëę° 28ë°ëŚŹě´ěě 36ë°ëŚŹě´ ěŹě´ëźęł 기ě ëě´ ěë¤. 12ë

ě´ ę˛˝ęłźë ě§ę¸ě 죟돸ě˛ëŚŹěëę° ě´ëł´ë¤ ë ëš ëĽź ę˛ěźëĄ ěśě ëë¤.

ěěĽěěě ěë경ě ęłźě´ęłź ęł ëšëęą°ëě ěŚę°ë í¸ę°ě¤íë ë(bid-ask spread)ě ěěĽěŹë(market depth) ęˇ¸ëŚŹęł ëłëěą ëą ęą°ëí경ě ě§ě 츥늴ě ë§ě ěíĽě ě¤ ę˛ěźëĄ ěěëë¤. 본 ě°ęľŹë KOSPI 200 ě 돟ěěĽěě IOCěŁźëŹ¸ě´ ěěĽě íě§ě ě´ë í ěíĽě ëźěšëě§ ë¤ěí ę°ëěě ę˛ěŚíë ę˛ě 몊íëĄ íë¤. Choi(2022)ě ě°ęľŹę° íęľě ě§ěěľě

ěěĽěě Easley et al.(2002)ě PIN(probability of informed trading)모í ëąě íľí´ IOCěŁźëŹ¸ě´ ě 보기ë°ęą°ëě¸ě§ ěŹëśëĽź 쥰ěŹí ę˛ě¸ ë°ëŠ´, 본 ě°ęľŹë ëěě´ ě§ěě 돟ěěĽě´ëźë ě ě´ě¸ě ë ë¤ëĽ¸ ꡟ본ě ě¸ ě°¨ě´ę° ěë¤. ě ěě ě°ęľŹë ěľě

ě 기ě´ěě°ě ëí´ ě°ě°í 졨ëí ëë ëśěě íľí´ ë°ęľ´í, ěŹě ě 보뼟 ëł´ě í ě ëł´ęą°ëěę° ě´ëĽź ěěĽěě ěěľěźëĄ ě íí기 ěí´ IOC 쥰깴죟돸ě ěŹěŠíë ę˛ě¸ě§ ěŹëśëĽź ěě보기 ěí ě°ęľŹě´ë¤. ë°ëŠ´ 본 ě°ęľŹë ě§ěě 돟ěěĽěě IOCę° ě¤íë ë, ěěĽěŹë, ëłëěą ëą ěěĽíě§ ě¸ĄëŠ´ěě ę¸ě ě íšě ëśě ě ěíĽě ëźěšëě§ ěŹëśëĽź 쥰ěŹí기 ěí ě°ęľŹě´ë¤.

í´ě¸ëŹ¸íěě IOCě°ęľŹë í¸ěŁźěěĽě ëěěźëĄ ëśěí Duong et al.(2017) ě°ęľŹę° ě ěźíë¤. ě´ë¤ě í¸ěŁźě S&P/ASX 200 죟ěěěĽěě IOCěŁźëŹ¸ě´ ě 체 ęą°ëë ě¤ěě 7.41%ě ëšě¤ě ě°¨ě§íęł ěęł , ěźë°ěŁźëŹ¸ëł´ë¤ ë ë§ě ę°ę˛ŠěśŠę˛Šě ěźę¸°íë ëąě ëśě결곟뼟 í ëëĄ ě ëł´ęą°ëëĄ íë¨íęł ěë¤. 본 ě°ęľŹë HFTě ëí ě°ęľŹěë ę´ë ¨ě´ ěë¤. ëš ëĽ¸ 죟돸ěëě ęł ëšëęą°ëę° ě¤íë ë, ěěĽěŹë, ě ëł´í¨ě¨ěą ë° ěěĽě ëłëěą ëą ěěĽíě§ě ě´ë í ěíĽě 미ěšëě§ě ę´í´ ë§ě ě°ęľŹę° ě§íëěë¤. ě´ë¤ ě°ęľŹë íŹę˛ ě¸ę°ě§ëĄ ëśëĽí ě ěë¤. 첍째 ëśëĽë ě´ëŹí ěë경ěě´ ěźę¸°í ěëĄě´ ęą°ëěíě ꡸ę˛ě´ ěěĽě 미ěšë ěíĽě ëśěí ě°ęľŹě´ęł , ë째 ëśëĽë ěëĄě´ ęą°ëí경ě ě ěíë ęą°ëěě 죟돸ííě ę´í ě°ęľŹě´ęł , ě¸ ë˛ě§¸ ëśëĽë ęł ëšëęą°ëě ëš ëĽ¸ 죟돸깰ëěě ęą°ë뼟 ęˇě í기 ěí ě ë° ě ěą

ęłź ꡸ę˛ě´ ěěĽě 미ěšë ěíĽě ę´í ě°ęľŹě´ë¤.

ęł ëšë매매ě ëš ëĽ¸ ěŁźëŹ¸ě´ ěěĽě ę¸ě ě ě¸ ěíĽě 미ěšë¤ë ě°ęľŹëĄë Hasbrouck and Saar(2013), Brogaard et al.(2013), Menkveld(2013), Ammar and Hellara(2021), Woo and Choe(2013) ëąě ë¤ ě ěë¤. Hasbrouck and Saar(2013)ë ě ěí 죟돸(low latency activity)ě 츥ě í ě ěë ě§í뼟 ěŹěŠíěŹ ęł ëšëë§¤ë§¤ę° ěěĽíě§ě ę°ě íšě ě

íěí¤ëě§ ěŹëśëĽź 쥰ěŹíěë¤. ꡸ë¤ě NASDAQě ęą°ëë°ě´í°ě ëí ëśěě íľí´ ě ě§ě°íë(low latency activity)ě´ ě¤íë ë뼟 ę°ěěí¤ęł , ěěĽěŹë뼟 ěŚę°ěí¤ëŠ° ěěĽě ë¨ę¸°ëłëěąě ę°ěěí¨ë¤ęł ëł´ěë¤. Brogaard et al.(2013)ě HFTę° ę°ę˛Šë°ę˛Źě 기ěŹíë¤ęł ëł´ěęł , Ammar and Hellara(2021)ë HFTę° ěěĽí¨ě¨ěąě 기ěŹíë¤ęł ëł´ěë¤. Woo and Choe(2013)ě íęľě ELWěěĽěě ęł ëšëęą°ëę° ěěĽě ě¤íë ë뼟 ę°ěěí¤ęł ëłëěąě ę°ěěěź°ęł , ě´ëĄ ę°ę˛Šęłź ěěĽę°ę˛Šě 괴댏뼟 ę°ěěěź ěěĽí¨ě¨ěąě 기ěŹíë¤ęł íę°íë¤.

ě´ěë ëŹëŚŹ HFTě ëśě ě 츥늴ě ě ěí ě°ęľŹ ëí ë§ě´ ěë¤. Lee(2015)ě Chung et al.(2015)ě ę°ę° íęľě ě§ěě 돟ěěĽęłź 죟ěěěĽěě ęł ëšëíëě ëśěíěëë° ě´ëĄ ě¸í´ ěěĽě ě§ě ěě¤ě´ ę°ěëěë¤ęł íę°íęł ěë¤. Kang et al.(2020)ě ě§ěě 돟ěěĽěě ęł ëšëíëě ěíĽë Ľě´ ěěĽě ěíě ë°ëźě ëŹëŚŹ ëíëë¤ęł ëł´ěë¤. ěŚ ě ěěíěěë ęł ëšëíëě´ ëłëěąě ę°ěěěź°ěźë ě¤í¸ë ě¤ěíŠěěë ëłëěąě ěŚę°ěěź°ë¤ęł ëł´ěë¤. Budish et al.(2015)ě HFTě ěë경ěě´ ěěĽě ëěąě ě

íěěź°ęł , Foucault et al.(2016)ë ěëě°ě뼟 ę°ë ě 보기ë°ęą°ëěě 죟돸íëŚě´ ëłëěąě ěŚę°ěí¨ë¤ęł 죟ěĽíěěźëŠ°, Baron et al.(2019)ęłź Brogaard et al.(2014)ë ęł ëšëęą°ëěě ěŚě ěěĽę°ěŁźëŹ¸ěźëĄ ě¸í´ ę°ę˛ŠěśŠę˛Šě´ ěŚę°íë ëą ěěĽě ëśě ě ě¸ ěíĽě ëźěł¤ë¤ęł ëśěíë¤. ëí Aquilina et al.(2022)ë HFTę° ěííë ě§ě°ě°¨ěľęą°ë(latency arbitrage)ę° ěěĽě ëśě ě ě¸ ěíĽě ëźěšë¤ęł 죟ěĽíë¤. ě´ě¸ěë HFTëĄ ě¸í´ ěëĄę˛ ëłíë ěěĽí경곟 경ěě ë¤ëĽ¸ ě°ęľŹëĄë Hagstromer and Norden(2013), Hendershott and Riordan(2013), Hoffmann (2014), Kirilenko et al.(2017), Brogaard and Garriott(2019) ëąě´ ěë¤.

HFT뼟 기ë°ěźëĄ íë IOCěŁźëŹ¸ě´ ěěĽě 미ěšë ěíĽě ëí ě°ęľŹë ě°žě보기 ě´ë ľë¤. IOCě ëí ě°ęľŹ ěě˛´ę° ęľë´ě¸ě ęą¸ěł Duong et al.(2017)ęłź Choi(2022) ě´ě¸ěë ëłëĄ ě기 ë돸ě´ë¤. 본 ě°ęľŹěěë 2019ë

5ěëśí° 2020ë

9ěęšě§ě 체결 ë° í¸ę°ë°ě´í° (TAQ; trade and quote)뼟 ěŹěŠíěŹ KOSPI 200 ě§ěě 돟ěěĽěě IOC죟돸ě ííŠęłź íšěą ë° ěěĽě 미ěšë ěíĽě 죟돸íëŚëśęˇ í, 체결ěěěę°, ě¤íë ë, ěěĽěŹë, ëłëěą ëąě 츥늴ěě ëśěíë¤.

본 ě°ęľŹëĽź íľí´ ëěśë 죟ě ě°ęľŹę˛°ęłźë ë¤ěęłź ę°ë¤. 첍째, ě§ěě 돟ěěĽěě IOC죟돸ě 죟돸깴ě 기ě¤ěźëĄë 10%ě ëšě¤ě, 체결ë 기ě¤ěźëĄë 50%ě ëšě¤ě ě°¨ě§íěęł , íŹěěě íëłëĄë ě¸ęľě¸ě´ 99.9%뼟 ěŹěŠíë ę˛ěźëĄ ëíëŹë¤. ë째, IOC죟돸ě ěŁźëĄ ë¤ěě ęł ëšëęą°ëěę° ëěě 죟돸ě ě ěśíë ëë°ë§¤ë§¤ě ííëĄ ëíëŹěźëŠ°, ě´ë¤ ěí¸ę°ě íęˇ ę˛˝ěëĽ ě 18%ëĄ ěĄ°ěŹëěë¤. ě

째, ę°ě¸íŹěěë ě 체 ęą°ëëěě 21%ě ëšě¤ě ě°¨ě§íęł ěěźë IOC ëë°ë§¤ë§¤ě ëí ęą°ëěëë°ŠěźëĄěë 34%ě ëšě¤ě ě°¨ě§íë ę˛ěźëĄ ëíë IOC죟돸ě ëí´ě ěëě ěźëĄ ëě ęą°ëëěě´ ëë ę˛ěźëĄ 쥰ěŹëěë¤. ě´ěě ëśě결곟ë 죟ę°ě§ěěľě

ě ëěěźëĄ í Choi(2022)ě ě°ęľŹę˛°ęłźě íŹę˛ ë¤ëĽ´ě§ ěě ę˛ěźëĄ ëíëŹëë°, ě´ë IOC죟돸ě ě¤ííë ě¸ęľě¸íŹěěę° ě§ěě 돟곟 ě§ěěľě

ě ëí´ ěí ě´ěŠęłź ęą°ëě ëľ ě¸ĄëŠ´ěě ěěę° í° ě°¨ě´ëĽź ëě§ ě기 ëëŹ¸ě¸ ę˛ěźëĄ íě´ëë¤.

ëˇě§¸, IOC죟돸ěźëĄ ě¸í´ ë°ěë 죟돸íëŚëśęˇ í(order flow imbalance)ě´ non-IOC죟돸ě ëší´ ë ë§ě ę°ę˛ŠěśŠę˛Šě 죟ë ę˛ěźëĄ 쥰ěŹëěë¤. ë¤ěŻě§¸, 체결ěę°ëśěě íľí´ě IOC매매ë ěźë°ě ě¸ ë§¤ë§¤ě ëšęľíěŹ ěŁźëŹ¸ě íęˇ ě˛´ę˛°ěę°ě 50% ě´ě ę°ěěí¤ë í¨ęłźę° ěë ę˛ěźëĄ ëíëŹë¤. ěŹěŻě§¸, IOCëë°ë§¤ë§¤ę° ěěĽíě§ě ěíĽě 미ěšëě§ íęˇëśěě íľí´ě ě´í´ëł¸ 결곟, IOC ëë°ë§¤ë§¤ě ěŚę°ë í¸ę°ě¤íë ë뼟 ěŚę°ěí¤ęł , ěěĽěŹë뼟 ę°ěěí¤ëŠ° ěěĽëłëěąě ěŚę°ěí¤ë ëą ě§ěě 돟ěěĽě ěěĽíě§ě ëśě ě ěíĽě ëźěšë ę˛ěźëĄ ëíëŹë¤.

íěŹ IOC ëą ěĄ°ęą´ëśěŁźëŹ¸ě ëí ě°ęľŹę° ęą°ě ěë ěíěě, 본 ě°ęľŹë IOCěŁźëŹ¸ě´ ě§ěě 돟ěěĽě 미ěšë ěíĽě ě´í´ë´ěźëĄě¨ 기쥴ě HFTě ěěĽëŻ¸ě꾏쥰ě 돸íě ě미ěë 기ěŹëĽź íěë¤ęł íë¨íë¤. íší 죟돸íëŚëśęˇ íęłź 체결ěěěę° ëśěě, 본 ě°ęľŹěě ěëĄę˛ ěëí ë°Šë˛ěźëĄě íĽí ě´ ëśěźě ě°ęľŹě íěŠë ě ěë ě°ęľŹë°Šë˛ëĄ ě ěśę°íěë¤ë ě ěě ěěę° ěë¤.

본 ě°ęľŹě 꾏ěąě ë¤ěęłź ę°ë¤. ě 2ěĽěěë ë°ě´í°ě IOC 죟돸ě íšěąě ě´í´ëł¸ë¤. ě 3ěĽěěë 죟돸íëŚě ëśęˇ íě ëśěíęł , ě 4ěĽěěë IOC죟돸곟 체결ěěěę° ěŹě´ě ę´ęłëĽź ëśěíë¤. ě 5ěĽěěë IOCěŁźëŹ¸ě´ ěěĽíě§ě 미ěšë ěíĽě ëśěíęł , ë§ě§ë§ěźëĄ ě 6ěĽěěë ę˛°ëĄ ęłź ěěŹě ě 기ě íë¤.

2. ë°ě´í°

2.1 í본ě ě ě

본 ě°ęľŹěě ěŹěŠíë ë°ě´í°ë íęľęą°ëěěě ě ěěźëĄ ě ęłľë°ě ę˛ěźëĄě, KOSPI 200 죟ę°ě§ě ě 돟ęłě˝ě 죟돸곟 체결ë´ěě´ 1/1000ě´ ë¨ěëĄ ëŞ¨ë 기ëĄëě´ ěë TAQ (trade and quote) ë°ě´í°ě´ë¤. 모ë ęą°ëë´ěě í¸ę°íěźęłź 체결íěź ëę°ě ë°ëĄ 꾏ëśëě´ ę¸°ëĄëě´ ěë¤. í¸ę°íěźěë 모ë ë§ę¸°ě ě§ěě 돟ęłě˝ ę°ę°ě ëí´ ě˘

몊ě˝ë, 죟돸ę°ę˛Š, 죟돸ěë, 매ě/매ëěŹëś, ě ęˇ/ě ě /졨ěěŹëś, 죟돸ěę°, 죟돸ě í(ěěĽę° ëë ě§ě ę°ěŁźëŹ¸ ëą), 죟돸쥰깴(IOC ëë FOK(Fill-or-Kill ëą), ě¸ęľě¸ ěŹëś, íŹěě

ě˘

ě˝ë, í¸ę°ě ěë˛í¸, ë 벨1ëśí° 5ęšě§ě í¸ę°ę°ę˛Šęłź í¸ę°ěęł ëąě´ 기ëĄëě´ ěęł , 체결íěźěë ě˘

몊ě˝ë, 체결ěę°, 체결ěë, 체결ěě ě ë 벨1ëśí° 5ęšě§ě í¸ę°ę°ę˛Šęłź ěęł ę° ę¸°ëĄëě´ ěęł ěě¸ëŹ 매ěě 매ëě ę°ę°ě 죟돸ěę°, 죟돸쥰깴, ě¸ęľě¸ ěŹëś, íŹěě

ě˘

ě˝ë ëąě´ ěëĄëě´ ěë¤. ě´ ěëŁëĽź íľí´ě 죟돸곟 체결곟ě ěě 기ę´, ę°ě¸, ě¸ęľě¸ 3ę° ęˇ¸ëŁšě ëí´ IOCě FOK ëą íšëłěŁźëŹ¸ě ęą°ëëšě¤ě ëŹźëĄ ëę° ęą°ë뼟 죟ëíěë ě§ ěŹëś ëąě ëśëŞ

íę˛ íë¨í ě ěë¤.

본 ě°ęľŹěěë 2019ë

5ě 14ěźëśí° 2020ë

9ě 10ěźęšě§ě 기ę°ěě ěľęˇźě돟 ęłě˝ ě¤ ě쥴ë§ę¸°ę° 30ěź ě´íě¸ KOSPI200 죟ę°ě§ě ě 돟ęłě˝ë§ě 쥰ěŹíëŻëĄ ě´ ęą°ëěźěë 122ěźě´ë¤. ě´ě¤ 2019ë

ěë ë§ę¸°ěźě´ 6ě, 9ě, 12ě ë°ěíęł 2020ë

ěë ë§ę¸°ěźě´ 3ě, 6ě, 9ěě ë°ěíë¤. ëí 2019ë

ě ęą°ëěźěë 63ěźě´ęł , 2020ë

ěë 59ěźě´ë¤.

2.2 IOC 죟돸ě ííŠ

<í 1>ě í본기ę°ě¸ 122ěźě ęą°ëěźěě ě ęˇęą°ëěę°ëě¸ 9:00amëśí° 15:35pm (ë§ę¸°ěźěë 15:20pm)ęšě§ ě ěë 모ë IOC죟돸곟 FOK죟돸 ęˇ¸ëŚŹęł ëë¨¸ě§ ěźë°ěŁźëŹ¸ě í¸ę°ëĽź 매ěě 매ë ę°ę°ě ëí´ě 5ę°ëĄ ëśëĽíěŹ ě 댏í ę˛ě´ë¤. ěěĽěąěŁźëŹ¸(marketable order)ě 모ë ěěĽę°ěŁźëŹ¸(market order)ęłź ěěĽěą ě§ě ę°ěŁźëŹ¸(marketable limit order)ě íŹí¨íë¤. 졨ě죟돸ě ě ě¸í 4ę°ě í¸ę° ě¤ěě ę°ěĽ ë§ě ëšě¤ě ě°¨ě§íë í¸ę°ě íě ěľě°ě 매ě ë° ěľě°ě 매ëí¸ę°ě´ęł , ę°ěĽ ëšě¤ě´ ëŽě í¸ę°ě íě ěźë°ěŁźëŹ¸ě ę˛˝ě° ěľě°ě 매ě (매ë)í¸ę°ëł´ë¤ ëě (ëŽě)í¸ę°ě´ęł IOC죟돸ě ę˛˝ě° ěľě°ě 매ě (매ë)í¸ę°ëł´ë¤ ëŽě (ëě)ě¸ ę˛ěźëĄ ëíëŹë¤. ě´ë IOCěŁźëŹ¸ě´ ěźë°ěŁźëŹ¸ě ëší´ ě˘ë ě ꡚě ě¸ ě˛´ę˛°ěěŹëĽź ę°ě§ 죟돸ě´ëźë ě ě ěěŹíë¤. ě 체 죟돸 ě¤ěě IOC죟돸ě 10.23%ě ëšě¤ěźëĄ ě ěë ë°ëŠ´ FOK죟돸ě 0.001%ëĄě ęą°ě íěŠëě§ ěěěźëŠ° ëë¨¸ě§ 89.77%ę° ěźë°ěŁźëŹ¸ěźëĄ ě ěë ę˛ěźëĄ ëíëŹë¤. í¸ę°ě íëł ëśíŹě íšëłěŁźëŹ¸ě ěěě 매ěě 매ë죟돸 ěŹëśě ěę´ěě´ ě ěŹíę˛ ëíëęł ěë¤.

<í 1>

ěźë°ěŁźëŹ¸ęłź IOC ë° FOK 죟돸ě í¸ę°ëśëĽ

ěëě íë 2019ë

5ě 14ěźëśí° 2020ë

9ě 10ěźě í본기ę°ěě ě쥴ë§ę¸°ę° 30ěź ě´ë´ě¸ ěľ ęˇźě돟ě ęą°ëěźě¸ 122ěź ëě ě ęˇěę°ëě ě ěë KOSPI 200 죟ę°ě§ěě 돟ęłě˝ě 죟돸ě IOCě FOK ęˇ¸ëŚŹęł ëł´íľěŁźëŹ¸ěźëĄ ëśëĽíěŹ ě 댏í ę˛ě´ë¤.

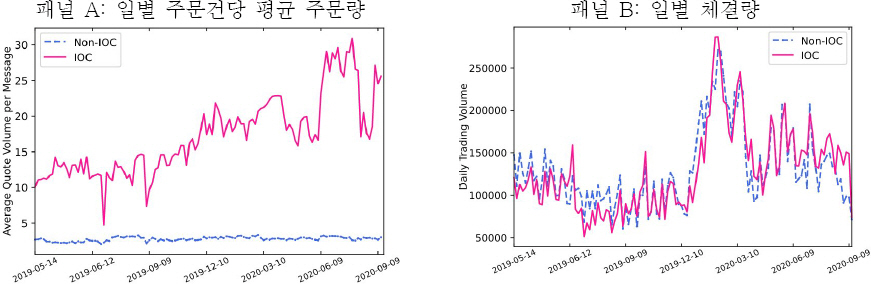

<í 2>ë íëł¸ę¸°ę° ě¤ ě˛´ę˛°ë KOSPI 200 죟ę°ě§ěě 돟ęłě˝ě ě°ëëł, íŹěěęˇ¸ëŁšëł ęˇ¸ëŚŹęł IOCěŹëśëłëĄ 꾏ëśíěŹ ě 댏í ę˛ě´ë¤. í¨ë Aë ě°ëëłëĄ ě 댏í 체결ëě 기ě´íľęłëě ěě˝í ę˛ě´ë¤. ě ë°ě ěźëĄ 2019ë

ëëš 2020ë

ě IOCěŹëśě ę´ęłěě´ ěźíęˇ ě˛´ę˛°ëě´ ëŞ¨ë ěŚę°í ę˛ěźëĄ ëíëŹë¤. ě¸ëśě ěźëĄ ě´í´ëł´ëŠ´ non-IOC죟돸ě 53% ěŚę°íěęł IOC죟돸ě 73% ěŚę°í ę˛ěźëĄ ëíëŹë¤. íší 2019ë

ěë IOC죟돸ě 체결ëě´ non-IOCëł´ë¤ ě ěě§ë§, 2020ë

ěë ꡟěí ě°¨ě´ě§ë§ ë ë§ě ę˛ěźëĄ ëíëŹë¤.

<í 2>

IOCě non-IOC 죟돸ě 체결ë

íě í¨ëAë í본기ę°ě¸ 2019ë

5ě14ěźëśí° 2020ë

9ě10ěźęšě§ě 기ę°ěě ěľęˇźě돟ě ě쥴ë§ę¸°ę° 30ěź ě´ë´ě¸ 122ěźě ęą°ëěźě ëí´ ě ęˇěę°ëě 체결ë KOSPI200 죟ę°ě§ě ě 돟ęłě˝ě ě°ëëł ęˇ¸ëŚŹęł IOC죟돸 ěŹëśëłëĄ 꾏ëśíěŹ ę¸°ě´íľęłëě ě 댏í ę˛ě´ë¤. íěě ë¨ěë ęłě˝ěě´ë¤. í¨ë Bë íŹěěëł ë§¤ě죟ë ë° ë§¤ë죟ë죟돸ě ęłě˝ě뼟 IOCě non-IOC죟돸ěźëĄ 꾏ëśíěŹ ě 댏í ę˛ě´ë¤.

í¨ë A: 체결ëě 기ě´íľęłë

í¨ë Bë íŹěěëłëĄ IOC죟돸 ë° non-IOC죟돸ě 체결ëëśíŹëĽź ě 댏í ę˛ě´ë¤. í본기ę°ě ě 체 체결ë ę¸°ě¤ IOC죟돸ěźëĄ 체결ë ě 돟ęłě˝ěě ëšě¨ě´ 2019ë

ěë 47.89%ě´ęł 2020ë

ěë 50.98%ě¸ ę˛ěźëĄ ëíë ěźë°ě ěźëĄ ěę°íë ěě¤ ě´ěěźëĄ IOCě ęą°ëëšě¨ě´ ë§¤ě° ëě ę˛ěźëĄ ě§ęłëěë¤. íŹěěëł ëśíŹëĽź 보늴 ě 체 체결ë ę¸°ě¤ 2019ë

ëěë 기ę´ě 9.37%, ę°ě¸ 19.55%, ě¸ęľě¸ě 71.09%ě ęą°ëëšě¤ě ě°¨ě§íěęł , 2020ë

ěë ę¸°ę´ 9.45%, ę°ě¸ 15.89%, ě¸ęľě¸ 74.66%ě ëšě¤ě ě°¨ě§íë ę˛ěźëĄ ëíëŹë¤. íě§ë§ IOC죟돸ě ëëśëś ě¸ęľě¸ęą°ëěę° ěëě ěźëĄ ë§ěëë° ęľŹě˛´ě ěźëĄ ě 체 IOC매매ě 99.9%뼟 죟ëíěŹ ě˛´ę˛°ë ę˛ěźëĄ ëíëŹë¤. ě´ěě KOSPI200 ě§ěě 돟ěěĽěěě IOC체결ëśíŹë Choi(2022)ě´ ëł´ęł í KOSPI200 죟ę°ě§ě ěľě

ěěĽěěě 결곟ě ë§¤ě° ě ěŹí ę˛ěźëĄě íęľě 죟ę°ě§ěě 돟 ë° ěľě

ěěĽěěë ě¸ęľě¸ęą°ëěę° IOC매매뼟 ě ě ěźëĄ 죟ëíë¤ęł íë¨í ě ěë¤. Lee(2015)ě ě°ęľŹë 2009 4ě~2010ë

3ěě KOSPI 200 ě§ěě 돟ěěĽěě 체결ëě 기ě¤ěźëĄ HFTěě ęľë´ę¸°ę´ě´ ě°¨ě§íë ëšě¤ě 35.11%ě´ęł ě¸ęľě¸íŹěěę° 57.92%, ę°ě¸íŹěěę° 6.97%ëźęł ëł´ęł íęł ěë¤. ëí ë ë

źëŹ¸ěě HFT뼟 í루ě ě ęˇ ë° ě ě ęłź 졨ě죟돸ě 모ë íŹí¨íěŹ 2,190í ě´ěě 죟돸ě ě ěśíë ęą°ëěëĄ ě ěíęł ěë¤. HFT뼟 ě´ëťę˛ ě ěíëę°ě ë°ëź ě´ ëšě¨ě´ ëŹëźě§ę˛ ě§ë§, ě 체 HFTě 1/3 ë´ě¸ëĽź ě°¨ě§íë ęľë´ę¸°ę´íŹěěę° IOCęą°ëě ěꡚě ě¸ ě´ě ëĄë ë¤ěęłź ę°ě ę˛ě ë¤ ě ěě ę˛ě´ë¤. 첍째, ęľë´ę¸°ę´íŹěěě 죟돸ě˛ëŚŹěëę° IOCęą°ë뼟 죟ëíë ě¸ęľě¸íŹěěě 죟돸ě˛ëŚŹěëě ëší´ ë§ě´ ëë ¤ ěë경ěěě ë°ëŚŹęą°ë, ë째, ęľë´ę¸°ę´íŹěěë¤ě´ IOCę´ë ¨ ěęł ëŚŹěŚęą°ë뼟 íě§ ěë 경ě°ě´ë¤. ëí ë ę°ě§ ě´ě ę° ëŞ¨ë í´ëšë ěë ěë¤.

<꡸댟 1>ě í¨ë Aë IOC죟돸곟 non-IOC죟돸 ę°ę°ě ëí´ ěŁźëŹ¸ í ęą´ëš íęˇ ěŁźëŹ¸ëě ěźěëłëĄ ꡸댰 ę˛ě´ë¤. IOC죟돸ě ę˛˝ě° ěźëł ęą´ëš íęˇ ěŁźëŹ¸ëě ëëśëś 5ęłě˝ěě 31ęłě˝ ěŹě´ě ëśíŹëĽź ëł´ě´ęł ěěźëŠ° ě˝ëĄë19 íŹë°ëŻš ě´í ęłě˝ëě´ ěŚę°íęł ěěě ëł´ěŹěŁźęł ěë¤. ë°ëŠ´ non-IOC 죟돸ě ěŁźëŹ¸ęą´ëš íęˇ ěŁźëŹ¸ěëě 5ęłě˝ 미ë§ěźëĄ íŹë°ëŻš ě íě 기ę°ě í° ě°¨ě´ëĽź ëł´ě´ě§ ěęł ěë¤.

<꡸댟 1>

죟돸ëęłź 체결ëě ěęłě´

í¨ë Aë íëł¸ę¸°ę° ëě 122ěźě ęą°ëěźěě IOC죟돸곟 non-IOC 죟돸 ę°ę°ě ëí´ ěŁźę°ě§ěě 돟ęłě˝ě 죟돸 ęą´ëš íęˇ ěŁźëŹ¸ëě ëíë¸ ę˛ě´ë¤. í¨ë Bë IOCě non-IOC 죟돸 ę°ę°ě ëí´ ěźëł 체결ëě ëíë¸ë¤.

<꡸댟 1>ě í¨ë Bë IOCě non-IOC 죟돸 ę°ę°ě ëí´ě ě ęˇęą°ëěę°ëě 체결ë ě 체 ęłě˝ě ě뼟 ěźěëłëĄ ꡸댰 ę˛ě´ë¤. IOC죟돸ě 체결ëě´ ě˝ëĄë19 íŹë°ëŻš ě´ě ěë non-IOC죟돸ě ęą°ëëëł´ë¤ ě˝ę° ě ěěźë ě´íěë ꡸ ë°ëëĄ ëíëŹë¤. ëí ë 죟돸ě 체결ë 모ë ě˝ëĄë íŹë°ëŻš ě§í ę¸ę˛Šíę˛ ěŚę°íěěźë ě´í ěŚę°ě¸ë ëŠěśěęł ë¤ě ě´ě ě ěě¤ěźëĄ ëěę°ë 모ěľě ëł´ě´ęł ěë¤.

2.3 ęł ëšëęą°ëě ěŹëĄ

본 ě ěěë KOSPI200 죟ę°ě§ěě 돟ěěĽěě IOCěŁźëŹ¸ě´ ě´ë í ííëĄ ë§¤ë§¤ę° ëęł ěëě§ëĽź ě뼟 íľí´ ě´í´ëł´ë ¤ íë¤. IOC죟돸ě ě¤íěë ěěĽě ëí ě¤ěę° ëŞ¨ëí°ë§ ëĽë Ľęłź ěěĽí경ě ëłíě ë§ěśě´ ě ěíę˛ ěŁźëŹ¸ě ě ěśí ě ěë ëš ëĽ¸ 죟돸ěě¤í

ě´ íěíë¤. ë°ëźě IOC죟돸ěë ëëśëś ęł ëšëęą°ëě(high-frquency trader; HFT)ëźęł ëłź ě ěë¤. SEC(2014)ě ëł´ęł ěě ěí늴 ęł ëšë ęą°ëě ëľě ë§ěźëŠě´íšě ëľ(market-making strategy)ęłź 기íęą°ëě ëľ(opportunistic trading strategy)ěźëĄ 꾏ëśë늰, 기íęą°ëě ëľě ë¤ě ě°¨ěľęą°ë(arbitrage)ě ë°ŠíĽěąęą°ë(directional trading)ě ëľěźëĄ 꾏ěąëë¤ęł íë¤. ë°ŠíĽěąęą°ëě ëíě ě¸ ě ëľě 죟돸ě츥(order anticipation)ęłź 모ëŠí

ě´ęˇ¸ëě

(momentum ignition)ě´ ěë¤. 먟ě íęľě KOSPI200 ě 돟ěěĽěě íëíë ęł ëšëęą°ëěě ë§ěźëŠě´íšě ëľě ěŹëĄëĽź ě´í´ëł¸ íě ë°ŠíĽěąęą°ëě ěźě˘

ěźëĄ ëłź ě ěë IOC ëë°ë§¤ë§¤ëĽź ě´í´ëł¸ë¤.

<í 3>ě í¨ë Aë 2019ë

12ě 2ěź ě¤ě 9:14:07:563ëśí° 9:14:09:404ęšě§ 1.841ě´ ëě 12ęą´ě 매ë죟돸ě ě ěśíë ëěź ęł ëšë ë§ěźëŠě´ěť¤ě ęą°ëěŹëĄëĽź ë°ěˇí ę˛ě´ë¤.1) ě´ ë§ěźëŠě´ěť¤ë 4ęłě˝ ęˇëިě 매ë죟돸ě 매ëę°ę˛Šě ë°ëłľíěŹ ě ě íęł ěë¤. 첍íě 죟돸ěę° 9:14:07:563ěë 280.55íŹě¸í¸ě ę°ę˛ŠěźëĄ ě´ě ě 죟돸ě ě ě íëë° ě´ ë§¤ë죟돸ę°ę˛Šě ěľě°ě 매ëí¸ę°ëł´ë¤ 1.50íŹě¸í¸ ëě ę°ę˛Šě´ë¤. ě´ě˝ęł 0.107ě´ íě ěľě°ě 매ëí¸ę°ě¸ 279.05íŹě¸í¸ě ę°ę˛ŠěźëĄ 죟돸ę°ę˛Šě ě ě íěŹ ě ěśíë¤. íě§ë§ 0.002ě´ ě´í ë¤ě ěëě ěľě°ě 매ëí¸ę°ě¸ 280íŹě¸í¸ëĄ ě ě ě ěśíë¤. ě¤ę°ěě ě¸ 9:14:08:146ě 죟돸 졨ě뼟 ě¤ííě§ë§ ëěźěę°ě ë¤ě ě ęˇěŁźëŹ¸ě íëŻëĄ ě¤ě ëĄë ě ě 죟돸곟 ëěźí 죟돸íí뼟 ë°ëłľíë¤ęł ëłź ě ěë¤.

<í 3>

ęł ëšëęą°ëě ěŹëĄ

í¨ë Aë 2019ë

12ě 2ěź 9:14:07:563ëśí° ę´ě¸Ąë 매ë ë§ěźëŠě´íš ě ëľě ë°ěˇí ę˛ě´ęł í¨ëBë ěęłź ě ěŹí ěę°ëě ę´ě¸Ąë 매ě ë§ěźëŠě´íš ě ëľě ë°ěˇí ę˛ě´ë¤. í¨ë Cë ëěź 14:02:17: 029ëśí° 14:02:17:045ęšě§ě 0.016ě´ ëě 매ě IOC ëë°ë§¤ë§¤ě ěŹëĄëĽź ě ěíęł ěë¤.

í¨ë A: ë§ěźëŠě´íšě ëľ(매ë íí¸)

í¨ë Bë ëěź ęłě˘ëĄ ěśě ëë ë§ěźëŠě´ěť¤ě 매ěęą°ë뼟 ěě í¨ë Aě ëěźí ěę°ëëĄëśí° ë°ěˇí ę˛ě´ë¤. ěě í¨ë Aěě ë§ěźëŠě´ěť¤ę° ě ěśí 첍 ë˛ě§¸ 죟돸ě 죟돸ë˛í¸ę° 70321ě´ęł í¨ë Bě 첍 ë˛ě§¸ 죟돸ë˛í¸ę° 70322ëĄě ě°ěë ěŤěě´ëŻëĄ í´ëš ë§ěźëŠě´ěť¤ë 매ëě 매ě죟돸ě ëěě ě´ěŠíë ě íě ě¸ ë§ěźëŠě´íšě ëľě 꾏ěŹíë¤ęł íë¨í ě ěë¤. 매ě 죟돸 ěě ěľě°ě 매ěí¸ę°ě ě´ëł´ë¤ 1.50íŹě¸í¸ ëŽě 277.5íŹě¸í¸ě 매ěí¸ę° ě¤ěě ëěěě´ ěŁźëŹ¸ę°ę˛Šě ě ě íęł ěěě ě ě ěë¤. í¨ë Aě í¨ë Bě 죟돸ëŠěě§ëĽź íľí´ě ě´ ë§ěźëŠě´ěť¤ë 매ěě 매ë 모ë ěľě°ě í¸ę°ëĽź 기ě¤ěźëĄ 1.5íŹě¸í¸ 깰댏ě í¸ę°ě ěľě°ě í¸ę° ěŹě´ěě 죟돸ę°ę˛Šě ë°ëłľ ě ě í늴ě íŹě§ě

ě ě ě§íë ě ëľě 졨íë¤ęł ëłź ě ěë¤. 본 ë§ěźëŠě´íšě ëľěěë ě´ ęą°ëŚŹëĽź 매ěě 매ë 모ë 1.5íŹě¸í¸ 깰댏뼟 ě ě§íęł ěě§ë§ ë§ěźëŠě´ěť¤ě ěŹęł ě ëľě´ ëŹëźě§ęą°ë ěěĽě ëłëěąęłź ě¤íë ë ëë ěěĽěŹëę° ëłíë ę˛˝ě° ęˇ¸ 깰댏ë ě¸ě ë ě§ ëłí ě ěë¤.

íęľě ěěĽěě íëíë ęł ëšëęą°ëě ëí´ ëŹ¸íěě ëł´ęł ë ę˛ě Chung et al.(2014) ěě ě ěí íęľěŁźěěěĽěěě ě ëľě ë°ëłľěŁźëŹ¸(strategic runs)ęłź Choi(2022)ě´ ě ěí KOSPI200 ě§ěěľě

ěěĽěěě IOCëë°ë§¤ë§¤ę° ěë¤.2) ě ëľě ë°ëłľěŁźëŹ¸ęłź IOC ëë°ë§¤ë§¤ë KOSPI200 ě§ěě 돟ěěĽěěë ę´ě¸Ąëëë° <í 3>ě í¨ëCë 2019ë

12ě 2ěź ě¤í ěę°ëěě ë¤ěě ęł ëšëęą°ëěëĄëśí° ě ěśë IOCëë°ë§¤ë§¤ëĽź ë°ěˇí ę˛ě´ë¤. 모ë 죟돸ě IOC죟돸ěźëĄ ě ěśí ę˛ě¸ë° 첍 죟돸ěę°ě 14:02:17:029ě´ęł ë§ě§ë§ 죟돸ěę°ě 14:02: 17:029ëĄě ě´ 24ę°ě ěŁźëŹ¸ě´ ë°ěí ë 경곟ë ěę°ě 0.016ě´ě´ë¤. 모ë 매ě죟돸ě´ęł 죟돸ę°ę˛Šě 277.8íŹě¸í¸ě´ëŠ° 죟돸ěëě ěľě 1ęłě˝ěě ěľë 109ęłě˝ěźëĄ ëíëęł ěë¤. ě´ 24ę°ě 매ě죟돸 ě¤ěě ě¤ě 체결ëë 죟돸ě ěě ë¤ěŻę°ě 죟돸 ëżě´ë¤. 첍 3ę°ě 죟돸ě 0.001ě´ě ěę° ë¨ěëĄ ě°¨ě´ę° 꾏ëłëě§ ěë ëěźí ěę°ě ě ěśëěęł ëë¨¸ě§ ë ę°ë ě´ëł´ë¤ ę°ę° 0.006ě´ě 0.008ě´ ëŚě ěę°ě ě ěśëěë¤. 6ë˛ě§¸ëśí° 9ë˛ě§¸ 죟돸ě 모ë 5ë˛ě§¸ 죟돸곟 ëěźěę°ě ě ěśëěě§ë§ ěě ě ěśí ë¤ěŻę° IOCěŁźëŹ¸ě´ ěľě°ě 매ëí¸ę°ě ěęł ëĽź 모ë ěě§íěŹ ě˛´ę˛°ě´ ëśę°ëĽíěŹ ëŞ¨ë ěŚě 졨ěë ę˛ěě ě ě ěë¤. ě´ ęą°ëěě íĽëŻ¸ëĄě´ ě ě 6ë˛ě§¸ě 죟돸(죟돸ë˛í¸ 411140)ě 죟돸ěë 85ęłě˝ęłź 죟돸ë˛í¸ 411143, 411146, 411152, 411157, 411162ě 죟돸ěë 55ęłě˝, 죟돸ë˛í¸ 411166, 411168ě 죟돸ěë 19ęłě˝ě 모ë 첍 4ę°ě ěŁźëŹ¸ě´ ě ěśëë ěě ě ěľě°ě 매ëí¸ę°ě ěęł ě ëěźíë¤ë ě ě´ë¤. ě´ëĄëśí° ëŻ¸ëŁ¨ě´ ě ěśí ě ěë ěŹě¤ě, ě˛´ę˛°ëĄ ě°ę˛°ëě§ ëŞťíęł ěˇ¨ěëë ě´ë¤ ëë¨¸ě§ 19ę° IOC죟돸ë¤ě ě ě´ě 체결ě 몊ě ěźëĄ 죟돸ě ě¤ííě§ë§ ěę°ě ěźëĄ ěě ë¤ěŻę°ě 죟돸 ě ěśěěě ěë경ěě ë°ë ¤ 체결ě ě¤í¨íěë¤ë ě ě´ë¤. ë¤ě ë§íěŹ ëë¨¸ě§ IOC죟돸ě ěśěë¤ě ěëě ěźëĄ 졨ěë ę˛ě ě§ěíęł ě ěľě°ě 매ëí¸ę°ëł´ë¤ 0.05íŹě¸í¸ ëŽě 매ěí¸ę°ëĽź ě ěśí ę˛ě´ ěëëźë ě ě´ë¤.

<í 4>ë í본 기ę°ě KOSPI 200 ě 돟ěěĽě ěźě¤ ě ě매매ěę°ëě ë°ěí ę¸¸ě´ 3 ě´ěě¸ IOC ëë°ë§¤ë§¤ě 길ě´ëł ëśíŹě ę°ę°ě ëë°ë§¤ë§¤ěě ěąęłľëĽ ě ě 댏í ę˛ě´ë¤. ěŹę¸°ě ěąęłľě´ë 죟돸ěë ě¤ ěľě 1ę° ě´ě ě 돟ęłě˝ě´ 체결ë 경ě°ëĽź ě미íë¤. <í 4>ěě ę°ěĽ ë§ě ëë°ë§¤ë§¤ě 길ě´ë 5~9ę°ěě ę°ěĽ ë§ěęł ěąęłľëĽ ě 3-4ę°ěě ę°ěĽ ë§ěë¤. ëí IOC ëë°ë§¤ë§¤ě íęˇ ěąęłľëĽ ě 18.4%ëĄ ëíëŹë¤.

<í 4>

IOC ëë°ë§¤ë§¤ě ëśíŹ

ěëě íë íëł¸ę¸°ę° ëě 122ěźě ęą°ë기ę°ěě ě ě매매ěę°ě¸ 9:00ëśí° 15:35ęšě§ ë°ěí IOCëë°ë§¤ë§¤ě ëśíŹě ěąęłľëĽ ě ě 댏í ę˛ě´ë¤.

2.4 IOC 죟돸ě ęą°ëěëë°Š ëśě

IOC죟돸ě ëëśëśě ě¸ęľě¸ ęą°ëěë¤ě´ ě ěśíęł ěëë° ě´ ěŁźëŹ¸ë¤ě ęą°ëěëë°Šě ë꾏ě¸ę°? 본ě ě ě´ ě§ëŹ¸ě ëľíęł ěë¤.

<í 5>ě í¨ë Aë í본기ę°ě 122ěźě ęą°ëěź ëě KOSPI 200 죟ę°ě§ěě 돟ęłě˝ěě ě¸ ę°ě§ ě íě íŹěěęˇ¸ëŁšëł ë§¤ë ęą°ëëě ě 체매ěęą°ëě ëí´ ëë 매ě죟ëęą°ëě ëí´ ę°ę° ě 댏í ę˛ě´ë¤. ě 체ě§ěě 돟ě 매ëëě¸ 31,605,520 ęłě˝ ě¤ ě¸ęľě¸íŹěěě 매ëęłě˝ěë 21,748,580 ęłě˝ě´ęł , ę°ě¸íŹěěę° 6,702,047 ęłě˝ ęˇ¸ëŚŹęł ę¸°ę´íŹěěę° 3,154,893 ęłě˝ěźëĄ ë¤ëĽź ě´ěë¤. íí¸ ě 체 매ě죟ëęą°ëě ęłě˝ěë ě´ 15,762,732ę°ě¸ë° ě´ě¤ 64.52%뼟 ě¸ęľě¸íŹěěę° ęą°ëěëë°Šě´ ëěęł , 기ę´ě´ 10.56%, ę°ě¸íŹěěę° 24.91%ě ëšě¨ëĄ ęą°ëěëë°Šě´ ëě´ ęą°ë뼟 체결íěë¤. ě¸ęľě¸íŹěěě ę˛˝ě° ë§¤ě죟ëęą°ëěě ëí ęą°ë ěëë°ŠěźëĄěě ëšě¨ě ě 체매ěęą°ëěě ëí ęą°ëěëë°Šëšě¨ëł´ë¤ ëŽę˛ ëíëŹěźëŠ° ę°ě¸íŹěěë ě´ëł´ë¤ ëę˛ ëíëŹë¤. 매ě죟ëęą°ëěë ěěĽę°ěŁźëŹ¸ ëë ěěĽěąě§ě ę°ěŁźëŹ¸ě ě ěśí ęą°ëěëĄě í´ëš ęą°ëě ëí´ ë§¤ě° ě ꡚě ě¸ ě˛´ę˛° ěě§ëĽź ę°ęł ěë ë°ëŠ´ ě´ ěŁźëŹ¸ě ęą°ëěëë°Šě stale priceě 죟돸ěě´ęą°ë pick-offě ëěě´ ëë ęą°ëěëĄěě ę°ëĽěąě´ ëë¤ęł ëłź ě ěë¤. 매ě죟ëęą°ë뼟 ë¤ě IOCëë°ë§¤ë§¤, IOCëšëë°ë§¤ë§¤, non-IOC죟ëęą°ë ě¸ę°ě§ëĄ 꾏ëśíěŹ ęą°ëěëë°Šě 쥰ěŹí 결곟, IOCëšëë°ë§¤ë§¤ě non-IOC죟ëęą°ëě ęą°ëěëë°Šëšě¨ě ě 체매ěęą°ëě ëí ęą°ëěëë°Šëšě¨ęłź í° ě°¨ě´ëĽź ëł´ě´ě§ ěěě§ë§, IOCëë°ë§¤ë§¤ě ëí ęą°ëěëë°Šëšě¨ě íŹę˛ ëłííë ę˛ěźëĄ ëíëŹë¤. 꾏체ě ěźëĄ ě¸ęľě¸íŹěěë IOCëë°ë§¤ë§¤ě ëí ęą°ëěëë°Šëšě¨ě´ 15.83% íŹě¸í¸ ę°ěí ë°ëŠ´ 기ę´íŹěěë 2.97% íŹě¸í¸ ěŚę°íěęł ę°ě¸íŹěěě ęą°ëěëë°Šëšě¨ě 12.86% íŹě¸í¸ ěŚę°íěë¤.

<í 5>

IOC죟돸ě ęą°ëěëë°Š ëśíŹ

í¨ë Aë í본기ę°ě 122ěźě ęą°ëěź ëě KOSPI 200 죟ę°ě§ěě 돟ęłě˝ěě ě¸ ę°ě§ ě íě íŹěěęˇ¸ëŁšëł ë§¤ë ęą°ëëě ě 체매ěęą°ëě ëí´ ëë 매ě죟ëęą°ëě ëí´ ę°ę° ě 댏í ę˛ě´ë¤. 매ě죟ëęą°ëë IOC죟돸ě ěí´ ěŁźëë ę˛ě¸ě§ ěŹëśëĽź 꾏ëśíěŹ ęłě°íěęł , IOC죟ëęą°ëë ë¤ě IOC ëë°ë§¤ë§¤(herd)ě ěŹëśëĄ ë 꾏ëśíěŹ ě 댏íěë¤. í¨ëBë ëěźí ěë šěźëĄ íŹěě ęˇ¸ëŁšëł ë§¤ěęą°ëëě ě 댏í ę˛ě´ë¤.

í¨ë A: íŹěě ęˇ¸ëŁšëł ë§¤ëëęłź ëśíŹ

<í 5>ě í¨ë Bë 매ëęą°ëě ëí´ íŹěěëł ęą°ë ěëë°ŠěźëĄěě ęą°ëęłě˝ěě ëšě¨ě ě 댏í ę˛ě´ë¤. ꡸ 결곟ë ěě í¨ë Aě íŹę˛ ë¤ëĽ´ě§ ěë¤. ě¸ęľě¸íŹěěë IOCëë°ë§¤ë§¤ě ëí ęą°ëěëë°Šëšě¨ě´ ěźë°ë§¤ë§¤ě ëší´ 15.85% íŹě¸í¸ ę°ěí ë°ëŠ´ 기ę´íŹěěë 3.12% íŹě¸í¸ ěŚę°íěęł , ę°ě¸íŹěěë 12.73% íŹě¸í¸ëĄ íŹę˛ ěŚę°í ę˛ěźëĄ ëíëŹë¤. ě´ ę˛°ęłźë ę°ě¸íŹěěę° ë¤ëĽ¸ íŹěěě ëší´ě ęą°ëě°¸ěŹëšě¨ ëëš IOCëë°ë§¤ë§¤ě ęą°ëěëë°ŠěźëĄě ë ëě ëšě¨ě ě°¨ě§íë ę˛ě ëł´ěŹěŁźë ę˛ě¸ë°, ě´ë ěë§ë ę°ě¸íŹěěę° ěŹěŠíë ęą°ëíëŤíźě 죟돸ěëę° ěëě ěźëĄ ë댏기 ë돸ě ěěĽěíŠě ë§ę˛ 죟돸ę°ę˛Šě ě ěě 쥰ě í기 ě´ë ¤ě ě˝ę˛ ęł ëšë IOC ëë°ë§¤ë§¤ě íě ě´ ë ę°ëĽěąě´ ëë¤ë ě ě ěěŹíë¤.

3. 죟돸íëŚě ëśęˇ í ëśě

죟돸íëŚëśęˇ í(order flow imbalance; OFI)ě´ë ě ě죟돸ěěĽěě 매ěě 매ë죟돸ě ëśęˇ íě ëíë ěěšě´ë¤. ě°ëŚŹë ěŹę¸°ě ěľě°ě 매ěě 매ëí¸ę°ëĽź ëíë´ë 죟돸ě§ęłěĽě ë 벨1ë§ě ęł ë ¤íë¤. Cont et al.(2014)ë 죟돸íëŚëśęˇ íě 츥ě íë íëě ë°Šë˛ěźëĄ ë¤ěě ě ěíěë¤. ë§ě˝ ëłě eně në˛ě§¸ě ěŁźëŹ¸ě´ ë§¤ěë° ë§¤ëě ë기죟돸ëě 기ěŹíë ě ëëź ě ěíë¤ëŠ´ ꡸ ěě ë¤ěęłź ę°ë¤.

ěŹę¸°ě 1Aě Aę° ěŹě¤ěź ę˛˝ě° 1ě ę°ě ę°ęł ꡸ë ě§ ěě ę˛˝ě° 0ě ę°ě ę°ë íěí¨ě(indicator function)ě´ë¤. ě´ě¸ěë ěěë në˛ě§¸ 죟돸ěě ě ěľě°ě 매ěí¸ę°(Pnb), ěľě°ě 매ëí¸ę°(Pns), ěľě°ě 매ěí¸ę°ě ěë(qnb), ęˇ¸ëŚŹęł ěľě°ě 매ëí¸ę°ě ěë(qns)ě´ íŹí¨ëě´ ěë¤. ë§ě˝ Pnbě´ ëłëíě§ ěě ěíěě qnbë§ ěŚę°íë¤ëŠ´, ě´ë ě ęˇ ě§ě ę°ěŁźëŹ¸ě 매ě죟돸ę°ę˛Šě´ 기쥴ě ěľě°ě 매ěí¸ę°ě ëěźíęł í¸ę°ěęł ę° q n b â q n â 1 b q n b â q n â 1 b â q n â 1 b

ě°ëŚŹë ëłě eně 죟돸ě íě ë°ëź ëę°ě íí¸ëĄ ëë ě ěë¤. íëë Non-IOC (enNIOC) 죟돸ě ěí ę˛ě´ęł ë¤ëĽ¸ íëë IOC order(enIOC) 죟돸ě ěí ę˛ě´ë¤. ě´ëĽź ěěźëĄ ííí늴 ë¤ěęłź ę°ë¤.

ěę°ę°ę˛Š [tk-1,tk]ěě 죟돸íëŚëśęˇ í(OFI)ě ě´ ęľŹę°ěě ë°ěí ę°ę°ě eně 모ë íŠí ę˛ěźëĄě ěěźëĄ ëíë´ëŠ´ ë¤ěęłź ę°ë¤.

ěŹę¸°ě N(t)ë ęľŹę° [0, t]ěě ě´ë˛¤í¸ě ę°Żěě´ë¤. íí¸ ëěź ęľŹę°ěě íęˇ ę°ę˛Šě ëłíë ë¤ěęłź ę°ě´ ě ěëë¤.

ěŹę¸°ě Pkbě Pksë ěě tkěěě ěľě°ě 매ěí¸ę°ě ěľě°ě 매ëí¸ę°ëĽź ę°ę° ëíë´ęł , δ ë ííąě íŹę¸°ě´ë¤. íěŹ KOSPI 200 ě§ěě 돟ěě ííąě íŹę¸°ë 0.05 íŹě¸í¸ě´ë¤.

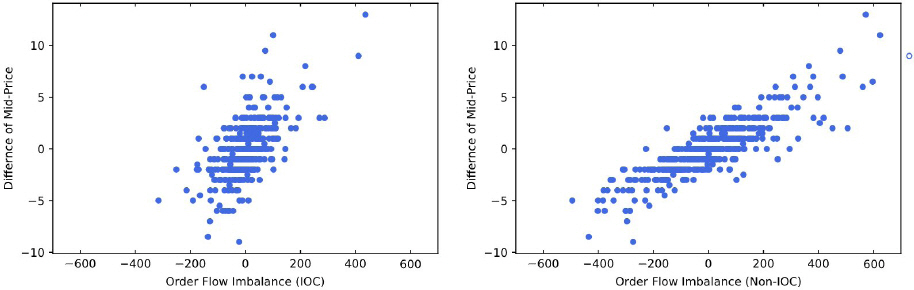

ě´ě Cont et al.(2014)ě 모íě íěĽíěŹ ę°ę˛Šëłíě IOCë° non-IOC 죟돸 ę°ę°ěźëĄëśí° ěźę¸°ë OFI ěŹě´ě´ ę´ęłëĽź ë¤ěě ěěźëĄ ę˛ěŚí´ 본ë¤.

ěŹę¸°ě ÎPk,ië íšě ěź iě ęľŹę° [tk-1,tk]ěěě ě¤ę°ę°ę˛Šě ëłíëě ëíë´ęł , OFIk,ië 죟돸íëŚëśęˇ íě ëíë¸ë¤. ëí βiNIOCě βiIOCë non-IOC죟돸곟 IOC 죟돸 ę°ę°ě ëí ę°ę˛ŠěśŠę˛Šě ëíë´ë íęˇęłěě´ęł âk,ië ě¤ě°¨íě´ë¤.

<í 6>ě ě (5)ě íęˇëśě결곟뼟 ě 댏í ę˛ě´ë¤. ëśě결곟 IOC죟돸ě ę°ę˛ŠěśŠę˛Šęłě (βiIOC)ę° non-IOC죟돸ě ęłě(βiNIOC)ëł´ë¤ íŹę˛ ëíëŹëë° ě´ë IOC죟돸ě ěí´ ë°ěíë 죟돸ëśęˇ íě´ non-IOC죟돸ě ëší´ ę°ę˛Šëłëěąě ëë°° ě´ěě ěíĽě ě¤ë¤ë ę˛ě ěěŹíë¤. 122ěě ęłě(βiIOC, βiIOC)ë 모ë 1%ě ěě¤ěě íľęłě ěźëĄ ě ěíěęł ěě R2ę°ě ěľě 33.4%, ěľë 82.9%ě´ęł íęˇ ěě R2ě 64.7%ëĄ ëíëŹë¤. ëí ë ęłěę°ě ě°¨ě´ę° ěëě§ ěŹëśëĽź ěě보기 ěíěŹ ě체ëšęľę˛ě (paired t-test)ě ě¤ěíěëë°, tę°ě´ 23,77ëĄě 1%ě ěě¤ěě íľęłě ěźëĄ ě ěíę˛ ě°¨ě´ę° ěë ę˛ěźëĄ ëíëŹë¤.

<í 6>

OFIě íęˇ ę°ę˛Š ěŹě´ě íęˇëśě결곟

본 íë IOCě non-IOC죟돸ěźëĄëśí° ěźę¸°ë 죟돸íëŚëśęˇ í(OFI)ęłź ę°ę˛Šëłë ěŹě´ě ę´ęłëĽź 쥰ěŹí기 ěí´ ěíë ěëě íęˇëśě모í(ě (5))ě 결곟뼟 ě 댏í ę˛ě´ë¤.

***ë 122ę°ě 결곟ěšę° 모ë 1%ě ěě¤ěě íľęłě ěźëĄ ě ěí¨ě ě미íë¤.

| Adj R2 | βNIOC | βIOC | |

|---|---|---|---|

| íęˇ | 0.647 | 0.004*** | 0.009*** |

| ě¤ěę° | 0.650 | 0.003 | 0.009 |

| íě¤í¸ě°¨ | 0.086 | 0.002 | 0.002 |

| ěľěę° | 0.334 | 0.001 | 0.005 |

| ěľëę° | 0.829 | 0.013 | 0.018 |

<꡸댟 2>ë ěľě°ě 매ě ë° ěľě°ě 매ëí¸ę°ě íęˇ ę°ę˛Š(ě´í âíęˇ ę°ę˛Šâě´ëź ëśëŚ)ě ě°¨ě´ě 죟돸íëŚëśęˇ í(OFI) ěŹě´ě ě°ě ë뼟 ꡸댰 ę˛ě´ë¤. í¨ë Aë IOC죟돸ěźëĄëśí° ěźę¸°ë OFIě íęˇ ę°ę˛Š ěŹě´ě ě°ě ë뼟, í¨ë Bë non-IOCëĄëśí° ěźę¸°ë OFIě íęˇ ę°ę˛Š ěŹě´ě ě°ě ë뼟 ę°ę° ꡸댰 ę˛ě´ë¤. ë ꡸댟ě ëíë ě°ě ëę° íěąí ë ëłě ěŹě´ě 기ě¸ę¸°ëĽź íľí´ě ě§ěí ě ěëŻě´ IOC죟돸ěźëĄëśí° ěźę¸°ë OFIě ę°ę˛ŠěśŠę˛Šě´ non-IOC죟돸ě ę°ę˛ŠěśŠę˛Šëł´ë¤ íŹę˛ ëíëęł ěěě ě ě ěë¤. ě´ë <í 5>ě íęˇëśě결곟ě ěźěšíë ę˛ě´ë¤. ëí 본 결곟ë IOCěŁźëŹ¸ě´ non-IOC죟돸ě ëší´ ěěĽě ëłëěąě ë ěŚę°ěí¤ë ę˛ěě ěěŹíë¤.

<꡸댟 2>

OFI ě íęˇ ę°ę˛Šě ę´ęł

ěëě ꡸댟ě 매 30ě´ë§ë¤ 츥ě ë 죟돸íëŚëśęˇ í(OFI)ęłź íęˇ ę°ę˛Š(mid-price) ěŹě´ě ě°ě ë뼟 ꡸댰 ę˛ě´ë¤. í¨ë Aë IOC죟돸ě ëíë´ęł í¨ë Bë non-IOC죟돸ě ëíë¸ë¤. ꡸댟ě ę´ě¸Ąěě ě 2020ë

8ě 25ěź, 9:00amëśí° 12:30pmęšě§ě´ë¤.

4. 체결ěěěę°

ëšěěĽěą ě§ě ę°ěŁźëŹ¸ě ęą°ëěëë°Šě´ ëíëęą°ë ěŁźëŹ¸ě´ ěˇ¨ěë기 ě ęšě§ë picking-off 댏ě¤íŹě ë

¸ěśëë¤. ë¤ëĽ¸ ěĄ°ęą´ě´ ëěźí ę˛˝ě° ěŁźëŹ¸ě§ęłěĽě ë기íë ěę°ě´ 길ěëĄ ě´ ěíě ë ë§ě´ ë

¸ěśëë¤ęł ëłź ě ěë¤. 본 ěĽěěë ěěě ëšěěĽěą ěŁźëŹ¸ě´ ě ěëęł ě˛´ę˛°ë ë ęšě§ě ěę°, ěŚ ě˛´ę˛°ěěěę°(time to execution)ě 츥ě íěŹ ę¸°ę´, ę°ě¸, ě¸ęľě¸íŹěě ëą ě¸ę°ě§ íŹěěě íęłź IOC죟돸 ěě¸ě´ 체결ěę°ě ěíĽě 죟ëě§ ěŹëśëĽź 쥰ěŹíë¤.

<í 7>ě ě¸ę°ě§ íŹěě ě íëłëĄ ëšěěĽěą ě§ě ę°ěŁźëŹ¸ě ëí´ ěŁźëŹ¸ëśí° 체결ë ëęšě§ě ěę°ě ëśěíěŹ ě 댏í ę˛ě´ë¤. í¨ë Aë íŹěě ě íëłëĄ ě ěśí 매ëěŁźëŹ¸ě´ ě˛´ę˛°ë ëęšě§ě ěę°ě ě 댏í ę˛ě´ë¤. â매ě죟ëęą°ë ě 체âě íě íěë 체결ěę°ě ę° íŹěě ě íëłëĄ ě ěśí ěŁźëŹ¸ě´ ë§¤ě죟ëęą°ëěě ěí´ ě˛´ę˛°ë 경ě°ě íęˇ ě˛´ę˛°ěę°ě ëíë¸ë¤. ëí 매ě죟ëęą°ëěę° (a) IOC매ěěě¸ě§ íšě (b) non-IOC매ěěě¸ě§ëĽź 꾏ëśíěŹ ě˛´ę˛°ěę°ě ęłě°íěęł ěě¸ëŹ IOC매ěěë (a-1) IOCëë°ë§¤ë§¤ (IOC herd) 매ěěě¸ě§ íšě (a-2) IOC ëšëë°ë§¤ë§¤(IOC non-herd) 매ěěě¸ě§ëĽź 꾏ëśíěŹ ě˛´ę˛°ěę°ě ęłě°íěŹ ě 댏íěë¤. ęą°ëěëë°Šě´ IOC 매ě죟돸ěě¸ě§ íšě ěźë°ë§¤ě죟돸ěě¸ě§ě ë°ëźě 체결ěę°ě íŹę˛ ě°¨ě´ę° ěë ę˛ěźëĄ 쥰ěŹëěë¤. ęą°ëěëë°Šě´ IOC ëë°ë§¤ë§¤ 죟돸ěźëĄ ęą°ë뼟 ě ě˛í ę˛˝ě° ëŞ¨ë íŹěě ě íěě 체결ěę°ě´ ëí íë˝íěëë° ě¸ęľě¸ě ę˛˝ě° 35.9ě´ěě 16.0ě´ëĄ íë˝íěęł , 기ę´ě ę˛˝ě° 116.2ěě 27.9ě´ëĄ íë˝íěěźëŠ°, ę°ě¸ě 110.3ě´ěě 42.0ě´ëĄ íë˝íěë¤. íě§ë§ ęą°ë죟ëěę° ěźë°ěŁźëŹ¸ě ě ě˛í ę˛˝ě° ě˛´ę˛°ěę°ě ě¤íë ¤ ë íŹę˛ ëíëŹë¤. ě¸ęľě¸ě 51.1ě´ëĄ, 기ę´ě 210.1ě´ëĄ, ę°ě¸ě 189.4ě´ëĄ ę°ę° ë í° ę˛ěźëĄ ëíëŹë¤. ě´ëŹí 결곟ë íŹěě ě íëłëĄ ě ěśí 매ěěŁźëŹ¸ě´ ě˛´ę˛°ë ëęšě§ě ěę°ě ě 댏í í¨ë Běěë ě ěŹíę˛ ëíëŹë¤.

<í 7>

íŹěě ęˇ¸ëŁšëł ě˛´ę˛°ěę°

본íë ě¸ ę°ě§ íŹěě ě íëłëĄ ëšěěĽěą ě§ě ę°ěŁźëŹ¸ě ëí´ ěŁźëŹ¸ëśí° 체결ë ëęšě§ě ěę°ě ëśěíěŹ ě 댏í ę˛ě´ë¤. í¨ëAë íŹěě ě íëłëĄ ě ěśí 매ëěŁźëŹ¸ě´ ě˛´ę˛°ë ëęšě§ě ěę°ě ě 댏í ę˛ě´ë¤. 매ě죟ëęą°ëě ě ěë 체결ěę°ě ę° íŹěě ě íëłëĄ ě ěśí ěŁźëŹ¸ě´ ë§¤ě죟ëęą°ëěě ěí´ ě˛´ę˛°ë 경ě°ě íęˇ ě˛´ę˛°ěę°ě ëíë¸ë¤. ëí 매ě죟ëęą°ëěę° IOC매ěěě¸ě§ íšě non-IOC매ěěě¸ě§ëĽź 꾏ëśíěŹ ě˛´ę˛°ěę°ě ęłě°íěęł ěě¸ëŹ IOC매ěěë IOC herd매ěěě¸ě§ íšě IOC non-herd 매ěěě¸ě§ëĽź 꾏ëśíěŹ ě˛´ę˛°ěę°ě ęłě°íěŹ ě 댏í ę˛ě´ (a), (a-1), (a-2) ë° (b)íě ëíë ěę°ě´ë¤. í¨ëBë ěęłź ëěźí ë°Šë˛ě ěŹěŠíë ë¤ë§ íŹěě ě íëłëĄ 매ě죟돸ě ëí´ ě˛´ę˛°ěę°ě 쥰ěŹíěŹ ě 댏í ę˛ě´ë¤. íěě ěę°ě ë¨ěë ě´(second)ě´ë¤.

í¨ë A: íŹěě ě íëł ë§¤ë죟돸ě 체결ěę°

ě´ ę˛°ęłźëĄëśí° ěťě ě ěë ěěŹě ě ë¤ěęłź ę°ë¤. 첍째, KOSPI 200 죟ę°ě§ěě 돟ěěĽěě IOC 매매ë non-IOC매매ě ëšęľíěŹ ëŞ¨ë 죟돸ě íęˇ ě˛´ę˛°ěę°ě ę°ěěí¤ë í¨ęłźę° ěë¤ë ě ě´ë¤. ë째, IOC ëë°ë§¤ë§¤ę° ëšëë°ë§¤ë§¤ě ëší´ 체결ěę°ě ę°ěí¨ęłźę° ë íŹę˛ ëíëęł ěěźëŠ°, ě

째, IOC매매ě 체결ěę° ę°ěí¨ęłźę° 기ę´ęłź ę°ě¸íŹěěěę˛ë íŹę˛ ëíë ë°ëŠ´ ě¸ęľě¸íŹěěěę˛ë ꡸ ę°ěí¨ęłźę° ěëě ěźëĄ ę°ěĽ ěěë¤. ě´ë ěě ě´í´ëł´ěëŻě´ IOC ëë°ë§¤ë§¤ěě ę°ě¸íŹěěę° ęą°ëěëë°ŠěźëĄěě ěí ě ě 체깰ë ëëš ęą°ëëšě¨ ě´ěěźëĄ íë ę˛ęłź ë°ě í ě°ę´ě´ ěě ę˛ěźëĄ ěśě ëë¤. ëˇě§¸, 기ę´ęłź ę°ě¸ě 체결ěę°ě´ ě¸ęľě¸íŹěěě ëší´ ě ë°ě ěźëĄ ë§ě ę˛ěźëĄ ëíëŹëë°, ě´ë ěëě ěźëĄ ě´ě

í ě ëł´ěě§ ë° ě˛ëŚŹëĽë Ľęłź ë댰 죟돸ěě¤í

ě 기ě¸íë ę˛ěźëĄ íę°ëë¤. ě´ ę˛°ęłźë 기ę´ęłź ę°ě¸íŹěěěę˛ ë

¸ěśë picking-off 댏ě¤íŹę° ě¸ęľě¸íŹěěě ëší´ě ëě ę˛ěě ěěŹíë¤.

5. IOCę° ěěĽíě§ě 미ěšë ěíĽ

본 ěĽěěë IOCěŁźëŹ¸ě´ ěěĽíě§ě 미ěšë ěíĽě ě íľě ě¸ ě§íě¸ í¸ę°ě¤íë ë, ěěĽěŹë, ëłëěą ě¸ĄëŠ´ěě ě´í´ëł¸ë¤. ë

댽ëłěë RunsInIOCëĄě ëë°ë§¤ë§¤ę° ě§ěëë ěę°ě 0.001ě´ ë¨ěëĄ ëíë¸ë¤.3) ěěĽíě§ě ëíë´ë ě˘

ěëłěëĄě í¸ę°ě¤íë ë(quote spread), ěěĽěŹë(market depth), ë¨ę¸°ëłëěą(short-term volatility) ëąě´ ěë¤. í¸ę°ě¤íë ëë ěľě°ě 매ëí¸ę°ě ěľě°ě 매ěí¸ę°ě ě°¨ě´ëĽź ě§ěë ěę°ě 길ě´ë§íź ę°ě¤íęˇ í ę°ě´ë¤. ěěĽěŹëë 죟돸ě§ęłěĽě ë 벨1ëśí° ë 벨5ęšě§ě 모ë 죟돸ěęł ëĽź íŠęłí ěěšě´ęł , ë¨ę¸°ëłëěąě ěľě°ě 매ěí¸ę°ě ěľě°ě 매ëí¸ę°ě íęˇ ě ěľęł ę°ěě ěľě ę°ě ě°¨ě´ëĄ ęłě°ëë¤. <í 8>ě ë

댽ëłěě ě˘

ěëłěë¤ě 기ě´íľęłëě ě 댏í ę˛ě´ë¤.

<í 8>

IOCëë°ë§¤ë§¤ěę°ęłź ěěĽíě§ě§íě 기ě´íľęłë

본 íë ë

댽ëłěëĄě IOCëë°ë§¤ë§¤ě ě§ěěę°ě ëíë´ë RunsInIOCě ěěĽíě§ě ëíë´ë 3ę°ě ě˘

ěëłěě 기ě´íľęłëě ě 댏í ę˛ě´ë¤. í¸ę°ě¤íë ëë ěľě°ě 매ëí¸ę°ě ěľě°ě 매ěí¸ę°ě ě°¨ě´ëĽź ě§ěë ěę°ě 길ě´ë§íź ę°ě¤íęˇ í ę°ě´ë¤. ěěĽěŹëë 죟돸ě§ęłěĽě ë 벨1ëśí° ë 벨5ęšě§ě 모ë 죟돸ěęł ëĽź íŠęłí ěěšě´ęł , ë¨ę¸°ëłëěąě ěľě°ě 매ěí¸ę°ě ěľě°ě 매ëí¸ę°ě íęˇ ě ěľęł ę°ěě ěľě ę°ě ě°¨ě´ëĄ ęłě°ëë¤. 모ë ë°ě´í°ë í본기ę°ě¸ 122ěź ęą°ëěź ě¤ ě ě매매ěę°ëě¸ 9:00ëśí° 15:35(ë§ę¸°ěźěë 15:20)ęšě§ě ěę°ě 10ëś ë¨ěëĄ ëśí íěŹ ě¸Ąě íěěźëŠ° ë°ě´í°ě ę°ěë 모ë ëłě ëš ëěźí 4,752ę°ě´ë¤. RunsInIOCě ë¨ěë 1/1000ě´ě´ęł , í¸ę°ě¤íë ëě ëłëěąě ë¨ěë íŹě¸í¸, ěěĽěŹëě ë¨ěë ęłě˝ěě´ë¤.

ë

댽ëłěě¸ RunsInIOCě ě˘

ěëłě ę°ě ěę´ęłě뼟 쥰ěŹí 결곟, RunsInIOCě í¸ę°ě¤íë ë ěŹě´ěë 2019ë

ě 0.29, 2020ë

ě 0.23ě ěěšëĄ ëíëŹë¤. ëí RunsInIOCě ěěĽěŹë ěŹě´ěë 2019ë

ě -0.41, 2020ë

-0.36ě ěę´ęłěę° ěśě ëěęł , RunsInIOCě ěěĽëłëěą ěŹě´ěë 2019ë

ě 0.76, 2020ë

0.64ě ěę´ęłěę° ëěśëěë¤. ěę´ę´ęł ěěšëĄë§ íë¨í´ëłź ë RunsInIOCë ěěĽíě§ě ëśě ě ě¸ ěíĽě ëźěšë¤ęł ëłź ě ěë¤.

본 ě°ęľŹěěë IOCëë°ë§¤ë§¤ę° ěěĽíě§ě ěíĽě 미ěšë ě ë뼟 ě´í´ëł´ę¸° ěíěŹ, ě ě매매ěę°ëě¸ 9:00ëśí° 15:35ęšě§ ěę°ě 10ëś ę°ę˛ŠěźëĄ ëśí í í Hasbrouck and Saar(2013)ě ë°Šë˛ëĄ ęłź ę°ě´ ë¤ěęłź ę°ě íęˇëśěě ěííë¤.

(6)

ěě ě¸ę°ě 모íěěě t(=1,âŚ,T)ë 10ëśě ěę° ę°ę˛Šě ëíë´ë ě¸ëąě¤ě´ęł , MQtë ěěĽíě§ě ëíë´ë ëłěëĄě ě¤íë ë, ěěĽěŹë, ëłëěą ě¤ íë뼟 ëíë¸ë¤. ëí Maturitytë ě 돟ě ë§ę¸°, TradingVolt-1ë ě 기ě ęą°ëëě´ęł , Rtë í´ëš 기ę°ëěě ëĄęˇ¸ěěľëĽ , | R t |

OLS ěśě ěšë ë´ěěąě´ 쥴ěŹíë ę˛˝ě° ě ě í ěśě ěšę° ë ě ěë¤. íě§ë§ ë´ěěąę˛ěŹëĽź ěíí 결곟 본 모íěěë ëěěą(simultaneity)ě ěí ë´ěěąě´ 쥴ěŹíě§ ěë ę˛ěźëĄ ëíëŹë¤. <í 9>ë OLS 결곟뼟 ě 댏í ę˛ě´ë¤.

<í 9>

IOC죟돸곟 ěěĽíě§ ěŹě´ě íęˇëśě결곟

본 íë IOC ëë°ë§¤ë§¤ę° ěěĽíě§ě 미ěšë ěíĽě ě´í´ëł´ę¸° ěí´ ě (6)ě íęˇëśě모íě 결곟뼟 ě 댏í ę˛ě´ë¤. íęˇëިíěěě t(=1,âŚ,T)ë 10ëśě ěę° ę°ę˛Šě ëíë´ë ě¸ëąě¤ě´ęł , MQtë ěěĽíě§ě ëíë´ë ëłěëĄě ě¤íë ë, ěěĽěŹë, ëłëěą ě¤ íë뼟 ëíë¸ë¤. ëí Maturitytë ě 돟ě ě쥴ë§ę¸°, TradingVolt-1ë ě 기ě ęą°ëëě´ęł , Rtë í´ëš 기ę°ëěě ëĄęˇ¸ěěľëĽ , | R t |

í¨ë A: 2019ë

<í 9>ěě í¨ë Aě í¨ë Bë ę°ę° 2019ë

, 2020ë

ě ë°ě´í°ëĽź ëěěźëĄ ëśěí 결곟ě´ë¤. íěě ę°ěĽ ě¤ěí ěěšë IOCëë°ë§¤ë§¤ę° ěěĽíě§ě ěíĽě 미ěšë ě ë뼟 ëíë´ë ě´ë¤. ě´ ěěšę° 2019ë

ęłź 2020ë

ě íęˇëśě 모ëěě í¸ę°ě¤íë ëě ěěĽëłëěąě ëí´ěë ěěě´ęł ěěĽěŹëě ëí´ěë ěěě´ëŠ°, 모ë ęłěë 1%ě ěě¤ěě íľęłě ěźëĄ ě ěíę˛ ëíëŹë¤. ě´ ę˛°ęłźë IOCëë°ë§¤ë§¤ę° í¸ę°ě¤íë ëě ěěĽëłëěąě ěŚę°ěí¤ęł ěěĽěŹë뼟 ę°ěěěź ěěĽě ě§ě ë¨ě´ë¨ëŚŹë ěě¸ě´ëźë ě ě ěěŹíë¤. ë§ę¸°í¨ęłźę° 미ěšë ěíĽě ëíë´ë ęłě a2ë ě°ëëłëĄ ë¤ëĽ´ę˛ ëíëŹë¤. 2019ë

ëěë ë§ę¸°ěźě ę°ęšě¸ěëĄ ěěĽěŹëę° ěŚę°íë ę˛ěźëĄ ëíë ë°ëŠ´ 2020ë

ëěë ë°ëëĄ ę°ěíë ę˛ěźëĄ ëíëŹë¤. í¸ę°ě¤íë ëë íëł¸ę¸°ę° ě 체ěě ë§ę¸°ěźě ę°ęšě¸ěëĄ ěŚę°íë ę˛ěźëĄ ëíëŹë¤. ë¨ę¸°ëłëěąě 2019ë

ěë ë§ę¸°ěźě ę°ęšě¸ěëĄ ę°ěíěěźë 2020ë

ěë ěŚę°íë ę˛ěźëĄ ëíëŹě§ë§ íľęłě ěźëĄ ě ěíě§ë ěěë¤. ę˛°ëĄ ě ěźëĄ ě§ěě 돟ěěĽěě IOC ëë°ë§¤ë§¤ë ěěĽě ě§ě ěě¤ě ě í´íë¤ęł ëłź ě ěëë°, ě´ ę˛°ęłźë Chung et al.(2014)ęłź Lee(2015)ę° ę°ę° íęľě 죟ěěěĽęłź ě 돟ěěĽěě HFTę° ěěĽě ě§ě ëśě ě ě¸ ěíĽě 미ěšë¤ë ě¤ěŚëśě결곟ě ëśíŠíë ę˛ě´ë¤.

6. 결ëĄ

본 ě°ęľŹěěë 2019ë

5ěëśí° 2020ë

9ěęšě§ KOSPI 200 ě§ěě 돟ěěĽě TAQ ë°ě´í°ëĽź ě´ěŠíěŹ ěĄ°ęą´ëśěŁźëŹ¸ ě¤ íëě¸ IOC죟돸ě 죟돸 íšěąě ě´í´ëł´ęł ě´ ěŁźëŹ¸ě´ ě§ěě 돟ěěĽě 미ěšë ěíĽě ě´í´ëł´ěë¤.

ëśě 결곟뼟 ě 댏í늴 ë¤ěęłź ę°ë¤. 첍째, ě쥴ë§ę¸° 30ěź ě´ë´ě ěľęˇźě돟 ě§ěě 돟ęłě˝ě 50%ę° IOC죟돸ě íľí´ě 체결ëěęł , IOC죟돸ě 99.9%ë ě¸ęľě¸íŹěěę° ě¤íí ę˛ěźëĄ ëíëŹë¤. ë째, IOC죟돸ě ë

댽ě ěźëĄ ë°ěí기 ëł´ë¤ë ěŹëŹ ęą°ëěę° ëěë¤ë°ě ěźëĄ 죟돸ě ě¤ííë ę˛ěźëĄ ëíë ëë°ë§¤ë§¤ě ěąę˛Šě ëł´ěŹěŁźęł ěěë¤. ëë°ë§¤ë§¤ě ě°¸ěŹí ęą°ëěěë 5ěě 9ěŹě´ę° ę°ěĽ ë§ěęł , ěľë 30ě´ě ě°¸ěŹí 경ě°ë ë°ěíęł ěë¤. ě

째, IOC죟돸ě ëí ęą°ëěëë°Šě ëśěí 결곟 ę°ě¸íŹěěę° 34%ëĄ ę°ěĽ ë§ěëë° ě´ë ę°ě¸íŹěěě ě 체 ęą°ëë ěěě ęą°ëëšě¤ě¸ 21%ëł´ë¤ 15% íŹě¸í¸ ë§ě ę˛ě´ěë¤. ëˇě§¸, IOC죟돸ěźëĄ ě¸í´ ë°ěë 죟돸íëŚëśęˇ íě´ ěźë°ěŁźëŹ¸ě ëší´ ë ë§ě ę°ę˛ŠěśŠę˛Šě ěźę¸°íë ę˛ěźëĄ ëśěëěë¤. ë¤ěŻě§¸, 체결ěę°ëśěě íľí´ě IOC매매ë ěźë°ë§¤ë§¤ëł´ë¤ 죟돸ě íęˇ ě˛´ę˛°ěę°ě 50% ě´ě ę°ěěí¤ë í¨ęłźę° ěë ę˛ěźëĄ ëíëŹë¤. ě´ë IOC매매ě íęˇ ěŁźëŹ¸ěëě´ ë§ęł ëë°ë§¤ë§¤ëĄ ëíë ëš ëĽ¸ ěëëĄ ěŁźëŹ¸ě§ęłěĽě ěŹęł 뼟 ěě§í기 ëëŹ¸ě¸ ę˛ěźëĄ íě´ëë¤. ěŹěŻě§¸, IOC ëë°ë§¤ë§¤ě ěŚę°ë í¸ę°ě¤íë ë뼟 ěŚę°ěí¤ęł , ěěĽěŹë뼟 ę°ěěí¤ëŠ° ěěĽëłëěąě ěŚę°ěí¤ë ëą ě§ěě 돟ěěĽě ěěĽíě§ě ëśě ě ěíĽě ëźěšë ę˛ěźëĄ 쥰ěŹëěë¤.

ę˛°ëĄ ě ěźëĄ IOCěŁźëŹ¸ě´ ëšěěĽěą ě§ě ę°ěŁźëŹ¸ě 체결ěę°ě ë¨ěśěěź ěěĽě ě ëěąě ę¸ě ě ě¸ ę¸°ěŹëĽź í기ë íě§ë§ ěěĽëłëěą, í¸ę°ě¤íë ëě ěěĽěŹë ëą ěěĽíě§ě ě í´íë ëśě ě ě¸ ě¸ĄëŠ´ě ëěě ę°ęł ěë¤ęł ëłź ě ěë¤. IOC죟돸ě ꡸ íšěąě 죟돸ě§ęłěĽě ěŹęł 뼟 ë¨ę¸°ě§ ěě ě ëěąě ěëšíë 경íĽě´ ę°í 죟돸ě´ęł , ëí íęˇ ěŁźëŹ¸ěëě´ ë§ęł ěŹëŹ ęą°ëěëśí° ëěě ë°ěí기 ë돸ě ě죟 짧ě ěŹě´ě ěľě°ě í¸ę°ě ěęł ę° ěě§ëë 경ě°ę° ë§ě ěěĽě ě§ě ëśě ě ěíĽě ëźěšë¤ęł íë¨í ě ěë¤. ěě <í 3>ě ęł ëšëęą°ëě ěŹëĄěěë ě ěíěëŻě´, ęł ëšëęą°ëë ë§ěźëŠě´íšě ëľ(market making trading strategies)ęłź 기íęą°ëě ëľ(opportunistic trading strategies) ëę°ëĄ ëśëĽí ě ěë¤. ë§ěźëŠě´ěť¤ě ëľě ěśęľŹíë HFTę° ë§ë¤ëŠ´ í¸ę°ě¤íë ëę° ę°ěíęł ěěĽěŹëę° ěŚę°íęł ëłëěąě´ ę°ěíë íě´ íŹę˛ ěěŠíë ë°ëŠ´, 기íęą°ëě ëľíě´ ë§ë¤ëŠ´ ꡸ ë°ëě íě´ ë íŹę˛ ěěŠí ę˛ě´ë¤. KOPSI200 ě§ěě 돟ěě IOCěŁźëŹ¸ě´ ě 체 체결ëě 50%뼟 ě°¨ě§íë¤ë ě ě ëšěśě´ ě´ ěěĽěě íëíë HFTě 죟ěśě ë§ěźëŠě´íšě ëľ ëł´ë¤ë 기íęą°ëě ëľě´ ěëęš ěśě¸Ąí´ëł¸ë¤. ę˛°ęľ ěěĽě ě´ë ě íě HFTę° ë ě°ě¸íę°ě ë°ëźě ęą°ëěěĽě íě§ě ę¸ě ě ě¸ ěí ě í ěë ěęł ęˇ¸ ë°ëě ěí ě í ě ěě ę˛ě´ë¤. HFTě ěěĽíě§ě ę´ęłě ę´í 기쥴돸íě ě°ęľŹëĽź 보늴 ę¸ě ęłź ëśě ě ě¸ íę° ëŞ¨ë 쥴ěŹíëë°, ě´ë í´ëš ěěĽěě HFTě 죟ëě¸ë Ľě´ ě´ë¤ ě ëľě ěŹěŠíëę°ě ë°ëź ěěĽě 미ěšë ěíĽě´ ëŹëźě§ë¤ęł ě§ěëë¤. ëŹźëĄ ě´ëŹí ę°ě¤ě íĽí 꾏체ě ě¸ ě¤ěŚëśěě íľí´ ęˇëŞ

ëě´ěź í ę˛ě´ë¤.

íěŹ ě ě¸ęł ęą°ëěěě ë˛ě´ě§ë HFT ěí¸ę°ě ęłźě´ë ěë경ěě ęľę° ę°ě 돴기경ěë§íźě´ë ěěě ëší¨ě¨ě ëśë°°ëźë ëšíěě ěě ëĄě¸ ě ěęł ëí ěëěěě ě´ěëĄ ě¸í ěěĽę˛˝ěěěě ëśě´ěľě´ ęłľě í ę˛ě¸ě§ě ëí´ěë ë

źěě ěŹě§ę° ěë¤. ę¸ěľěěĽěěě ěë경ěě ě§ě ěí¤ę¸° ěí ë°Šë˛ěźëĄ 돸íěě ë§ě´ ě ěëë ę˛ ě¤ě íëę° íěŹě ě ě매매(continuous two-sided auction)뼟 ëšë˛í ë¨ěźę°ë§¤ë§¤(batch auction ëë single price auction)ëĄ ë°ęž¸ěë ę˛ě´ë¤. Budish et al.(2015)ě íěŹ ě§íëë 돴í ěë경ěě ěľě í ě ěë ë°Šë˛ěźëĄ 매 1ě´ë§ë¤ ę°ąě ëë ë¨ěźę°ë§¤ë§¤ěěĽěźëĄě ě íě 죟ěĽíë¤. ě´ë í루ě 23,400í ě ë ë¤ěě 매ěě 매ëěŁźëŹ¸ě´ íëě 체결ę°ę˛ŠěźëĄ ęą°ëę° ěąěŹëë ę˛ě ě미íë¤. ě´ëŹëŠ´ 죟돸ě˛ëŚŹěë늴ěě 1ě´ ě´ë´ě ě°ěë ě í 경ěë Ľě ę°ě§ 몝íę˛ ëë¤. ě´ëĽź íľí´ 2010ë

ě Flash crashě ěŹë°ë ë§ě ě ěë¤ęł 죟ěĽíë¤. ě´ě¸ěë Menkveld(2014)ë ëěźí ě ë뼟 ěší¸í늰 1ě´ëš 10ë˛ě ë¨ěźę°ë§¤ë§¤ę° ě ëšíë¤ęł ëł´ěë¤. ëí Manahov(2021)ë HFTę° ě ëľě ë°ëłľěŁźëŹ¸ěě 졨ě죟돸ě 0-50ms ë´ě ë°ěěí¤ę¸° ë돸ě 50msë§ë¤ 1í(ěŚ 6ěę°ě ęą°ëěę°ě´ëźëŠ´ ě´ 6,308,571í)ě ë¨ěźę°ë§¤ë§¤ę° ě ě íë¤ęł ě ěíęł ěë¤. íęľęą°ëěě ěĽë´ěěĽěě ěëě ě´ ęłźě´ëě´ íšě íŹěě꡸룚ě ęą°ëí¸ě¤ě´ ěŹíę˛ ë ę˛˝ě° ęą°ë ëšęľěěë ě´ë° ě ëë íëě ëěěźëĄ íę°í´ëłź ě ěě ę˛ě´ë¤. ě´ ě ëë íěŹ íęľěěë 죟ěěěĽ ę¸°ě¤ ě¤ě 8:30-9:00, ě¤í 3:20~3:30 ęˇ¸ëŚŹęł 16:00~18:00ěě 10ëś ë¨ěëĄ ěíëęł ěë ë§íź ě´ë ě ëě ě´ě 경íě´ ěě´ ě´ëĽź íëíëë° ěě´ě 기ě ě ě´ë ¤ěě ë§ě§ ěě ę˛ěźëĄ íë¨ëë¤. ë¤ë§ ě 늴ě ě¸ ë¨ěźę°ë§¤ë§¤ëĄ ě¸í´ ě욍 ě ëěąě ę°ě, ę°ę˛Šë°ę˛Źę¸°ëĽě ě í, 체결ěę°ě ěŚę° ëąě ëśěěŠě´ ěëě§ëĽź ěě보기 ěí´ í´ě¸ěŹëĄëĽź ě´í´ëł´ë ëą ěśŠëśí ę˛í ę° íěí ę˛ě´ë¤.

본 ě°ęľŹëĽź íľí´ě ęł ëšëęą°ë뼟 기ë°ěźëĄ íë IOCěŁźëŹ¸ě´ KOSPI200 죟ę°ě§ě ě 돟ěěĽěěë ꡸ ëšě¤ě´ ë§¤ě° ëě 죟돸ě íě´ëźë ę˛ě´ ęˇëŞ

ëěë¤. íěě°ęľŹëĽź íľí´ íěěíěěĽ ëż ěëëź ěŁźěěěĽěě IOCěŁźëŹ¸ě´ ěźë§ë í° ëšě¤ěźëĄ íěŠëëě§ëĽź ęˇëŞ

íęł ěěĽíě§ě 미ěšë ěíĽě´ 쥰ěŹëë¤ëŠ´, íęľęą°ëěěě íëíë HFTě ě¤ě˛´ě ěěĽě 미ěšë ěíĽë Ľě ě˘ë 꾏체ě ěźëĄ íě

í ě ěě ę˛ě´ë¤.